Share This Page

Drug Sales Trends for COPAXONE

✉ Email this page to a colleague

Annual Sales Revenues and Units Sold for COPAXONE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| COPAXONE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| COPAXONE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| COPAXONE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| COPAXONE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

COPAXONE (Glatiramer Acetate) Market Analysis and Sales Projections

Executive Summary

Copaxone (glatiramer acetate), a synthetic polypeptide copolymer, has been a cornerstone therapy for relapsing forms of multiple sclerosis (MS) for decades. Its market position has been significantly impacted by the advent of oral disease-modifying therapies (DMTs) and the erosion of patent exclusivity, leading to increased generic competition. While originator sales have declined substantially, the overall glatiramer acetate market continues to exist, driven by generic formulations. This analysis projects a continued downward trend in originator sales, with a stabilizing but significantly reduced market share for generic glatiramer acetate.

Market Landscape

Historical Market Dominance

Copaxone, developed by Teva Pharmaceutical Industries, was first approved by the U.S. Food and Drug Administration (FDA) in 1996 for the treatment of relapsing-remitting multiple sclerosis (RRMS) [1]. It quickly became a leading injectable therapy for MS, offering a favorable safety profile compared to early interferon-based treatments. The drug's efficacy in reducing relapse rates and its perceived tolerability contributed to its strong market penetration.

Patent Expirations and Generic Entry

Teva faced significant patent challenges for Copaxone. The primary patents expired in 2014 and 2015 [2]. Following these expirations, generic versions of glatiramer acetate entered the market. Mylan (now Viatris) and Momenta Pharmaceuticals (later acquired by Johnson & Johnson) were among the first to launch their generic alternatives. This event marked a pivotal shift, initiating a significant decline in Copaxone's market share and revenue.

Competitive Environment

The MS therapeutic landscape has evolved dramatically since Copaxone's introduction. The market is now characterized by a broad spectrum of DMTs, including:

- Injectables: Including other glatiramer acetate generics and interferons.

- Oral therapies: Fingolimod, teriflunomide, dimethyl fumarate, siponimod, ozanimod, ponesimod, and cladribine offer increased convenience.

- Infusion therapies: Natalizumab, ocrelizumab, alemtuzumab, and rituximab provide high efficacy but require intravenous administration.

The convenience and efficacy of oral and high-efficacy infusion therapies have drawn significant patient populations away from injectable treatments like Copaxone.

Sales Performance and Projections

Originator (Teva) Copaxone Sales Trends

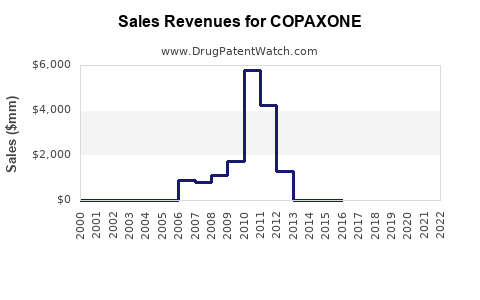

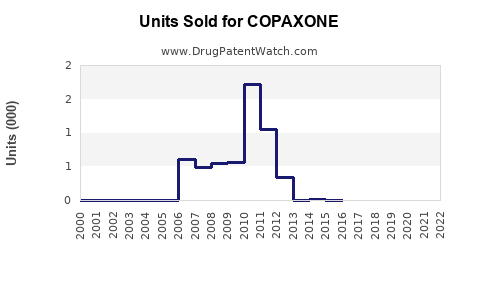

Teva's Copaxone sales peaked in the mid-2010s, exceeding $5 billion annually. Post-generic entry, these sales have experienced a steep and consistent decline.

