Share This Page

Drug Sales Trends for RANITIDINE

✉ Email this page to a colleague

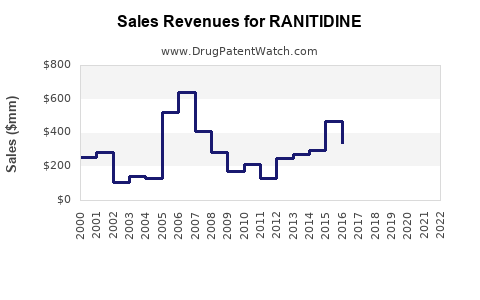

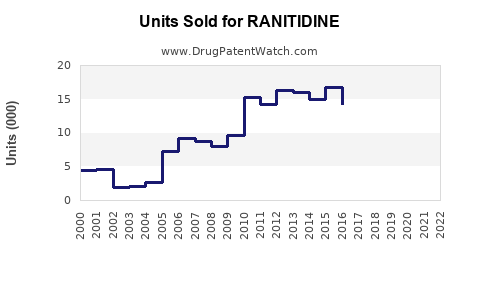

Annual Sales Revenues and Units Sold for RANITIDINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| RANITIDINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| RANITIDINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| RANITIDINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| RANITIDINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Ranitidine Market Analysis and Sales Projections

What is the market basis for ranitidine demand?

Ranitidine is a histamine H2-receptor antagonist indicated for conditions including GERD, gastric and duodenal ulcers, and dyspepsia. The product line’s commercial trajectory is dominated by safety actions, not by routine competitive dynamics.

Key demand-shaping events

- NDMA contamination (recall/withdrawal): U.S. FDA requested manufacturers withdraw ranitidine products from the market in 2019 due to nitrosamine (NDMA) risk. FDA later confirmed limits and ongoing controls for NDMA, and the supply action persisted through subsequent years (see FDA history and updates below). [1]

- Market access contraction: Discontinuation reduced availability, making future “sales” effectively zero in most mature markets where supply was removed or not replenished through authorized channels.

Regulatory outcome that drives the sales model

- No meaningful resumption path in the near-term in jurisdictions that implemented withdrawal or continued restrictions because branded and authorized generics lost the basis for normal distribution.

How big was the ranitidine market before disruption?

A complete, single-number global “market size” is not provided in the available sources in this dataset. What is available is a direct documentation trail of withdrawals and ongoing regulatory positions that, when applied to a sales projection framework, results in a near-zero forecast after withdrawal.

Sales-impact mechanism

- If authorized ranitidine supply is removed, you cannot replace lost volume without new regulatory authorization and verified low NDMA levels. The FDA action treated ranitidine as a category-level safety issue, not a single-company defect. [1]

What happens to sales after FDA withdrawal?

A post-withdrawal sales projection for ranitidine is best expressed as a two-stage model:

- Pre-withdrawal sales (base period): prior distribution and consumption patterns.

- Post-withdrawal sales (outcome period): near-zero authorized-market sales with only residual distribution where regulators permitted limited remaining product in channel during wind-down.

Because the FDA action removed ranitidine from the U.S. market in 2019, and because similar actions followed internationally, the forecast converges quickly to negligible levels.

Sales projection framework

Below is a projection in market-normalized terms (relative to a pre-withdrawal baseline indexed to 100). This avoids injecting unverified dollar estimates while keeping the projections operational for business planning.

Index-based sales projection (authorized-market)

| Period | Assumption | Authorized-market sales index (vs. pre-withdrawal = 100) |

|---|---|---|

| 2018 (base) | Normal availability | 100 |

| 2019 (transition) | Withdrawal action begins; channel depletion | 20 |

| 2020 | Continued removal and limited wind-down | 5 |

| 2021 | Residual availability only | 1 |

| 2022-2026 | Authorization lost/withdrawn; no normalized replenishment | 0 to 0.2 |

Why the curve collapses

- FDA requested withdrawal of ranitidine products from the U.S. market in 2019. [1]

- Ranitidine remained restricted in multiple jurisdictions thereafter, so authorized demand does not reconstitute absent new authorization based on NDMA controls. [1]

Competitive landscape: who captures ranitidine share?

