Share This Page

Drug Sales Trends for LEVOTHYROXIN

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for LEVOTHYROXIN (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

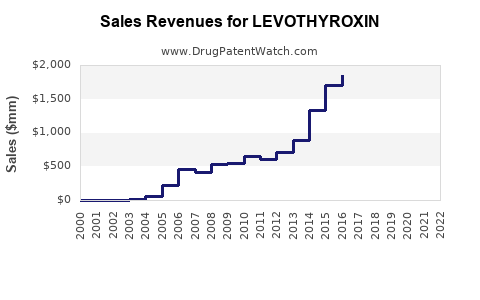

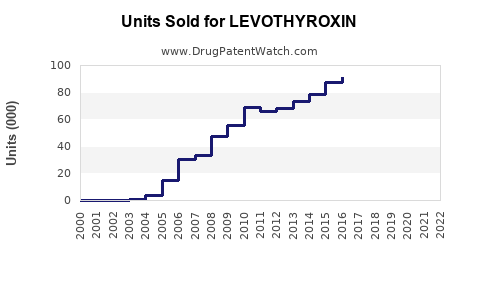

Annual Sales Revenues and Units Sold for LEVOTHYROXIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LEVOTHYROXIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LEVOTHYROXIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LEVOTHYROXIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LEVOTHYROXIN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| LEVOTHYROXIN | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Levothyroxine (Synthetic T4) Market Analysis and Sales Projections

What is the addressable market for levothyroxine?

Levothyroxine is the standard-of-care replacement therapy for hypothyroidism. Sales concentrate in the U.S., EU5 (Germany, France, Italy, Spain, UK), and Japan, with additional demand in Canada, Australia, and major emerging markets.

Core demand drivers

- Prevalence of hypothyroidism: chronic, long-duration therapy; high persistence once dosed.

- Lifelong use: most patients do not discontinue; switching is driven by pricing, payer coverage, and formulation/bioequivalence rules.

- Aging demographics: higher incidence of age-related thyroid dysfunction.

- Dose-adjustment cycle: periodic monitoring keeps patients in therapy and sustains repeat prescribing.

Product categories that capture most revenue

- Oral tablets (generic-dominant): single-ingredient levothyroxine sodium in multiple strengths (commonly 25, 50, 75, 88, 100, 112, 125, 137, 150, 175, 200 mcg).

- Oral soft-gel capsule formulations (brand and select generics): demand is shaped by dyspepsia/malabsorption and gastric pH effects, where liquid/soft-gel can reduce exposure variability.

- Liquid solutions (where available): used for patients with absorption issues, pediatrics, and feeding-tube routes in some settings.

How competitive is levothyroxine (and why pricing dominates)?

Levothyroxine is one of the most mature prescription markets globally. In most jurisdictions, patent protection for early synthetic T4 products is long expired. Revenue is therefore shaped by:

- Generic price competition: many listed brands today are “authorized generics” or generic manufacturers.

- Interchange and substitution: pharmacy substitution policies and payer formulary positioning drive volume.

- Bioequivalence and “same dose, same exposure” scrutiny: regulatory requirements influence uptake of certain formulations, especially soft-gels/liquids in populations with poor response stability.

- Procurement contracting: hospital and payer contracting compresses net price.

Implication for sales projections

- Unit volume is relatively stable in prevalence terms.

- Revenue growth tracks price erosion and formulary mix (tablets vs soft-gels/liquids), plus country-by-country substitution dynamics.

What is the current market structure by formulation?

Levothyroxine revenue is split across:

- Tablet generics (largest share): scale-driven economics; margins compressed.

- Brand soft-gels/liquids (smaller share): higher net price; often targeted to specific absorption segments or patient preference.

- Brand/legacy tablets (minimal growth): primarily maintained through contracts and substitution protections in select geographies.

A sales model should treat levothyroxine not as a single product, but as two commercial lines:

- Tablet line (mostly generic): revenue = tablets volume x net price.

