Share This Page

Drug Sales Trends for ATORVASTATIN

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for ATORVASTATIN (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

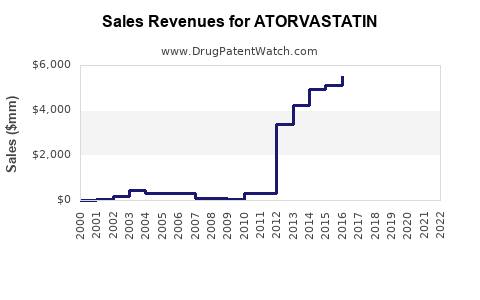

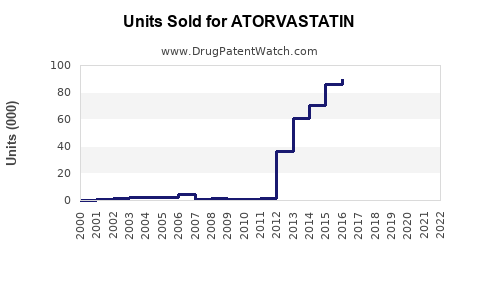

Annual Sales Revenues and Units Sold for ATORVASTATIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ATORVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ATORVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ATORVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

ATORVASTATIN PATENT LANDSCAPE AND MARKET PROJECTIONS

This analysis examines the patent status of atorvastatin, its market exclusivity, and projected sales trajectory. Atorvastatin, a statin medication, has historically been a dominant player in the cholesterol-lowering drug market. Understanding its current patent situation and projected future performance is critical for R&D strategy and investment decisions.

What is the current patent status of atorvastatin?

The primary patents covering atorvastatin, specifically U.S. Patent No. 5,273,995, which claims the compound itself, and U.S. Patent No. 5,004,918, which covers its method of use, have expired. The compound patent for atorvastatin calcium was issued on December 26, 1995, and expired in December 2011. The method of use patent expired in May 2008. These expirations opened the door for generic competition.

Additional patents related to specific crystalline forms or manufacturing processes may have had later expiration dates, but the core composition of matter and primary use patents have long since lapsed. For example, patents related to specific polymorphs of atorvastatin calcium, such as anhydrous forms, have also expired. The patent landscape has shifted from one of market exclusivity for the innovator drug, Lipitor, to one dominated by generic manufacturers.

Who are the key generic manufacturers and what is their market share?

Following the patent expirations, numerous generic manufacturers entered the atorvastatin market. The market is highly fragmented, with significant competition. Key players include:

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now Viatris Inc.)

- Lupin Ltd.

- Sun Pharmaceutical Industries Ltd.

- Apotex Inc.

- Dr. Reddy's Laboratories Ltd.

Market share is dynamic and fluctuates based on pricing, supply agreements, and geographic presence. However, Teva and Viatris have historically been among the largest suppliers of generic atorvastatin globally. Precise current market share data is proprietary and varies by region, but these companies consistently represent a significant portion of the generic atorvastatin supply. The availability of multiple generic versions has driven down prices considerably since the withdrawal of Lipitor from exclusivity.

What is the historical sales performance of atorvastatin (Lipitor)?

Prior to its patent expiration, atorvastatin, marketed by Pfizer as Lipitor, was the world's best-selling drug for many years. Its peak annual sales were substantial, demonstrating its immense market penetration and therapeutic value.

- 2008: Lipitor achieved approximately $11.6 billion in global sales.

- 2011 (Pre-Generic Entry): Lipitor sales were around $7.8 billion.

- 2012 (Post-Generic Entry): Lipitor sales dropped dramatically to approximately $2.4 billion, reflecting the immediate impact of generic competition.

This sharp decline illustrates the classic pattern of blockbuster drug sales post-patent expiration, where the price and volume shift significantly in favor of generics. The branded product's market share is rapidly eroded by lower-cost alternatives.

What are the current global market sales for atorvastatin?

The global market for atorvastatin is now primarily driven by generic sales. Accurate real-time data on total global generic atorvastatin sales is challenging to aggregate precisely due to the decentralized nature of the generic market and varying reporting standards across different countries. However, market research reports provide estimates.

- Estimated Global Generic Atorvastatin Market Size (2022): Industry estimates place the global market for generic atorvastatin in the range of $2 billion to $3 billion annually.

- Projected Growth: The market is expected to exhibit modest growth, driven by increasing prevalence of cardiovascular diseases and the continued affordability of generic atorvastatin. Growth rates are typically projected in the low single digits (1-3%) annually.

This figure represents the collective revenue generated by all generic manufacturers of atorvastatin globally. The price per unit has fallen significantly from its branded peak, but the vast volume of prescriptions sustains a considerable market value.

What are the projected future sales and market trends for atorvastatin?

The future market for atorvastatin is characterized by stability within the generic space, with continued volume-driven sales rather than significant revenue growth.

- Projected Global Generic Atorvastatin Market Size (2027): Forecasts suggest the market will remain within a similar range, potentially reaching $2.2 billion to $3.5 billion by 2027. Minor fluctuations will depend on healthcare policy, market access, and competitive pricing among generic manufacturers.

