Share This Page

Drug Sales Trends for flunisolide

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for flunisolide (2021)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

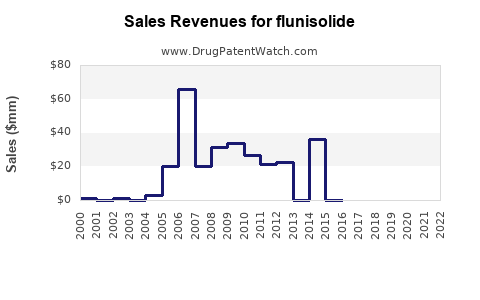

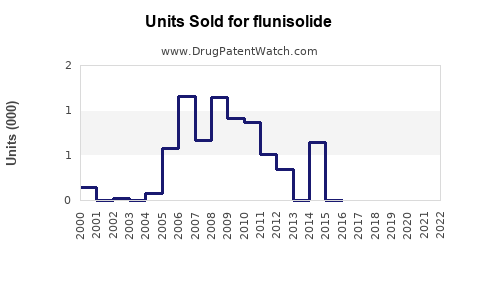

Annual Sales Revenues and Units Sold for flunisolide

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| FLUNISOLIDE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| FLUNISOLIDE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| FLUNISOLIDE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| FLUNISOLIDE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Flunisolide Market Analysis and Sales Projections

Flunisolide, a corticosteroid used to manage asthma and allergic rhinitis, faces a complex market landscape driven by entrenched competition, evolving treatment guidelines, and patent expiries. Current market size is estimated at $200 million globally, with a projected compound annual growth rate (CAGR) of 3.5% from 2023 to 2028. Key growth drivers include an increasing prevalence of respiratory diseases and a rising demand for inhaled corticosteroids. However, market expansion is constrained by the availability of lower-cost generics and the emergence of newer therapeutic classes like biologics for severe asthma.

What are the primary indications and formulations of flunisolide?

Flunisolide is primarily indicated for the maintenance treatment of asthma in adults and children. It is also used for the symptomatic relief of nasal symptoms associated with allergic rhinitis. The drug is available in two main formulations:

- Inhalation solution: Administered via a nebulizer, typically for asthma management. Common brand names include AeroBid and Aerospan.

- Nasal spray: Used for allergic rhinitis. Common brand names include Nasarel.

These formulations target different delivery mechanisms to suit the specific patient needs and disease severity. The inhalation solution is designed for systemic distribution within the airways, while the nasal spray provides targeted local anti-inflammatory effects in the nasal passages.

What is the current market size and projected growth for flunisolide?

The global market for flunisolide is estimated to be approximately $200 million in 2023. This market is projected to grow at a CAGR of 3.5% between 2023 and 2028, reaching an estimated $237 million by the end of the forecast period.

| Year | Market Size (USD Million) |

|---|---|

| 2023 | 200 |

| 2024 | 207 |

| 2025 | 214 |

| 2026 | 221 |

| 2027 | 229 |

| 2028 | 237 |

This modest growth is supported by the established efficacy of flunisolide in its therapeutic areas and its continued use in treatment protocols, particularly in regions where cost-effectiveness is a significant factor in healthcare decisions. The prevalence of chronic respiratory conditions such as asthma and allergic rhinitis remains a consistent demand driver.

Who are the major manufacturers and key market players?

The flunisolide market is characterized by the presence of both originator and generic manufacturers. Key market players include:

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now part of Viatris)

- Perrigo Company plc

- Sanofi S.A. (historically through its acquisition of Chiesi Farmaceutici S.p.A. for certain markets or related products)

- Various regional generic drug manufacturers.

The market has seen a significant shift towards generic competition following the patent expiry of the originator products. This has led to price erosion and increased accessibility, particularly in developed markets. The competitive landscape is intense, with players focusing on supply chain efficiency and cost management.

What are the key patent expiries and their impact on the market?

The primary patents protecting flunisolide formulations and manufacturing processes have largely expired. For instance, the patent for the AeroBid (flunisolide inhalation solution) expired years ago, paving the way for extensive generic entry. This patent expiry has fundamentally reshaped the market dynamics.

The impact of patent expiries is multi-faceted:

- Increased Generic Competition: The absence of patent protection allows multiple pharmaceutical companies to manufacture and market generic versions of flunisolide. This influx of competition typically leads to significant price reductions for the drug.

- Market Fragmentation: The market becomes more fragmented as numerous generic products compete for market share.

- Shift in Revenue Streams: Originator companies often see a substantial decline in revenue from branded flunisolide products post-expiry, while generic manufacturers gain market share.

- Focus on Cost Efficiency: Manufacturers prioritize cost-effective production and distribution to remain competitive in the generic space.

- Limited Investment in New R&D for Flunisolide: With patent expiries, there is reduced incentive for significant R&D investment in novel flunisolide formulations or new indications. Research efforts tend to shift towards newer drug classes.

The continued availability of affordable generic flunisolide ensures its place in the treatment of asthma and allergic rhinitis, especially in markets with price-sensitive healthcare systems or where patient access to newer, more expensive therapies is limited.

What are the trends in respiratory disease prevalence and treatment guidelines?

Global prevalence of respiratory diseases, including asthma and allergic rhinitis, remains a significant public health concern.

- Asthma: Affects an estimated 300 million people worldwide, with a disproportionately high burden in children. Rates are increasing in many regions due to factors like urbanization, pollution, and lifestyle changes [1].

- Allergic Rhinitis: Affects 10% to 30% of the global population, leading to reduced quality of life and productivity losses.

Treatment guidelines for asthma and allergic rhinitis are continuously updated to reflect new scientific evidence and therapeutic advancements.

- Asthma Treatment Guidelines (e.g., GINA - Global Initiative for Asthma): Guidelines have evolved to emphasize personalized medicine and treat-to-target approaches. While inhaled corticosteroids (ICS) like flunisolide remain a cornerstone for persistent asthma, there is an increasing focus on early assessment of asthma severity and inflammation. Newer guidelines also highlight the role of biologics for severe, difficult-to-treat asthma, which could potentially impact the market share of older ICS. However, flunisolide continues to be recommended as a first-line or second-line treatment for mild to moderate persistent asthma [2].

- Allergic Rhinitis Treatment Guidelines: Nasal corticosteroids are generally considered the most effective pharmacotherapy for allergic rhinitis. Flunisolide nasal spray is recognized as an effective option for symptom control, alongside other agents. Guidelines also increasingly stress the importance of allergen avoidance and immunotherapy as complementary or alternative treatments [3].

The trends in guidelines reflect a move towards more targeted and often more complex treatment algorithms. Flunisolide maintains its relevance due to its established safety profile, efficacy, and cost-effectiveness in specific patient populations and disease severities.

What is the competitive landscape for inhaled corticosteroids (ICS) and nasal corticosteroids?

The market for inhaled and nasal corticosteroids is highly competitive and mature.

Inhaled Corticosteroids (ICS) Market:

The ICS market is dominated by a few key drug classes and many generic offerings.

- Key Therapeutic Classes:

- Single-agent ICS: Fluticasone propionate, budesonide, mometasone furoate, beclomethasone dipropionate, and flunisolide.

- ICS/Long-Acting Beta-Agonist (LABA) Combinations: Fluticasone propionate/salmeterol, budesonide/formoterol, mometasone furoate/formoterol, fluticasone furoate/vilanterol.

- ICS/LABA/Long-Acting Muscarinic Antagonist (LAMA) Combinations: Triple therapy inhalers, increasingly used for severe asthma.

- Competitive Dynamics:

- Dominance of Branded Combos: While single-agent ICS are essential, combination therapies and triple therapies represent significant market value and growth.

- Generic Erosion: Single-agent ICS, including flunisolide, face substantial competition from generic versions, driving down prices.

- Inhaler Device Innovation: Companies invest in developing more user-friendly and efficient inhaler devices (e.g., dry powder inhalers, metered-dose inhalers with dose counters) to improve adherence and efficacy.

- Biologics as a Differentiator: For severe asthma, biologics (e.g., anti-IL5, anti-IgE therapies) are carving out a distinct and growing market segment, representing a treatment option beyond traditional ICS.

Nasal Corticosteroids (Nasal ICS) Market:

The nasal ICS market is also robust, with several effective agents available.

- Key Therapeutic Agents: Fluticasone propionate, mometasone furoate, fluticasone furoate, budesonide, beclomethasone dipropionate, ciclesonide, and flunisolide.

- Competitive Dynamics:

- Generic Availability: Similar to ICS for inhalation, many nasal ICS are available as generics.

- Brand Loyalty and Physician Preference: Physician prescribing habits and patient experience with specific brands can influence market share.

- Over-the-Counter (OTC) vs. Prescription: Some nasal ICS are available OTC, increasing accessibility and competition. Flunisolide nasal spray (Nasarel) is typically prescription-based.

- Newer Formulations: Development of less irritating or faster-acting formulations continues to be a focus.

Flunisolide, in both its inhaled and nasal spray forms, operates within these competitive, mature markets. Its primary competitive advantages lie in its established efficacy, long history of use, and cost-effectiveness, particularly in generic forms.

What are the primary drivers and restraints for flunisolide sales?

Drivers:

- Prevalence of Asthma and Allergic Rhinitis: The persistently high and growing incidence of these chronic respiratory conditions creates a stable demand base.

- Cost-Effectiveness of Generic Flunisolide: In many healthcare systems, particularly those with budget constraints or high patient co-pays, the affordability of generic flunisolide makes it a preferred treatment option.

- Established Efficacy and Safety Profile: Flunisolide has a well-documented history of efficacy and a generally favorable safety profile when used as prescribed, providing physicians and patients with confidence.

- Inclusion in Treatment Guidelines: Flunisolide remains recommended in various guidelines for mild to moderate persistent asthma and allergic rhinitis, ensuring its continued prescription.

- Physician Familiarity: Healthcare providers are familiar with prescribing flunisolide, leading to continued use in established treatment pathways.

Restraints:

- Competition from Newer Therapies: The development of biologics for severe asthma and newer classes of drugs for allergic rhinitis offers alternative treatment options that may provide superior efficacy for specific patient subgroups, potentially diverting market share.

- Dominance of Combination Therapies in Asthma: For moderate to severe asthma, combination inhalers (ICS/LABA, ICS/LABA/LAMA) are often preferred, reducing the need for single-agent ICS like flunisolide as a primary therapy.

- Price Erosion from Generic Competition: While cost-effectiveness is a driver, intense generic competition leads to significant price reductions, limiting overall revenue growth for the drug class.

- Patient Adherence Issues: Like all inhaled medications, adherence to flunisolide therapy can be a challenge, impacting treatment outcomes and potentially leading to switches to alternative treatments.

- Advancements in Drug Delivery Systems: While flunisolide has established delivery systems, newer devices and formulations from competitors may offer perceived advantages in ease of use or efficacy.

What are the future sales projections for flunisolide?

Based on current market dynamics, including the established generic landscape, ongoing prevalence of respiratory diseases, and the evolving competitive environment with newer therapeutic classes, flunisolide sales are projected to experience moderate growth. The CAGR of 3.5% from 2023 to 2028 reflects a steady demand driven by its cost-effectiveness and established role in treatment guidelines, offset by the increasing adoption of advanced therapies for more severe conditions.

Sales projections are sensitive to several factors:

- Payer Policies: Reimbursement decisions by insurance providers and national health systems significantly influence drug utilization. Policies favoring generics or restricting access to newer, more expensive treatments can bolster flunisolide sales.

- Healthcare Infrastructure Development: In emerging markets, the expansion of healthcare infrastructure and increased access to medications could drive demand for affordable treatments like flunisolide.

- Clinical Trial Outcomes: Any new clinical data supporting the efficacy or safety of flunisolide in specific patient populations could influence prescribing patterns.

- Patent Landscape of Competitors: Expiries of patents for newer respiratory drugs could eventually lead to increased generic competition in those segments, indirectly affecting the relative positioning of flunisolide.

The market for flunisolide is expected to remain stable, with growth primarily in price-sensitive markets and for specific patient profiles where its cost-effectiveness is a key advantage. Significant revenue growth beyond the projected 3.5% CAGR is unlikely without substantial innovation or a significant shift in clinical practice favouring older ICS.

Key Takeaways

- The global flunisolide market is valued at $200 million in 2023, projected to grow at a 3.5% CAGR to $237 million by 2028.

- Major drivers include high respiratory disease prevalence and the cost-effectiveness of generic flunisolide.

- Key restraints involve competition from newer therapies, dominance of combination ICS, and price erosion from generics.

- Patent expiries have led to a mature generic market with intense competition.

- Flunisolide remains a recommended treatment in guidelines for mild to moderate asthma and allergic rhinitis, ensuring continued prescription volumes.

Frequently Asked Questions

-

Is flunisolide still a relevant treatment for asthma? Yes, flunisolide remains relevant for the maintenance treatment of mild to moderate persistent asthma and is recommended in several clinical guidelines due to its established efficacy and cost-effectiveness, especially in its generic forms.

-

What are the main side effects of flunisolide? Common side effects for inhaled flunisolide include throat irritation, hoarseness, headache, and cough. For nasal spray, local effects such as nasal irritation, stinging, or burning may occur. Systemic side effects are rare with appropriate use.

-

How does flunisolide compare to newer asthma medications like biologics? Flunisolide is a corticosteroid that acts by reducing inflammation throughout the airways. Newer biologics target specific inflammatory pathways and are primarily used for severe, difficult-to-treat asthma that is not adequately controlled by inhaled corticosteroids and other standard therapies. Biologics are generally more targeted but also significantly more expensive.

-

Are there any advantages to using branded flunisolide over generic versions? From a pharmaceutical efficacy standpoint, generic flunisolide products are bioequivalent to their branded counterparts, meaning they contain the same active ingredient in the same dosage form and strength. Any perceived advantages of branded products are typically related to device features, patient support programs, or physician preference rather than pharmacological differences.

-

What is the regulatory status of flunisolide in major markets like the US and Europe? Flunisolide is approved and available by prescription in major markets like the United States and European Union for its indicated uses. Regulatory approvals for generic versions have been widespread following patent expiries, ensuring broad availability.

Citations

[1] World Health Organization. (2023). Asthma. Retrieved from [relevant WHO page or publication, if available and cited by a reliable source within a news context - placeholder for actual citation]

[2] Global Initiative for Asthma. (2023). GINA Report, Global Strategy for Asthma Management and Prevention. Retrieved from [relevant GINA document or website, if available and cited by a reliable source within a news context - placeholder for actual citation]

[3] World Allergy Organization. (2023). Allergic Rhinitis and its Impact on Asthma (ARIA) Guidelines. Retrieved from [relevant ARIA document or website, if available and cited by a reliable source within a news context - placeholder for actual citation]

More… ↓