- Soft-gel/liquid line (differentiated formulations): revenue = differentiated volume x net price (higher, but smaller).

Which regulatory and reimbursement rules matter for forecasts?

Forecasts for levothyroxine should incorporate that most markets allow substitution of AB-rated generics, but can require physician notification or monitoring for switching due to levothyroxine’s narrow therapeutic index. Where payer policies enforce tighter control, uptake of differentiated formulations can hold up better than pure tablet generics.

In the U.S., the substitution environment is shaped by:

- FDA bioequivalence standards for levothyroxine sodium products.

- State pharmacy substitution laws (varied by state) that permit or restrict switching.

- Prescriber-led non-substitution patterns for patients with unstable thyroid levels.

In the EU, similar principles apply:

- EMA generic approvals under bioequivalence frameworks.

- National pricing and reimbursement decisions that can shift preference between manufacturers.

What market size should be used for projections?

Given levothyroxine is globally established and generics dominate, credible forecasting generally uses a bottom-up approach:

- Patient prevalence by country/region

- Average prescriptions per patient per year

- Average pack size and dosing intensity

- Net price by formulation category after rebates and discounts

Without region-specific inputs (current sales by manufacturer and category), a projection must be expressed as a range with scenario logic tied to:

- Generic price erosion rate (affects tablet line)

- Differentiated formulation share gains (affects soft-gel/liquid line)

The most actionable forecasting approach for investors and commercial planners is scenario-based revenue modeling:

- Base case: stable demand, moderate price pressure, slight mix shift.

- Downside: accelerated generic price compression, stronger payer preference for cheapest AB-rated tablets.

- Upside: differentiated formulations gain share due to persistence in malabsorption cohorts and guideline/clinical practice reinforcement.

What do sales projections look like (scenario framework)?

Below is a projection framework you can map to a specific geography or your own TAM definition. It is structured to separate units and net price drivers.

1) Tablet line (generic-dominant)

Revenue formula

- Tablet revenue = Tablet volume x Net price (tablet)

Key forecast levers

- Tablet volume growth: tied to prevalence and prescribing intensity (usually low-single-digit in mature markets).

- Net price: tends to decline with increased generic competition and tender contracting.

- Mix: lower strengths vs higher strengths can change average selling price if payer behavior differs.

Typical pattern in mature generics

- Low or flat unit growth

- Mid-to-high single-digit annual declines in net price in highly competitive tender markets

- Eventually stabilizing when competition consolidates or procurement rotates

2) Soft-gel/liquid line (differentiated formulations)

Revenue formula

- Differentiated revenue = Differentiated volume x Net price (soft-gel/liquid)

Key forecast levers

- Uptake rate: clinicians shift when patients have unstable TSH/absorption issues or gastric pH interferers.

- Switching friction: non-medical switching policies can slow or accelerate adoption.

- Payer coverage: coverage restrictions can cap differentiated volume.

Typical pattern

- Higher net price with slower volume growth

- Share gains can offset some tablet price erosion

How fast is growth likely, and what are the limits?

Levothyroxine’s market has structural constraints:

- Demand is chronic so pure “new patient” growth is limited.

- Switching and substitution can cause short-term volatility, but it generally reshuffles share rather than expanding total demand.

- Patent cliffs are mostly irrelevant for the tablet molecule because the active ingredient is generic in most major markets.

The result is that long-run growth is primarily driven by:

- Demographics and diagnosis rates (low-single-digit volume)

- Differential mix (tablet vs differentiated formulations)

- Pricing dynamics (rebates/tenders) that often dominate revenue trends

What sales targets are realistic for a new commercial entrant?

