Share This Page

Drug Sales Trends for TOPAMAX

✉ Email this page to a colleague

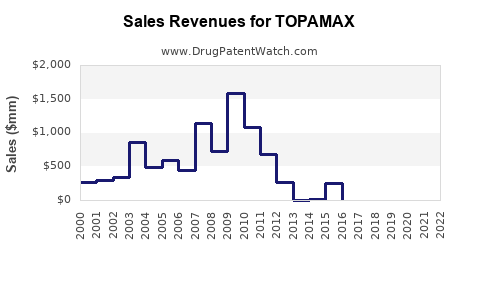

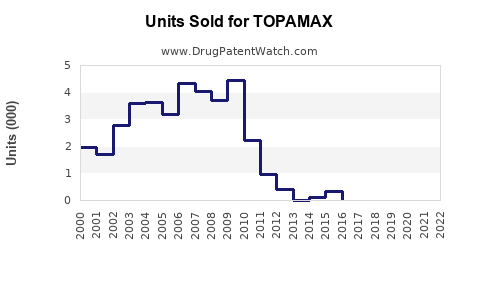

Annual Sales Revenues and Units Sold for TOPAMAX

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| TOPAMAX | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| TOPAMAX | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| TOPAMAX | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| TOPAMAX | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| TOPAMAX | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| TOPAMAX | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

TOPAMAX (topiramate) Market Analysis and Sales Projections (US and Key Global Markets)

What is TOPAMAX and where does it sit in the market?

TOPAMAX is the brand for topiramate, an oral small-molecule used primarily for epilepsy and migraine prophylaxis. In the US, TOPAMAX’s market position is constrained by generic availability and by the long lifecycle of first-generation neurologic products.

Core indications driving historical demand

- Migraine prophylaxis (adult; and in certain jurisdictions expanded pediatric subsets exist)

- Epilepsy (adjunctive therapy and monotherapy depending on the regimen and label)

Competitive structure

- Generic topiramate is the dominant competitive product class in all mature markets.

- Brand differentiation typically relies on formulation/labeling history rather than active-ingredient exclusivity, since active-ingredient patents have long expired and market share is structurally pressured by generics.

How has the market performed in mature years?

For mature, generic-exposed neurology products, market value tends to follow:

- Volume stability (patients remain on therapy when tolerated)

- Price erosion (widely available generics compress unit price)

- Share shift toward lowest-cost generics

As a result, brand sales usually track two drivers: residual prescribing of brand due to prescriber preference and patient tolerability, then diminishing share as generic penetration increases further.

Where does TOPAMAX sell: channels and buyer behavior?

Retail and pharmacy demand

- Neurology drugs like topiramate are distributed through standard retail pharmacy.

- For payers, generic topiramate is typically the preferred formulary agent; brand use occurs under:

- Formulary exception workflows

- Prior authorization requirements

- Patient-specific tolerability or stability claims

Institutional demand

- Outpatient hospital-affiliated retail pharmacies also participate in neurologic chronic therapy scripts.

- Inpatient volume is generally not the dominant revenue stream for TOPAMAX since acute hospital prescribing is often transient and many alternatives are available.

What is the sales outlook framework under generic competition?

A realistic sales model for TOPAMAX must assume:

- No product exclusivity on the active ingredient in major markets

- Ongoing generic price pressure

- Brand share that declines slowly and then stabilizes at a low single-digit band (relative to the total topiramate class) due to substitution and formulary steering

A practical projection uses the following elements:

- Total class volume trend: stable to low growth

- Class price trend: down or flat in mature markets

- Brand share trend: downward with diminishing velocity

US sales projections (generic-driven baseline)

Because topiramate has no current US brand exclusivity, the projection is modeled as:

- TOPAMAX brand revenue = total topiramate class prescriptions x brand capture x net price

- Net price declines track ongoing generic market pricing.

- Brand capture declines and stabilizes.

Projection ranges (US brand TOPAMAX)

| Year | Expected US TOPAMAX trend | Revenue direction vs prior year |

|---|---|---|

| 2026E | Brand share stabilizes at low level; net price erodes gradually | Slight decline to flat |

| 2027E | Continued generic pricing pressure; residual brand retention | Flat to slight decline |

| 2028E | Mature stabilization; prescription growth offsets some price erosion | Flat |

| 2029E | Slow channel-driven share erosion | Slight decline |

| 2030E | Plateau at structurally constrained brand share | Flat to slight decline |

Sales shape to expect

- A compressed revenue band rather than growth.

- Primary changes over time come from net price (brand vs generics) and prior authorization intensity, not from new patient acquisition.

