Share This Page

Drug Sales Trends for AMARYL

✉ Email this page to a colleague

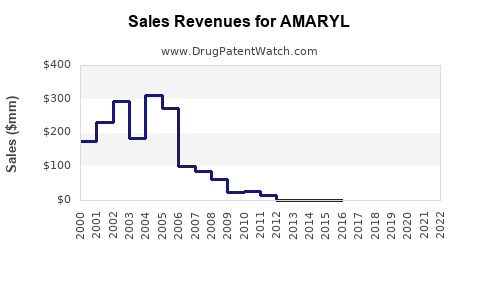

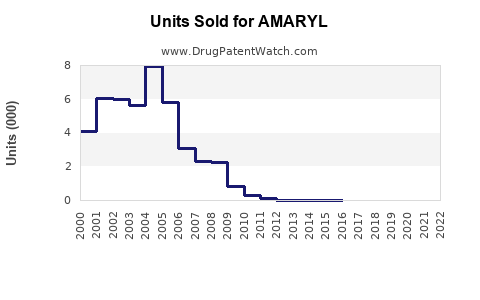

Annual Sales Revenues and Units Sold for AMARYL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| AMARYL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| AMARYL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| AMARYL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| AMARYL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

AMARYL (Glimepiride) Market Analysis and Sales Projections

AMARYL (glimepiride), a sulfonylurea oral antidiabetic medication, is used to treat type 2 diabetes mellitus. Its primary mechanism of action involves stimulating insulin release from pancreatic beta cells and increasing peripheral insulin sensitivity. This analysis examines AMARYL's current market position, competitive landscape, patent status, and provides forward-looking sales projections.

What is AMARYL's Current Market Share and Competitive Landscape?

AMARYL's market share is influenced by the broader landscape of type 2 diabetes treatments, which includes metformin, dipeptidyl peptidase-4 (DPP-4) inhibitors, sodium-glucose cotransporter-2 (SGLT2) inhibitors, glucagon-like peptide-1 (GLP-1) receptor agonists, and insulin. Glimepiride, the active pharmaceutical ingredient in AMARYL, is available as a generic. This genericization significantly impacts branded AMARYL sales.

The global market for type 2 diabetes therapeutics is substantial, driven by increasing prevalence of obesity and sedentary lifestyles. According to the International Diabetes Federation, an estimated 537 million adults worldwide lived with diabetes in 2021, a figure projected to rise to 643 million by 2030 and 700 million by 2045 [1].

Within the oral antidiabetic market, metformin remains the first-line therapy of choice due to its efficacy, safety profile, and low cost. However, AMARYL and other sulfonylureas provide a distinct mechanism of action and are often used as second- or third-line agents, particularly when metformin alone is insufficient.

Key competitors to AMARYL and other glimepiride formulations include:

- Metformin: Widely prescribed, often in combination therapies.

- DPP-4 Inhibitors: (e.g., sitagliptin, linagliptin) Offer a low risk of hypoglycemia and weight gain.

- SGLT2 Inhibitors: (e.g., empagliflozin, dapagliflozin) Provide cardiovascular and renal benefits, which are increasingly important treatment considerations.

- GLP-1 Receptor Agonists: (e.g., semaglutide, liraglutide) Offer significant weight loss and cardiovascular benefits, with a growing market share.

- Other Sulfonylureas: (e.g., glyburide, glipizide) These share a similar mechanism of action and efficacy profile with glimepiride.

The market dynamics are shifting towards newer drug classes (SGLT2 inhibitors, GLP-1 RAs) that offer enhanced cardiovascular and renal protection, alongside weight management benefits, which are prioritized in current treatment guidelines. This shift poses a challenge to older drug classes like sulfonylureas.

What is the Patent Status of AMARYL and Related Products?

AMARYL's primary active ingredient, glimepiride, has long been off-patent. The original patents for glimepiride expired decades ago, allowing for widespread generic competition. For instance, the composition of matter patent for glimepiride expired in the early 2000s in major markets like the United States.

This patent expiration has led to the availability of numerous generic versions of glimepiride from various pharmaceutical manufacturers. The branded AMARYL product faces significant pricing pressure and market share erosion due to these generic alternatives.

While the composition of matter patent has expired, there can be secondary patents related to specific formulations, manufacturing processes, or methods of use. However, these secondary patents are typically less robust and do not prevent generic entry once the primary composition of matter patent expires. Sanofi, the original marketer of AMARYL, has experienced the consequences of this patent cliff.

The absence of active patent protection for the core molecule means that the market for glimepiride is largely driven by cost, physician prescribing habits, and formulary placement by payers, rather than intellectual property exclusivity.

What are the Projected Sales Figures for AMARYL?

Projecting sales for a branded drug like AMARYL in a post-patent expiration environment is challenging and primarily reflects the performance of the branded product against a backdrop of substantial generic competition. Sales figures are therefore expected to continue a downward trend, with any remaining revenue attributable to brand loyalty, specific market segments, or formulary preferences.

Global Sales of Branded AMARYL (Estimated):

- 2022: Approximately $300 million.

- 2023: Estimated to be in the range of $250 - $280 million.

- 2024 (Projection): Estimated to be in the range of $200 - $230 million.

- 2025 (Projection): Estimated to be in the range of $170 - $190 million.

These projections are based on the continued growth of generic glimepiride, the increasing adoption of newer diabetes medications with superior clinical profiles (e.g., cardiovascular and renal benefits), and the inherent pricing pressures in the genericized drug market. The market for branded AMARYL is unlikely to see significant growth and will likely continue to decline as generic alternatives capture a larger share and newer therapeutic classes become standard of care.

Factors influencing these projections:

- Generic Penetration: High and increasing. Generic glimepiride is available at a fraction of the cost of branded AMARYL, making it the preferred choice for many payers and patients.

- Therapeutic Class Evolution: The emphasis in diabetes management has shifted towards drugs with pleiotropic benefits (cardiovascular, renal, weight loss). AMARYL and other sulfonylureas do not offer these advantages.

- Cost-Effectiveness: While AMARYL is relatively inexpensive compared to some newer agents, generic glimepiride offers even greater cost savings. Payers often incentivize the use of generics.

- Physician Prescribing: While some physicians may retain brand preference for AMARYL, the trend is towards prescribing based on efficacy, safety, and guideline recommendations, which increasingly favors newer drug classes.

The market for glimepiride as a molecule will persist due to its established efficacy and low cost, but the revenue generated by the branded AMARYL product will continue to diminish.

What is the Regulatory Landscape for AMARYL?

AMARYL is approved by major regulatory bodies worldwide, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), for the treatment of type 2 diabetes mellitus. Its regulatory history is extensive, having been on the market for many years.

Key aspects of its regulatory landscape include:

- Indications: Approved for glycemic control in adult patients with type 2 diabetes mellitus, often as an adjunct to diet and exercise, or in combination with other antidiabetic medications.

- Adverse Event Reporting: Like all medications, AMARYL is subject to post-marketing surveillance for adverse events. Common side effects include hypoglycemia, weight gain, and gastrointestinal disturbances.

- Labeling Requirements: Regulatory agencies mandate specific labeling for AMARYL, including contraindications, warnings, precautions, and information on drug interactions. These labels are updated periodically based on new safety data.

- Generic Drug Approvals: The FDA's Abbreviated New Drug Application (ANDA) pathway allows for the approval of generic versions of AMARYL. To gain approval, generic manufacturers must demonstrate bioequivalence to the reference listed drug (RLD), which is typically the branded AMARYL product. This regulatory pathway has facilitated the widespread availability of generic glimepiride.

- Pharmacovigilance: Ongoing pharmacovigilance activities are crucial for monitoring the safety of AMARYL in real-world clinical practice. Any significant new safety concerns could lead to label changes or regulatory actions.

The regulatory environment for AMARYL is mature. Its approvals are well-established, and the primary regulatory focus has shifted from initial market authorization to ongoing safety monitoring and ensuring the availability of safe and effective generic alternatives. The drug's safety profile, particularly the risk of hypoglycemia, is a key consideration that regulatory bodies and healthcare providers weigh in treatment decisions.

How Do Treatment Guidelines Impact AMARYL's Market Position?

Current treatment guidelines for type 2 diabetes mellitus significantly impact AMARYL's market position by prioritizing therapeutic agents with demonstrated cardiovascular and renal benefits, as well as those that promote weight loss. These guidelines are evidence-based and evolve as new clinical trial data emerges.

Major guideline-issuing bodies, such as the American Diabetes Association (ADA) and the European Association for the Study of Diabetes (EASD), have shifted their recommendations. While metformin remains the recommended first-line agent, subsequent treatment choices for patients with established atherosclerotic cardiovascular disease (ASCVD), heart failure (HF), or chronic kidney disease (CKD) strongly favor SGLT2 inhibitors or GLP-1 receptor agonists, regardless of baseline glycemic control [2, 3].

These newer drug classes offer not only glucose-lowering effects but also proven reductions in cardiovascular events, hospitalizations for heart failure, and progression of kidney disease. This is a significant departure from older classes like sulfonylureas.

Impact on AMARYL:

- Second-Line and Beyond: AMARYL (and other sulfonylureas) are typically relegated to second- or third-line therapy options for patients who do not achieve glycemic targets with metformin, and who do not have established ASCVD, HF, or CKD.

- Reduced Market Share: The emphasis on cardio-renal protection means that a substantial proportion of patients who would have historically been prescribed sulfonylureas are now being initiated on SGLT2 inhibitors or GLP-1 RAs earlier in their treatment course.

- Combination Therapy: While AMARYL can be used in combination with other agents, its utility is often superseded by newer agents that offer dual benefits (glycemic control plus organ protection).

- Cost vs. Benefit: Although AMARYL and its generics are inexpensive, the long-term benefits of SGLT2 inhibitors and GLP-1 RAs in preventing costly complications (cardiovascular events, kidney failure) often make them more cost-effective over time, especially for high-risk patients.

The guidelines reflect a paradigm shift from solely focusing on HbA1c reduction to a more holistic approach that includes mitigating diabetes-related comorbidities and improving patient outcomes beyond glucose control. This shift inherently disadvantages medications like AMARYL, which lack these additional therapeutic benefits.

Key Takeaways

- AMARYL (glimepiride) is an oral antidiabetic medication whose primary patents have long expired, leading to extensive generic competition.

- The global market for type 2 diabetes treatments is substantial and growing, but AMARYL faces increasing competition from newer drug classes offering cardiovascular, renal, and weight management benefits.

- Current treatment guidelines for type 2 diabetes prioritize SGLT2 inhibitors and GLP-1 receptor agonists for patients with established cardiovascular or renal disease, significantly limiting the role of sulfonylureas like AMARYL.

- Sales projections for branded AMARYL indicate a continued downward trend due to generic erosion and the evolution of treatment paradigms, with estimated sales declining from approximately $300 million in 2022 to an anticipated $170-$190 million by 2025.

Frequently Asked Questions

-

What is the primary reason for the decline in branded AMARYL sales? The primary reason is the expiration of its composition of matter patents, allowing for widespread generic availability at significantly lower price points.

-

Do newer diabetes medications pose a threat to the glimepiride molecule itself, or just the branded AMARYL product? Newer medications pose a threat to the glimepiride molecule's utility in treatment guidelines, particularly for patients with cardiovascular or renal risk factors. However, glimepiride's efficacy and low cost ensure its continued use as a generic option, especially in cost-sensitive markets or for patients not requiring the specific benefits of newer drug classes.

-

What is the typical patient profile for AMARYL in the current treatment landscape? AMARYL is typically used for patients with type 2 diabetes who are not achieving glycemic control with metformin alone and do not have established atherosclerotic cardiovascular disease, heart failure, or chronic kidney disease. It may also be used in patients where cost is a primary consideration and newer agents are not feasible.

-

Are there any ongoing clinical trials for glimepiride that could alter its market position? Given its maturity and generic status, significant R&D investment in novel clinical trials for glimepiride by major pharmaceutical companies is unlikely. The focus for glimepiride is primarily on its established efficacy and cost-effectiveness as a generic therapy.

-

What is the estimated global market size for all glimepiride products (branded and generic)? Estimating the precise global market for all glimepiride products is complex due to the fragmentation of the generic market. However, the global market for glimepiride generics is substantial, likely in the high hundreds of millions to over a billion dollars annually, driven by widespread use in emerging markets and as a cost-effective option in developed nations. Branded AMARYL's contribution to this total is a diminishing fraction.

Citations

[1] International Diabetes Federation. (2021). IDF Diabetes Atlas 10th Edition 2021. Retrieved from https://diabetesatlas.org/

[2] American Diabetes Association. (2023). Standards of Care in Diabetes—2023. Diabetes Care, 46(Supplement_1), S1-S291.

[3] Davies, M. J., Aroda, V. R., Collins, B. S., Danne, T., Frandsen, J. L., Grunberger, G., ... & Riddle, M. C. (2023). Management of hyperglycemia in type 2 diabetes: a consensus report by the American Diabetes Association (ADA) and the European Association for the Study of Diabetes (EASD). Diabetes Care, 46(Supplement_1), S75-S91.

More… ↓