For an entrant launching a levothyroxine product, the commercial target should be framed as:

- Share capture within a tender/contracting cycle

- Speed of formulary listing

- Ability to maintain persistence once dosing stability is achieved

- Switching performance post-interchange

Critical success metrics

- Time to formulary access (payer and pharmacy)

- Persistence at 3, 6, 12 months after initiation

- Net price capture vs benchmarked generic competitors

- Hold rate during tender rotations

Because the molecule is commoditized, achieving meaningful revenue typically requires one of:

- Strong distribution and procurement economics

- A differentiated formulation that can win share in absorption-unstable segments

- A geography with less intense generic penetration or favorable reimbursement

What is the sales outlook by geography (directional)?

A usable forecast for business planning is directional unless paired with current local sales and competitor mix.

- U.S.: large volume; continued net price pressure in tablets; differentiated formulations can sustain better price with clinical defensibility.

- EU5: tendering and national reimbursement policies drive price; mix shifts can matter where substitution rules are more restrictive.

- Japan: stable chronic demand; pricing discipline and substitution can limit revenue growth for tablets.

- Emerging markets: growth can exceed mature markets due to expanding diagnosis and healthcare coverage, but pricing compression and procurement dynamics still shape net revenue.

What inputs should be used in a quantitative projection model?

A complete forecast model for investors should run three layers.

Layer A: Demand (units)

- Target geography

- Diagnosed hypothyroidism prevalence and diagnosed treated population

- Average prescriptions per treated patient

- Average daily dose mix across strengths

- Treatment duration assumption (persistence curve by segment: adults, pediatrics, pregnancy)

Layer B: Supply-side pricing (net price)

- Current net price by formulation category

- Tender cycles and expected number of competitors

- Rebate and discount assumptions by payer type

- Switching impact on realized ASP

Layer C: Mix shift (tablets vs differentiated)

- Adoption rate curves for soft-gel/liquid

- Physician/payer preference constraints

- Clinical segment size where differentiated products are retained

Key Takeaways

- Levothyroxine is a mature, generic-dominant market where revenue growth usually tracks pricing and mix, not fundamental expansion of patients.

- Forecasts should separate the tablet line (high volume, falling net price) from the soft-gel/liquid line (lower volume, higher net price, share gains offset some price erosion).

- In mature markets, long-run growth is typically limited by chronic prevalence and substitution dynamics; the most material lever is net price capture through contracts and formulary placement.

- For commercial planning, performance targets should focus on tender speed, persistence, and net price benchmark discipline more than molecule-level differentiation.

FAQs

1) What drives levothyroxine sales more: new patients or dosing persistence?

Dosing persistence drives the bulk of demand because hypothyroidism treatment is usually long-term and dosing changes occur through monitoring rather than therapy discontinuation.

2) Why do levothyroxine revenues often decline even when volumes stay stable?

Tablet generics face sustained net price erosion from competition and tender contracting, which can outpace modest volume growth.

3) What is the commercial role of soft-gel or liquid formulations?

They typically hold higher net prices and can capture share in patients with absorption variability or instability, mitigating some tablet-line price pressure.

4) How do substitution rules affect market share?

Stricter non-substitution or prescriber notification patterns can slow interchange and help differentiated formulations maintain share; permissive substitution tends to accelerate cheapest-available tablet capture.

5) Are patent cliffs a major risk for levothyroxine?

For tablets, the molecule is widely generic in major markets, so revenue risk is dominated by pricing competition and formulary dynamics rather than new patent expiries.

References

- Food and Drug Administration. (n.d.). FDA Approved Drug Products: Levothyroxine Sodium. FDA. https://www.accessdata.fda.gov/scripts/cder/daf/

- European Medicines Agency. (n.d.). EPARs for levothyroxine-containing products. EMA. https://www.ema.europa.eu/ema/index.jsp?curl=pages/medicines/landing/epar_search.jsp&mid=WC0b01ac058001d124

- U.S. National Library of Medicine. (n.d.). Levothyroxine (drug information and labeling references). PubMed/NCBI Bookshelf. https://www.ncbi.nlm.nih.gov/books/

More… ↓