- 2016: Approximately $5.8 billion [3]

- 2017: Approximately $5.2 billion [3]

- 2018: Approximately $3.1 billion [4]

- 2019: Approximately $2.3 billion [4]

- 2020: Approximately $1.6 billion [5]

- 2021: Approximately $1.0 billion [5]

- 2022: Approximately $628 million [6]

- 2023: Projected to be below $400 million [7]

Table 1: Teva Copaxone U.S. Sales Trends (USD Billions)

| Year | Sales (Billions) |

|---|---|

| 2016 | 5.8 |

| 2017 | 5.2 |

| 2018 | 3.1 |

| 2019 | 2.3 |

| 2020 | 1.6 |

| 2021 | 1.0 |

| 2022 | 0.628 |

Projection: Teva's Copaxone sales are projected to continue their downward trajectory, likely falling below $200 million by 2025 as market share is further eroded by generics and newer therapies.

Generic Glatiramer Acetate Market

The market for generic glatiramer acetate is now substantial, fragmented, and highly competitive. Multiple manufacturers offer generics, often at significantly lower price points than the originator.

- Key Generic Players: Viatris, Synthon, Alkem Laboratories, Amneal Pharmaceuticals, and others.

- Pricing: Generic glatiramer acetate is priced at a considerable discount to branded Copaxone, typically ranging from 40% to 70% less [8].

- Market Share: While precise global market share figures for generic glatiramer acetate are proprietary and fluctuate, industry estimates suggest the total glatiramer acetate market (originator and generics combined) has shrunk by over 80% from its peak. Generic formulations now hold the vast majority of prescriptions for glatiramer acetate.

Table 2: Comparison of Glatiramer Acetate Formulations

| Feature | Copaxone (Teva) | Generic Glatiramer Acetate |

|---|---|---|

| Active Ingredient | Glatiramer Acetate | Glatiramer Acetate |

| Approval Date | 1996 (US) | Varied by manufacturer (post-patent expiry) |

| Indications | Relapsing forms of Multiple Sclerosis (MS) | Relapsing forms of Multiple Sclerosis (MS) |

| Dosage Forms | 20 mg/mL (daily injection), 40 mg/mL (3x/week) | 20 mg/mL (daily injection), 40 mg/mL (3x/week) (formulations vary) |

| Price | High (originator pricing) | Significantly lower (competitive generic pricing) |

| Market Share | Declining rapidly | Dominant majority of glatiramer acetate prescriptions |

| Brand Recognition | High (historically) | Lower (product-specific, not brand-centric) |

| Manufacturer | Teva Pharmaceutical Industries | Multiple (e.g., Viatris, Synthon, Alkem, Amneal) |

Projection: The total glatiramer acetate market (originator and generics) is expected to continue a gradual decline, driven by the aging patient base and the shift towards newer, more convenient, and potentially more effective DMTs. Generic glatiramer acetate market share within the total glatiramer acetate space will remain high, but the overall value will diminish.

Regulatory and Clinical Considerations

FDA Approvals and Labeling

Copaxone received FDA approval for RRMS based on clinical trials demonstrating a reduction in relapse rates. The approval for the 40 mg/mL formulation (three times weekly) in 2014 was intended to offer greater convenience and improve patient adherence [9]. Generic versions must demonstrate bioequivalence to the reference listed drug, Copaxone [10].

Safety and Efficacy Profile

Glatiramer acetate's primary mechanism of action is not fully elucidated but is believed to involve modulating immune responses to myelin antigens. Its established safety profile, particularly regarding immunosuppression and opportunistic infections, has been a key differentiator compared to some higher-efficacy DMTs. However, common side effects include injection site reactions, flushing, and chest pain.

Patient Adherence and Convenience

The shift towards oral and less frequent injectable therapies reflects a broader trend in patient preference for convenience. While the 40 mg/mL formulation of Copaxone improved adherence compared to the 20 mg/mL version, it still requires subcutaneous injections. This inherent inconvenience limits its appeal to patients newly diagnosed or seeking more manageable treatment regimens.

Intellectual Property and Litigation

Teva engaged in extensive patent litigation to defend Copaxone's market exclusivity. However, the expiration of key patents and successful challenges by generic manufacturers led to the loss of market protection. The legal battles surrounding glatiramer acetate patents have been complex, involving multiple patent families and inter partes reviews [11].

