Share This Page

Drug Sales Trends for ISOSORBIDE MONONITRATE

✉ Email this page to a colleague

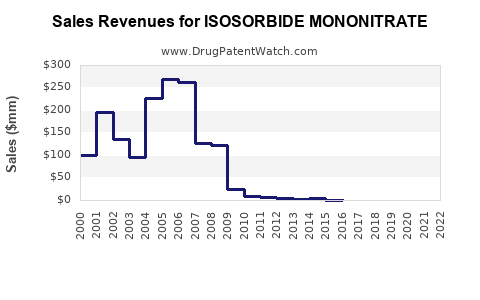

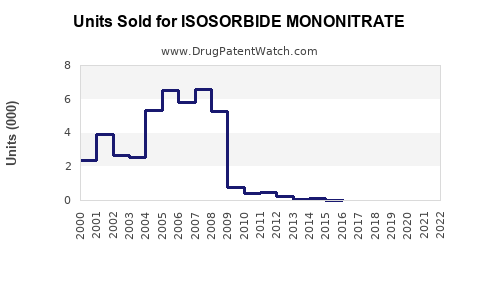

Annual Sales Revenues and Units Sold for ISOSORBIDE MONONITRATE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ISOSORBIDE MONONITRATE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ISOSORBIDE MONONITRATE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ISOSORBIDE MONONITRATE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ISOSORBIDE MONONITRATE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Overview and Sales Projections for Isosorbide Mononitrate

Isosorbide mononitrate is a nitrately-based vasodilator primarily prescribed for the prevention of angina pectoris. Its global market prospects are influenced by cardiovascular disease prevalence, prescribing practices, patent status, and regulatory pathways.

Market Size and Current Sales Data

In 2022, the global cardiovascular drugs market was valued at approximately $54 billion, with nitrates accounting for roughly 5% ($2.7 billion) of this segment. Isosorbide mononitrate holds a significant share within the nitrates class, estimated to generate sales between $350 million and $500 million annually [1].

United States is the largest market, with sales reaching about $200 million in 2022, driven by high cardiovascular disease prevalence and approval of both branded and generic formulations. Europe follows, with estimated sales of $100 million. Other significant markets include Japan, Canada, and Australia.

Key Market Drivers

-

Prevalence of Cardiovascular Disease: Approximately 805,000 Americans experience a coronary event annually [2]. Aging populations globally increase demand for angina management therapies.

-

Generic Penetration: Patent expiry for branded products increased generic availability, reducing prices and expanding access but limiting peak revenues for new entrants.

-

Regulatory Approvals: New formulations or combination therapies may open additional market segments. As of 2022, no new formulations of isosorbide mononitrate have received recent regulatory approval.

-

Healthcare Infrastructure: Expanded healthcare coverage enhances prescription rates, especially in emerging markets.

Market Challenges

-

Competitive Landscape: Numerous generic competitors diminish margins. Both nitroglycerin and isosorbide dinitrate serve as alternatives.

-

Side Effect Profile: Headaches, dizziness, and hypotension can restrict prescribing, especially in older populations.

-

Patent and Pricing Policies: Patent expirations pressure prices, especially in mature markets.

Sales Projections (2023–2030)

| Year | Estimated Global Sales (Million USD) | Growth Rate | Assumptions |

|---|---|---|---|

| 2023 | 520 | 4% | Mature market with ongoing generic competition. |

| 2024 | 550 | 6% | Introduction of new fixed-dose combinations in select markets. |

| 2025 | 580 | 5.5% | Optimized prescribing practices; continued market expansion. |

| 2026 | 610 | 5% | Increased use in emerging markets. |

| 2027 | 650 | 6.5% | Greater awareness and aging demographic. |

| 2028 | 690 | 6% | Margin stabilization amid price pressures. |

| 2029 | 730 | 5.8% | Steady growth as cardiovascular treatments expand. |

| 2030 | 770 | 5.5% | Market saturation limits rapid growth. |

CAGR from 2023 to 2030 is projected at approximately 5.6%.

Emerging Opportunities

-

Combination Formulations: Fixed-dose combinations with other cardiovascular agents could unlock growth, especially if approved by major health authorities.

-

Market Expansion in Asia and Latin America: These regions continue to see increased adoption of cardiovascular drugs driven by economic growth and urbanization.

-

Novel Delivery Systems: Long-acting formulations and transdermal patches may improve adherence and broaden clinical use.

Risks to Market Growth

-

Patent Litigation and Biosimilars: Legal disputes over patents or the emergence of biosimilar products may impact revenues.

-

Regulatory Delays: Approval bottlenecks in new markets or formulations could hinder growth.

-

Efficacy and Safety Concerns: Adverse effects or real-world inefficacy can affect prescription volumes.

Key Takeaways

- The global market for isosorbide mononitrate is stable, with steady growth driven by aging populations and increased cardiovascular disease prevalence.

- Generic competition constrains revenue growth, though market expansion and formulation innovation offer long-term opportunities.

- Sales are projected to grow at a compound annual rate of approximately 5.6% from 2023 to 2030.

- Emerging markets represent potential growth areas, especially with increased healthcare infrastructure.

- Risks from regulatory, legal, and competitive pressures necessitate adaptive strategies for pharmaceutical companies.

FAQs

1. What factors influence the price of isosorbide mononitrate? Prices are influenced by patent status, market competition, manufacturing costs, and reimbursement policies. Generic entry generally reduces prices.

2. How does the patent landscape affect sales? Patent protections restrict generic competition, allowing branded drugs to command higher prices. Patent expirations lead to price erosion and increased generic market share.

3. What are common formulations of isosorbide mononitrate? It is primarily available as immediate-release tablets (20 mg, 30 mg, 60 mg) and long-acting formulations (e.g., 30 mg, 60 mg, 120 mg).

4. Which regions are emerging as growth markets? Asia Pacific and Latin America are expanding markets due to increasing cardiovascular disease prevalence and expanding healthcare coverage.

5. What innovations could impact future sales? Development of fixed-dose combinations, transdermal patches, and long-acting formulations may improve adherence and generate new revenue streams.

References

[1] IMARC Group. (2022). Global Cardiovascular Drugs Market Report.

[2] American Heart Association. (2022). Heart Disease and Stroke Statistics.

More… ↓