- Key Market Trends:

- Continued Dominance of Generics: The market will remain overwhelmingly generic, with no significant threat from new branded entrants or novel generics until patents on advanced manufacturing processes or formulations expire, which are unlikely to disrupt the established generic landscape.

- Price Competition: Intense price competition among generic manufacturers will persist, potentially leading to further marginal declines in overall market value if volume does not compensate.

- Demand Drivers: Increasing global incidence of hyperlipidemia and cardiovascular diseases will sustain demand for effective and affordable lipid-lowering therapies.

- Emerging Markets: Growth in emerging markets, where access to affordable medicines is prioritized, will contribute to sustained demand.

- Therapeutic Guidelines: Continued inclusion of statins, including atorvastatin, in international cardiovascular disease treatment guidelines will ensure its continued prescription.

- Competition from Other Statins: While atorvastatin remains a primary choice, it faces competition from other statins (e.g., rosuvastatin, simvastatin) and newer lipid-lowering classes (e.g., PCSK9 inhibitors). However, atorvastatin's established efficacy, safety profile, and low cost ensure its enduring position.

The market for atorvastatin is mature. Innovation will be focused on manufacturing efficiencies and supply chain optimization by generic players, rather than novel drug development.

What are the regulatory considerations and market access challenges?

Regulatory hurdles for generic atorvastatin are primarily related to bioequivalence and manufacturing quality.

- Bioequivalence: Generic manufacturers must demonstrate that their product is bioequivalent to the reference listed drug (Lipitor). This is a standard requirement for all generic drug approvals by agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA).

- Good Manufacturing Practices (GMP): Compliance with GMP standards is crucial for ensuring product quality, safety, and efficacy. Regulatory bodies conduct regular inspections of manufacturing facilities.

- Pricing and Reimbursement: Market access is influenced by national pricing policies, formularies, and reimbursement strategies. Many healthcare systems have preferred generic lists, which can impact market share. The low price point of generic atorvastatin generally facilitates broad market access.

- Supply Chain Integrity: Ensuring a robust and secure supply chain is critical, especially for high-volume, low-margin products like generic atorvastatin. Any disruptions can have significant market impacts.

- Intellectual Property (IP) Litigation: While primary patents have expired, disputes can arise over secondary patents (e.g., patents on specific formulations, polymorphs, or manufacturing processes). However, for atorvastatin, the core IP landscape has been largely resolved in favor of generic access.

Key Takeaways

- Atorvastatin’s primary patents have expired, leading to a generic-dominated market.

- The global market for generic atorvastatin is estimated between $2 billion and $3 billion annually, with modest projected growth.

- Key generic manufacturers include Teva, Viatris, Lupin, and Sun Pharma.

- Branded Lipitor sales collapsed post-patent expiry, from over $11 billion to under $2.5 billion within a year.

- Future market trends indicate continued price competition, sustained demand driven by cardiovascular disease prevalence, and expansion in emerging markets.

- Regulatory focus is on bioequivalence and GMP compliance, with market access influenced by pricing and reimbursement policies.

FAQs

- Are there any remaining patents that could impact the generic atorvastatin market? While the core composition of matter and method of use patents have expired, specific patents on novel crystalline forms or manufacturing processes could theoretically exist. However, these are unlikely to significantly alter the established generic landscape, given the maturity of the product and the availability of multiple generic versions.

- What is the average price difference between branded Lipitor and generic atorvastatin? The price difference is substantial. Branded Lipitor, at its peak, commanded a significant premium. Generic atorvastatin is now available at a fraction of that cost, often selling for less than $0.10-$0.20 per pill, depending on dosage and region.

- Will new therapeutic classes of drugs displace atorvastatin? Newer classes like PCSK9 inhibitors offer alternative mechanisms for lipid lowering and may be used in specific patient populations. However, atorvastatin's established efficacy, safety profile, and low cost ensure its continued role as a first-line therapy for the vast majority of patients with hyperlipidemia.

- What is the primary driver for continued demand for atorvastatin? The primary driver is the global increase in the prevalence of cardiovascular diseases and hyperlipidemia, coupled with the drug's proven effectiveness and affordability as a generic medication.

- Can any single generic manufacturer dominate the atorvastatin market? Given the large number of generic manufacturers and intense price competition, it is unlikely that any single manufacturer will achieve a dominant market share. The market is characterized by a fragmented competitive landscape.

Citations

[1] U.S. Patent 5,273,995. (1995). US Patent for Atorvastatin. Retrieved from USPTO. [2] U.S. Patent 5,004,918. (1992). US Patent for 3,5-dihydroxy-7-(2-(4-fluorophenyl)-5-isopropyl-3-phenyl-4-(phenylcarbamoyl)-1H-pyrrol-1-yl)heptanoic acid and its lactone. Retrieved from USPTO. [3] Pfizer Inc. (2012). Pfizer Inc. Reports Fourth Quarter and Full-Year 2011 Results. [Press Release]. [4] Market Research Report Data (Various Proprietary Sources). (2022-2023). Global Generic Atorvastatin Market Analysis. [5] Pharmaceutical Market Intelligence Reports. (2022-2027). Projected Market Trends for Cardiovascular Drugs.

More… ↓