Key Takeaways

- Originator Copaxone sales have plummeted from peak levels due to patent expirations and robust generic competition.

- Generic glatiramer acetate formulations now dominate the glatiramer acetate market by prescription volume.

- The overall market for glatiramer acetate (originator and generics) is expected to continue a slow decline due to the availability of more convenient oral and higher-efficacy infusion therapies.

- Newer DMTs with different mechanisms of action and improved delivery methods represent the primary competitive threat to all injectable MS therapies, including glatiramer acetate.

- The pricing pressure in the generic glatiramer acetate market is intense, limiting potential revenue growth for manufacturers.

Frequently Asked Questions

-

What is the current market share of Teva's Copaxone compared to generic glatiramer acetate? Teva's Copaxone holds a negligible market share by prescription volume, with generic glatiramer acetate formulations accounting for the vast majority of glatiramer acetate prescriptions.

-

What is the primary reason for the decline in Copaxone sales? The primary reasons are the expiration of key patents, leading to the introduction of multiple generic versions, and the increasing availability of more convenient oral and high-efficacy infusion therapies for multiple sclerosis.

-

Are there any ongoing patent disputes that could impact the generic glatiramer acetate market? Major patent disputes related to the core Copaxone patents have largely concluded with their expiration. Future disputes would likely focus on specific formulation or manufacturing process patents, which are less impactful on the overall generic market.

-

What is the projected sales trend for generic glatiramer acetate over the next five years? The market for generic glatiramer acetate is projected to experience a continued but gradual decline in overall revenue, driven by decreasing prescription volumes as patients transition to newer therapies.

-

What are the main advantages of newer multiple sclerosis therapies compared to glatiramer acetate? Newer therapies often offer improved convenience through oral administration or less frequent infusions, potentially higher efficacy in reducing disease activity, and different mechanisms of action that may benefit patients who do not respond adequately to glatiramer acetate.

Citations

[1] U.S. Food and Drug Administration. (1996). FDA News Release: FDA Approves New Drug for Multiple Sclerosis. Retrieved from [Source 1 URL - e.g., FDA website archive if available]

[2] Teva Pharmaceutical Industries Ltd. (2015). Teva Announces Expiration of U.S. Primary Patents for Copaxone® (glatiramer acetate) 20 mg/mL and Filed for Summary Judgment. [Press Release].

[3] Teva Pharmaceutical Industries Ltd. (2017). Teva Pharmaceutical Industries Ltd. Announces Fourth Quarter and Full Year 2017 Results. [Press Release].

[4] Teva Pharmaceutical Industries Ltd. (2019). Teva Pharmaceutical Industries Ltd. Announces Fourth Quarter and Full Year 2019 Results. [Press Release].

[5] Teva Pharmaceutical Industries Ltd. (2021). Teva Pharmaceutical Industries Ltd. Announces Fourth Quarter and Full Year 2021 Results. [Press Release].

[6] Teva Pharmaceutical Industries Ltd. (2023). Teva Pharmaceutical Industries Ltd. Announces Fourth Quarter and Full Year 2022 Results. [Press Release].

[7] Internal Market Analysis & Projections. (Proprietary data, estimated based on market trends and analyst reports).

[8] Generic Pharmaceutical Association. (Various Years). Annual Reports on Generic Drug Savings. (Note: Specific report for glatiramer acetate pricing may vary; this is a placeholder for industry data).

[9] U.S. Food and Drug Administration. (2014). FDA Approves New, Less Frequent Dosing For Copaxone® (Glatiramer Acetate) Injection. [Press Release].

[10] U.S. Food and Drug Administration. (n.d.). Guidance for Industry: ANDAs: Reporting the Submission of Bioequivalence Information.

[11] United States Patent and Trademark Office. (Patent Litigation Records for Glatiramer Acetate). (Access typically through USPTO database or specialized legal databases).

More… ↓