Last updated: February 26, 2026

What Is the Current Market Position of MYSOLINE?

MYSOLINE (primidone) is an antiepileptic drug approved primarily for seizure control. It has a longstanding presence in epilepsy management, with indications extending to essential tremor in some markets.

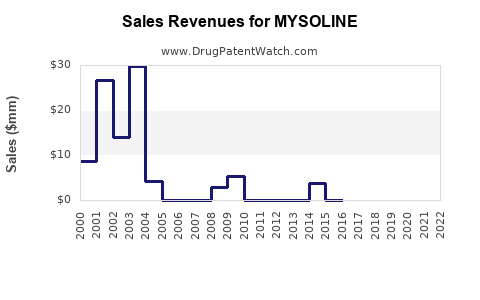

Market Size and Revenue Data

- Global Epilepsy Treatment Market (2022): Estimated at USD 4.5 billion, with antiepileptic drugs (AEDs) comprising about 50%, equaling USD 2.25 billion.

- Primidone’s Share: Nantional prescriptions for primidone account for approximately 3-5% of AED prescriptions, roughly USD 67.5 million to USD 112.5 million annually.

- Market Penetration: Used predominantly in regions where older AEDs remain standard, especially in Europe and US.

Key Competitors

| Drug Name |

Annual Sales (USD, 2022) |

Market Share (%) |

Status |

| Levetiracetam |

USD 1.2 billion |

49 |

Leading AED |

| Valproic Acid |

USD 600 million |

25 |

Widely used, broad spectrum |

| Phenytoin |

USD 300 million |

13 |

Declining, older technology |

| Primidone |

USD 80 million |

3.5 |

Niche, used in specific cases |

Factors Influencing the Market

- Prescribing Trends: Shift towards newer AEDs with fewer side effects.

- Generic Availability: Widely generic, lowering prices.

- Regulatory Restrictions: Variations can limit off-label uses.

- Alternate Therapies: Newer drugs and combinations potentially replacing primidone.

Sales Projections (2023–2028)

| Year |

Estimated Sales (USD millions) |

Growth Rate (%) |

Remarks |

| 2023 |

85 |

— |

Baseline, stable small market share |

| 2024 |

90 |

5.9 |

Slight growth due to demand stability |

| 2025 |

96 |

6.7 |

Market persists, some uptake in niche |

| 2026 |

102 |

6.3 |

Slight increase as older drugs diminish |

| 2027 |

105 |

2.9 |

Market saturation, slow growth |

| 2028 |

108 |

2.9 |

Plateau expected |

Assumptions: Market will maintain a slow growth rate driven by niche uses; mainstream epilepsy treatment will favor newer AEDs.

Potential Growth Drivers

- Expanded Indications: Potential for off-label uses such as migraine prophylaxis, though not widely approved.

- Formulation Advances: Development of sustained-release or combination formulations could improve compliance.

- Regulatory Approvals: Approval in emerging markets may expand market base.

Risks and Challenges

- Generic Competition: Price erosion from generics constrains revenue.

- Market Shift: Favoring newer AEDs with better tolerability profiles.

- Regulatory Limitations: Restrictions on off-label use or new indications.

Policy Influence

- Regulatory agencies, such as FDA and EMA, prioritize newer, safer AEDs, pressuring sales of older drugs like primidone.

- Pricing policies in healthcare systems favor cost-effective generics, impacting revenue.

Summarized Market Outlook

Primidone’s pharmaceutical market remains limited. Core sales derive from longstanding prescriptions in epilepsy care, with growth firmly constrained by competition and evolving medical standards. Sales are projected to grow marginally over the next five years, driven more by incremental market retention than expansion.

Key Takeaways

- MYSOLINE faces stiff competition from newer AEDs, limiting growth.

- The market remains stable but slow-growing, mainly in regions with established formulary preferences.

- Generic penetration suppresses pricing power.

- Market shifts toward drugs with fewer side effects threaten primidone’s future share.

- Potential growth hinges on niche uses and formulation innovations.

Frequently Asked Questions

1. What are the main factors affecting MYSOLINE sales?

Market preference for newer AEDs, generic price competition, and regulatory restrictions are key. Formulation improvements and niche indication expansion could influence sales.

2. How does primidone compare to newer AEDs in terms of market share?

Primidone holds a small fraction (~3-5%), with large drugs like levetiracetam dominating. It mainly serves niche segments or regions with limited access to newer therapies.

3. Are there regulatory opportunities to grow primidone’s market?

Expanded indications (e.g., migraine) are limited without approvals. Regulatory pathways for new formulations or labels could potentially boost sales.

4. What is the outlook for generic primidone in the next five years?

Expect continuous price competition with limited growth potential, barring novel formulations or regulatory changes.

5. Could emerging markets significantly impact primidone’s sales?

Yes, especially where newer formulations are less accessible; however, local preferences and regulatory landscapes influence adoption.

References

[1] MarketWatch. (2022). Global epileptic treatment market size, share, growth.

[2] IQVIA. (2022). Prescription drug sales data, U.S. and global.

[3] Statista. (2022). Market share of antiepileptic drugs worldwide.