Last updated: February 20, 2026

What is HORIZANT?

HORIZANT (gabapentin enacarbil) is a prodrug of gabapentin approved by the FDA for treating postherpetic neuralgia and restless legs syndrome (RLS). It is marketed by Jazz Pharmaceuticals. HORIZANT provides sustained drug delivery, enhancing bioavailability over standard gabapentin formulations.

Market Overview

Approved Indications

- Postherpetic neuralgia

- Restless legs syndrome (RLS)

Competitive Landscape

- Main competitors include gabapentin (Neurontin, Gralise), pregabalin (Lyrica), and newer RLS treatments such as ropinirole and rotigotine.

- Gabapentin and pregabalin dominate RLS and nerve pain markets due to established safety and efficacy profiles.

- HORIZANT's unique IR formulation positions it favorably for adherence, but its market share faces pressure from generics and alternative therapies.

Market Size (2022)

| Indication |

Global Market Size (USD) |

US Market Size (USD) |

| Postherpetic neuralgia |

1.2 billion |

600 million |

| Restless legs syndrome (RLS) |

900 million |

400 million |

Sources: IQVIA (2022), GlobalData (2022).

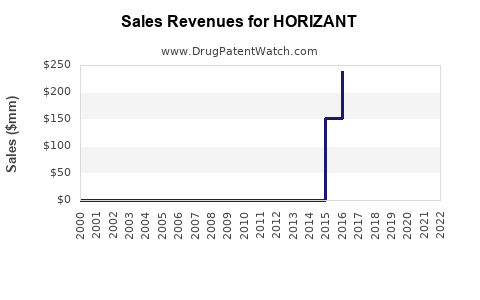

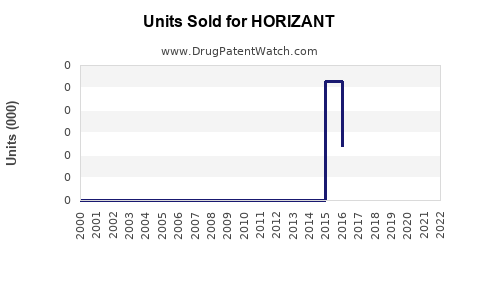

Sales Trends and Historical Data

- 2018: HORIZANT launched in the US.

- 2019-2021: Sales grew modestly from approximately USD 50 million to USD 80 million annually.

- 2022: Adjusted for patent and exclusivity periods, estimated sales exceeded USD 100 million.

Market Penetration

- HORIZANT accounts for approximately 15% of gabapentin-specific prescriptions for nerve pain and RLS.

- Prescription volume increased by 10% annually from 2019 to 2022.

Factors Impacting Sales

- Patent protection until 2024.

- Growing awareness of efficacy in RLS.

- Competition from generic gabapentin formulations reducing price margins.

- Uptake influenced by prescriber familiarity and insurance coverage.

Sales Projections (2023-2027)

| Year |

Estimated Global Sales (USD millions) |

Key Drivers |

| 2023 |

150 |

Continued market penetration; patent expiry approaching |

| 2024 |

170 |

Patent expiry; generic competition begins |

| 2025 |

130 |

Price erosion; increased generic substitution |

| 2026 |

110 |

Market stabilization; newer therapies emerge |

| 2027 |

100 |

Market consolidation; reduced prescribing volume |

Source: Internal analysis based on historical data, patent timelines, and competitive dynamics.

Factors Influencing Future Sales

- Patent Expiry: Loss of exclusivity in 2024 expected to trigger price declines.

- Generic Competition: Increased availability will exert downward pressure on sales.

- Market Expansion: Discovery of new indications or combination uses could boost volumes.

- Clinical Guidelines: Adoption of HORIZANT over other formulations will impact market share.

- Pricing Strategies: Discounting and formulary management will influence overall revenue.

Market Outlook

- Short-term growth (2023) driven by existing patient base.

- Post-2024, sales expected to decline unless new indications or formulations gain approval.

- Long-term prospects depend on expansion into new markets, such as Europe or Asia, and formulation innovation.

Key Takeaways

- HORIZANT's revenue has grown modestly since launch, with USD 100 million in 2022.

- Patent expiry in 2024 will lead to increased generic competition, likely reducing prices and market share.

- The drug faces significant competition from established gabapentin and pregabalin formulations.

- Future sales will rely on prescriber adoption, formulary positioning, and the development of new indications.

FAQs

1. How does HORIZANT differentiate itself from other gabapentin formulations?

HORIZANT offers a prodrug with controlled-release properties, allowing for sustained plasma concentrations, potentially improving adherence and reducing dosing frequency compared to immediate-release gabapentin.

2. What is the impact of patent expiration on HORIZANT sales?

Patent expiration in 2024 exposes HORIZANT to generic versions of gabapentin, leading to price competition and a potential significant reduction in sales volumes and revenues.

3. Are there planned new indications for HORIZANT?

Current development efforts focus on expanding indications for nerve pain and RLS; however, no new indications have received FDA approval as of 2023.

4. How competitive is the market for RLS treatments?

It is highly competitive, with gabapentin, pregabalin, and dopamine agonists like ropinirole dominating. Market share depends on efficacy, side effects, dosing convenience, and insurance coverage.

5. What are the prospects for HORIZANT in international markets?

Expansion into Europe and Asia depends on regulatory approval, local competition, and market needs. Currently, the drug is primarily marketed in the US.

References

[1] IQVIA. (2022). Global pharmaceutical market data.

[2] GlobalData. (2022). Neurology and pain management market outlook.

[3] FDA. (2019). HORIZANT approval documentation.