Drug Sales Trends for COREG

✉ Email this page to a colleague

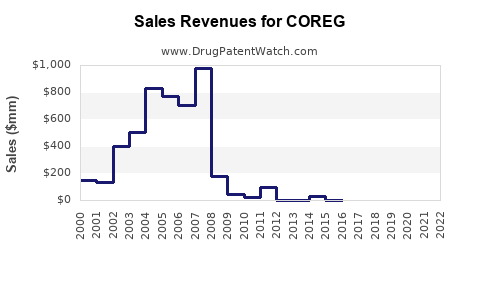

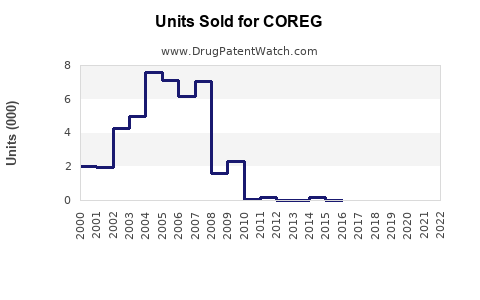

Annual Sales Revenues and Units Sold for COREG

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| COREG | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| COREG | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| COREG | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| COREG | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| COREG | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |