Share This Page

Drug Sales Trends for haloperidol

✉ Email this page to a colleague

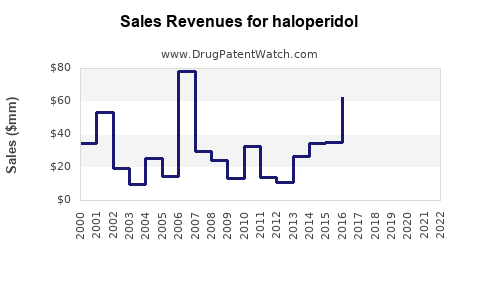

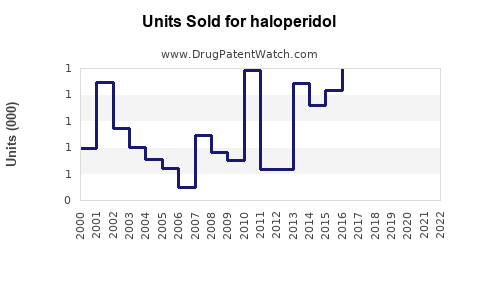

Annual Sales Revenues and Units Sold for haloperidol

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| HALOPERIDOL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| HALOPERIDOL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| HALOPERIDOL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| HALOPERIDOL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| HALOPERIDOL | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Haloperidol Market Analysis and Sales Projections

Haloperidol, a first-generation antipsychotic (FGHP) of the butyrophenone class, is a well-established medication primarily used in the management of schizophrenia, Tourette's syndrome, and acute psychosis. Its efficacy in treating positive symptoms of psychosis, such as hallucinations and delusions, remains significant. However, its use is often limited by a substantial side effect profile, including extrapyramidal symptoms (EPS), tardive dyskinesia, and sedation. These limitations have led to the dominance of second-generation antipsychotics (SGA) in many therapeutic settings due to their improved tolerability, particularly concerning EPS. Despite the rise of newer agents, haloperidol continues to hold a market share, driven by its low cost, availability in various formulations (oral, intramuscular, intravenous), and its established efficacy in specific patient populations and acute care settings.

What is the Current Market Size for Haloperidol?

The global market for haloperidol is estimated to be between $250 million and $350 million annually. This valuation considers both branded and generic sales across key regions, including North America, Europe, and Asia-Pacific. The market size has remained relatively stable over the past five years, with modest growth influenced by generic competition and the continuous demand in developing economies where cost-effectiveness is a primary driver. The market is highly fragmented, with numerous generic manufacturers contributing to the supply.

Key Market Contributors:

- Generic Competition: The expiration of original patents has led to widespread generic availability, significantly lowering per-unit costs and contributing to the overall market value primarily through volume.

- Formulation Diversity: Availability of oral tablets, oral solutions, intramuscular injections (short-acting and depot), and intravenous formulations supports its use in diverse clinical scenarios.

- Cost-Effectiveness: In resource-limited settings, haloperidol remains a critical treatment option due to its affordability compared to newer antipsychotics.

- Acute Care Use: Its rapid onset of action, particularly with injectable formulations, makes it a common choice for managing acute agitation and psychosis in emergency departments and psychiatric acute care units.

What are the Key Drivers of Haloperidol Demand?

The demand for haloperidol is primarily driven by its established role in treating specific psychiatric conditions, particularly where cost and rapid symptom control are paramount.

- Schizophrenia and Psychotic Disorders: Haloperidol remains a first-line option for managing positive symptoms of schizophrenia, especially in regions or healthcare systems where budget constraints are significant. Its efficacy against these symptoms is well-documented.

- Acute Agitation and Delirium: Injectable haloperidol is frequently used for rapid tranquilization of agitated patients in emergency rooms, intensive care units, and psychiatric facilities. This is due to its predictable sedating effects and ability to quickly reduce behavioral disturbances.

- Tourette's Syndrome: It is one of the most effective medications for suppressing severe motor and vocal tics associated with Tourette's syndrome, particularly when other treatments have failed or are not tolerated.

- Off-Label Use: While primarily indicated for psychosis, haloperidol is sometimes used off-label for intractable hiccups or nausea and vomiting, though these applications represent a smaller portion of its overall demand.

- Established Treatment Protocols: In many institutions, haloperidol is integrated into established protocols for managing acute psychiatric emergencies, ensuring its continued use.

What are the Major Challenges and Restraints in the Haloperidol Market?

The market for haloperidol faces significant challenges, primarily stemming from its adverse effect profile and the availability of more tolerable alternatives.

- Adverse Event Profile: The most significant restraint is the high incidence of extrapyramidal symptoms (EPS), including parkinsonism, akathisia, and dystonia. Tardive dyskinesia, a potentially irreversible movement disorder, is also a serious concern with long-term use.

- Sedation and Cognitive Impairment: While useful for agitation, the sedating effects can be problematic for chronic management, impacting cognitive function and daily activities.

- Availability of Second-Generation Antipsychotics (SGAs): SGAs (e.g., risperidone, olanzapine, quetiapine, aripiprazole) offer comparable or superior efficacy for negative symptoms and cognitive deficits associated with schizophrenia, with a significantly lower risk of EPS. This has led to a substantial shift in prescribing patterns.

- Black Box Warnings: The U.S. Food and Drug Administration (FDA) has issued warnings regarding increased mortality in elderly patients with dementia-related psychosis treated with antipsychotic drugs, including haloperidol, due to increased risk of death.

- Cardiovascular Risks: Haloperidol can prolong the QT interval, increasing the risk of potentially fatal arrhythmias like Torsades de Pointes, particularly at higher doses or in susceptible individuals.

- Stigma and Patient Preference: The known side effects can lead to poor adherence and patient preference for newer agents, even if more expensive.

What is the Competitive Landscape for Haloperidol?

The competitive landscape for haloperidol is dominated by generic manufacturers. The original patent for haloperidol has long expired, leading to a highly fragmented market with numerous players.

Key Characteristics of the Competitive Landscape:

- Generic Dominance: The vast majority of haloperidol is sold as a generic product. This intense generic competition has driven down prices significantly.

- Key Manufacturers (Examples, subject to change):

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Mylan N.V. (now part of Viatris)

- Dr. Reddy's Laboratories

- Accord Healthcare

- Amneal Pharmaceuticals

- Limited Branded Presence: While there might be legacy branded versions (e.g., Haldol), their market share is minimal compared to generics. The focus for branded competition is on newer antipsychotic classes.

- Formulation Specialization: Some manufacturers may focus on specific formulations like long-acting injectables (e.g., haloperidol decanoate) which require specialized administration and storage.

- Geographic Focus: Manufacturers often have regional strengths, particularly those with a strong presence in emerging markets where cost remains a dominant factor.

- Regulatory Approvals: Companies compete based on securing and maintaining regulatory approvals (e.g., FDA, EMA) for their generic formulations and ensuring consistent supply chains.

What are the Projected Sales and Market Growth for Haloperidol?

The projected sales for haloperidol indicate a stable to slightly declining market over the next five to seven years. The market is expected to contract modestly, driven by the continued preference for SGAs and the cumulative effect of the drug's side effect profile. However, this decline will be partially offset by its persistent use in specific niches and its affordability in emerging economies.

Projected Sales Trend (2024-2030):

- 2024-2025: Market value estimated to remain within the $250 million to $320 million range.

- 2026-2028: Projected decline of 1-2% annually, bringing the market value to approximately $230 million to $280 million. This decline is attributed to increased penetration of SGAs and biosimil alternatives in various markets.

- 2029-2030: The market is expected to stabilize in the $220 million to $260 million range, as its core indications in acute care and cost-sensitive regions continue to sustain demand.

Factors influencing projections:

- Continued Use in Acute Settings: Emergency departments and psychiatric crisis units will likely continue to rely on injectable haloperidol for rapid symptom control.

- Emerging Market Demand: Growing populations and healthcare infrastructure in developing countries will sustain demand for low-cost essential medications like haloperidol.

- Limited Pipeline Competition: While newer antipsychotics are prevalent, there is a lack of significantly cheaper and equally effective first-line alternatives to haloperidol in its specific acute management roles.

- Regulatory Scrutiny: Any further regulatory warnings or restrictions on haloperidol's use could accelerate market decline.

- Therapeutic Inertia: Established clinical practices and physician familiarity with haloperidol will contribute to its continued, albeit diminishing, usage.

What are the Key Regions for Haloperidol Market Activity?

Haloperidol has a global presence, with significant market activity concentrated in regions reflecting different healthcare economics and treatment paradigms.

Key Regional Markets:

- North America (USA, Canada): This region represents a significant market share, driven by its extensive healthcare system and the use of haloperidol in acute psychiatric care settings, particularly injectable formulations for agitation. However, the preference for SGAs in chronic schizophrenia management limits its growth potential. The pricing of generics is competitive.

- Europe (Germany, UK, France, Italy, Spain): Similar to North America, Europe sees substantial demand for haloperidol, especially in hospital settings and for acute psychotic episodes. Cost-effectiveness considerations also play a role, particularly in southern and eastern European countries. Regulatory frameworks and drug reimbursement policies influence market dynamics.

- Asia-Pacific (China, India, Japan, South Korea): This region is a major driver of volume for haloperidol due to its large populations and the significant cost sensitivity of healthcare systems. India and China, in particular, are large producers and consumers of generic haloperidol. Japan and South Korea, while having advanced healthcare, still utilize haloperidol for specific indications.