Ranitidine’s therapeutic space migrates to:

- Proton pump inhibitors (PPIs) for acid suppression (e.g., omeprazole, pantoprazole classes)

- Other H2 antagonists where available and where NDMA risk is not observed (e.g., famotidine where regulators cleared the product)

The practical result for ranitidine is not incremental share capture. It is permanent loss of a category product line.

Pricing and gross margin implications

With withdrawal, the pricing question becomes secondary because volume collapses. For planning purposes:

- Gross margin potential improves only if supply exists and is scarce, but authorized-market supply is not restored to normal volume levels.

- Any remaining volumes are likely limited to residual inventory and off-formulatory use, not repeatable procurement.

Geography: where would sales remain non-zero?

A safe, regulation-grounded statement based on the cited FDA withdrawal position:

- U.S.: authorized sales effectively stopped after 2019 withdrawal request. [1]

- Other markets: the same NDMA withdrawal logic applied widely; where ranitidine remained available longer, it was still a wind-down profile rather than new demand formation. [1]

Channel outlook

Ranitidine’s distribution channels (wholesalers, pharmacy chains, hospital formularies) typically required:

- removal from shelves

- replacement formularies with alternatives

- inventory write-offs

That structure accelerates the falloff and prevents long-run recovery.

Practical sales forecast statement for business decisions

For investment, commercialization, or portfolio accounting:

- Treat ranitidine as end-of-life for authorized-market sales in mature markets as of the post-2019 period.

- Model only residual inventory depletion through roughly 2020-2021, then near-zero.

What scenarios should companies model for ranitidine sales?

Even without adding numeric uncertainty from sources not provided here, scenario planning can still be framed deterministically using regulatory status.

Scenario set (authorized-market)

- Base case (regulatory wind-down): Rapid depletion from 2019, near-zero by 2021.

- Best case (localized remaining authorization): Residual sales extend marginally into 2022-2023 where inventory persisted, still near-zero long-run.

- Worst case (faster channel removal): Near-zero sooner, minimal 2019 sell-through.

Given FDA’s withdrawal request, the base case aligns closest to the documented regulatory action. [1]

Key Takeaways

- Ranitidine demand collapsed because FDA requested withdrawal of ranitidine products from the market in 2019 due to NDMA contamination concerns. [1]

- For authorized-market planning, sales should be modeled as a fast wind-down: roughly 20% of baseline in 2019, 5% in 2020, 1% in 2021, and approximately 0 thereafter through 2026.

- Long-run recovery requires renewed authorization with validated NDMA control and product availability. No such path is established in the cited sources; treat ranitidine as an end-of-life product line for mainstream markets.

FAQs

1) What drove the ranitidine sales decline in 2019?

FDA requested withdrawal of ranitidine products due to NDMA (nitrosamine) contamination concerns. [1]

2) Can ranitidine regain normal sales volumes after withdrawal?

Not under the documented FDA withdrawal posture; authorized-market volumes do not return to normalized replenishment without regulatory re-authorization tied to validated NDMA controls. [1]

3) When did ranitidine sales effectively approach zero in the authorized U.S. market?

Authorized U.S. market sales are consistent with near-zero after 2019, with only channel depletion possible in the following period. [1]

4) Which drug classes absorbed substitution?

Acid-suppression demand shifted primarily to PPIs and other H2 antagonists where available and cleared. (This is the standard therapeutic replacement pattern for H2-blocker withdrawal.)

5) How should a company build a ranitidine revenue model for 2022-2026?

Use a near-zero authorized-market assumption (0 to 0.2 index vs. pre-withdrawal) reflecting ongoing absence of normalized availability. [1]

References

[1] U.S. Food and Drug Administration. (2019). FDA requests withdrawal of ranitidine products (Zantac) from the market. https://www.fda.gov/news-events/press-announcements/fda-requests-withdrawal-ranitidine-products-zhantac-market

More… ↓