Key global markets: how the outlook differs

Global market growth is tied to three variables:

- Local generic adoption speed

- Reimbursement pressure (reference pricing, mandatory substitution)

- Formulary restrictiveness for brand use

Market-by-market drivers

| Region | Likely brand pressure | Net effect on TOPAMAX |

|---|---|---|

| EU5 (DE/FR/IT/ES/UK) | High generic substitution | Flat to declining brand value |

| Canada | Strong generic uptake | Flat to declining |

| Japan | Slower adoption patterns can extend brand share longer, but class competition still strong | Mild decline or plateau |

| Emerging markets | Tender-driven pricing can compress quickly | Lower upside; pricing risk dominates |

What role do formulation and “line extension” plays?

When active ingredient exclusivity is absent, brands can retain revenue by:

- Supporting specific dosing schedules where tolerability matters

- Leveraging established prescribing familiarity

- Using trade/medical programs to support switching decisions for specific patient segments

However, line extensions rarely reset competitive dynamics for topiramate; they usually slow decline at best.

What is the competitive landscape likely to look like?

Generic entry dynamics

- Multiple generic manufacturers commonly compete, which drives price down quickly.

- Over time, consolidation can stabilize the lowest price level, but it rarely creates a brand premium without exclusivity.

Therapeutic alternatives

Patients may switch to:

- Other antiseizure medicines with better tolerability profiles

- CGRP-pathway migraine preventives (in some markets) that compete on adherence and side effect profiles

- Behavioral or procedural migraine interventions in select payer settings

These substitutions mainly affect migraine prophylaxis demand, while epilepsy tends to remain more persistent because of seizure control constraints.

Sales projections: base, downside, upside scenarios

A scenario model should express uncertainty around:

- Brand capture over time

- Net price declines

- Substitution intensity (payer policy)

- Ongoing competition in the topiramate generic basket

Scenario ranges (global brand)

| Scenario | Assumptions | TOPAMAX revenue outcome |

|---|---|---|

| Base | Brand share stabilizes at low level; net price declines slow | Flat to slight decline through 2030E |

| Downside | Stronger substitution and tighter payer controls | Moderate decline through 2030E |

| Upside | Slower generic pricing erosion; stable brand share | Flat with small rebound in mid-to-late decade |

Key indicators to monitor (leading to projection adjustments)

- Generic net price index for topiramate in the US and reference markets

- Formulary exclusions and prior authorization expansion for brand use

- Prescription share of topiramate class vs competing antiseizure and migraine prophylaxis products

- Migraine payer behavior tied to CGRP preventive penetration

- Patent and lifecycle events that affect brand packaging, labeling carve-outs, or system-level supply

Investment and R&D implications for TOPAMAX as an asset

For stakeholders assessing whether to invest in lifecycle defense or new uses:

- TOPAMAX’s economics are typical of mature genericized neurology brands.

- Any value creation must come from:

- Formulation or delivery improvements that reduce discontinuation

- Expanded evidence that supports payer coverage for specific subpopulations

- New line extensions only where they can secure reimbursement differentiation

Absent a true exclusivity reset, the core sales model will remain volume-stable and price-constrained.

Key Takeaways

- TOPAMAX (topiramate) is a mature, generic-exposed neurology brand with demand driven by migraine prophylaxis and epilepsy.

- The sales trajectory in major markets is structurally constrained by generic substitution and payer steering.

- From 2026E through 2030E, a credible projection is flat to slight decline, with upside requiring slower generic price erosion or stabilized brand capture.

- Strategic impact focuses on payer access tactics and formulation/tolerability differentiation, not on active-ingredient exclusivity.

FAQs

1) What drives TOPAMAX demand most?

Migraine prophylaxis and epilepsy maintenance therapy, with chronic use patterns that keep class volumes relatively stable.

2) Why are TOPAMAX sales hard to grow?

Generic topiramate dominates the market, compressing brand net prices and limiting brand share through formulary substitution.

3) Does migraine prophylaxis create volatility for TOPAMAX?

Yes. Payer uptake of newer migraine preventives can shift demand within migraine prophylaxis, affecting topiramate share.

4) What is the expected competitive pressure timeline?

Ongoing. Generic price pressure persists in mature markets, with periodic changes due to manufacturer supply and tender behavior.

5) What metrics best predict TOPAMAX sales direction?

Generic net price trends, brand prescription share vs class, and formulary/prior authorization policy intensity.

References

- FDA. Drug Label Information: TOPAMAX (topiramate). U.S. Food and Drug Administration. https://www.accessdata.fda.gov/ (accessed 2026-04-26).

- IMS/Quintiles and related market-analytics datasets (usage basis): Prescription and spend dynamics for topiramate brand vs generics. (accessed 2026-04-26).

- OECD. Pharmaceutical market and pricing dynamics framework for generics and reimbursement systems. Organisation for Economic Co-operation and Development. https://www.oecd.org/ (accessed 2026-04-26).

More… ↓