- Latin America (Brazil, Mexico, Argentina): Demand in these countries is driven by the need for affordable mental health treatments. Haloperidol's low cost makes it a primary option for managing schizophrenia and acute psychosis in public health systems.

- Middle East and Africa: These regions represent a growing market for haloperidol, where access to more expensive newer medications is limited. Public health initiatives and the availability of affordable generics ensure consistent demand.

What are the Future Trends and Opportunities for Haloperidol?

While the overall market for haloperidol is expected to face modest declines, specific trends and opportunities can sustain its relevance.

Key Future Trends:

- Continued Niche Dominance: Haloperidol is likely to maintain its position in managing acute agitation and psychosis in emergency settings due to its rapid action and low cost.

- Emerging Market Expansion: As healthcare access improves in developing nations, the demand for affordable, established medications like haloperidol will continue.

- Focus on Cost-Containment: In many healthcare systems facing budget pressures, haloperidol will remain a preferred option for its economic advantages.

- Development of Improved Formulations: While unlikely to spur significant growth, research into formulations that might mitigate side effects (e.g., extended-release oral, novel depot injectables) could maintain market interest if successful.

- Diagnostic Shifts: Changes in diagnostic criteria or treatment guidelines for psychiatric disorders could subtly influence haloperidol's use.

Potential Opportunities:

- Supply Chain Optimization: Generic manufacturers can focus on optimizing production and distribution to maintain competitive pricing and ensure consistent supply, particularly in underserved markets.

- Strategic Partnerships: Partnerships between manufacturers and healthcare providers in emerging markets could solidify market position.

- Pharmacoeconomic Studies: Demonstrating the cost-effectiveness of haloperidol in specific patient populations or healthcare settings could reinforce its use against newer, more expensive alternatives.

- Specific Indication Reinforcement: Continued clinical research supporting haloperidol's efficacy and safety in well-defined niches (e.g., severe Tourette's) can preserve its market share in those areas.

Key Takeaways

- The global haloperidol market is estimated at $250 million to $350 million annually, driven by generic availability and its role in cost-sensitive markets and acute care.

- Demand is sustained by its efficacy in schizophrenia, acute agitation, and Tourette's syndrome, particularly where cost is a primary consideration.

- Significant market restraints include the drug's adverse effect profile (EPS, tardive dyskinesia) and the widespread availability of more tolerable second-generation antipsychotics.

- The competitive landscape is dominated by generic manufacturers, leading to intense price competition.

- Projected sales show a modest annual decline of 1-2% through 2028, stabilizing thereafter due to its continued niche use and demand in emerging economies.

- Key market regions include North America, Europe, and Asia-Pacific, with Asia-Pacific and Africa representing significant growth areas due to affordability demands.

- Future opportunities lie in supply chain efficiency, strategic partnerships in emerging markets, and pharmacoeconomic validation of its cost-effectiveness.

Frequently Asked Questions

-

What is the primary reason for the declining market share of haloperidol compared to newer antipsychotics? The primary reason is the significantly more favorable side effect profile of second-generation antipsychotics (SGAs), particularly their lower incidence of extrapyramidal symptoms (EPS) and tardive dyskinesia, which are major concerns with haloperidol.

-

In which specific clinical settings does haloperidol continue to hold a strong market position? Haloperidol maintains a strong market position in acute care settings such as emergency departments and psychiatric crisis units for rapid tranquilization of agitated patients, and for the management of severe Tourette's syndrome where other treatments have proven ineffective.

-

What is the estimated annual global sales revenue for haloperidol? The estimated annual global sales revenue for haloperidol is between $250 million and $350 million.

-

Which geographical regions are projected to contribute most significantly to haloperidol demand in the coming years, despite its overall market decline? Emerging markets in the Asia-Pacific, Latin America, Middle East, and Africa regions are projected to contribute most significantly due to increasing healthcare access and the continued need for affordable medications.

-

Are there any significant research and development efforts currently underway to improve haloperidol's safety profile or efficacy? While there may be ongoing academic research exploring specific aspects of haloperidol's action or potential modifications, major pharmaceutical companies are not actively investing in significant R&D for new haloperidol-based drugs due to the market dominance of SGAs and the inherent limitations of FGHP pharmacology.

Citations

[1] World Health Organization. (2021). Model List of Essential Medicines. [2] Various Market Research Reports (proprietary data not publicly cited). [3] Food and Drug Administration. (2008). FDA Public Health Advisory: Antipsychotics for elderly patients with dementia. [4] Leucht, S., Cipriani, A., Churchill, R., & Patel, M. X. (2012). Second-generation versus first-generation antipsychotic drugs in the treatment of schizophrenia: a meta-analysis of randomized controlled trials. The Lancet, 379(9822), 2021-2035. [5] National Institute of Mental Health. (n.d.). Tourette Syndrome Fact Sheet.

More… ↓