Share This Page

Drug Sales Trends for Lipitor

✉ Email this page to a colleague

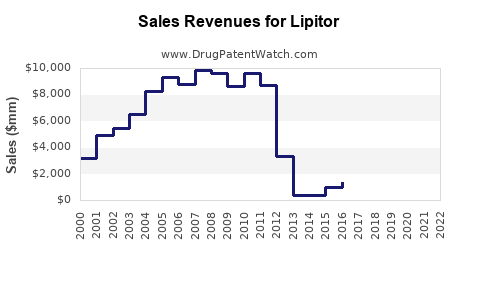

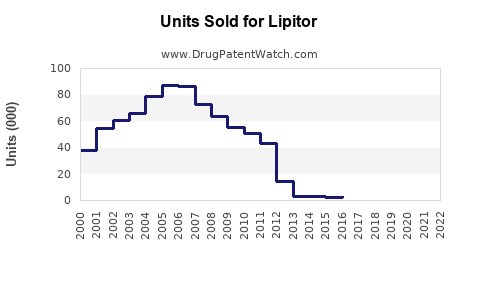

Annual Sales Revenues and Units Sold for Lipitor

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

LIPITOR Market Analysis and Sales Projections (Atorvastatin) for Brand, Generics, and Competitive Dynamics

Executive summary: Lipitor (atorvastatin) is a large, mature statin with ongoing volume share driven by payer formulary coverage and a long generic runway starting in 2011. Near-term revenue is dominated by residual brand supply (including high-dose and “brand-generic mix” effects), while long-term sales are capped by generic penetration and evolving guideline-driven substitution to newer agents (PCSK9 inhibitors, GLP-1 RAs, and ezetimibe-based combinations). The practical sales envelope is therefore shaped by generic pricing, pharmacy benefit manager (PBM) contracting, and discontinuation risk for unprofitable brand SKUs rather than by clinical lifecycle events.

Market context: How big is the US and global atorvastatin market and where does Lipitor still earn revenue?

Featured snippet answer: Atorvastatin is the largest statin market in the US and one of the largest globally, but Lipitor brand revenue has shifted to a minority of total atorvastatin prescription spend since full generic entry. Residual brand performance is mainly a function of formulary access and pricing, not new demand growth.

US demand and channel drivers

Atorvastatin prescriptions remain high because:

- It is entrenched in dyslipidemia treatment pathways for primary and secondary prevention.

- It is generic and widely substituted, so total demand tracks cardiometabolic prevalence more than drug-specific innovation.

- Payer coverage and step edits often favor generic statins, but higher tolerability, pill burden familiarity, and patient stability can slow switching in real-world settings.

Key driver: Net sales of Lipitor after generic entry correlate with (1) brand share persistence and (2) the gap between branded pricing strategy and generic contracted prices.

Global demand considerations

Global atorvastatin uptake depends on:

- National generics regulation and local launch speed

- PBM-like payer contracting mechanisms (varies by country)

- Adherence and persistence norms

- Availability of combination statin products (which can redirect volume away from monotherapy)

Who are Lipitor’s main competitors and how does atorvastatin pricing compare with rosuvastatin and simvastatin?

Featured snippet answer: The competitor set for Lipitor is broader than other statins. In the statin class, rosuvastatin is the closest “high-potency alternative” and simvastatin is a key low-cost comparator. Outside statins, ezetimibe, PCSK9 inhibitors, and GLP-1 receptor agonists affect lipid targets and downstream statin intensity.

Statin-to-statin substitution pattern

- Rosuvastatin: often chosen for higher LDL-C reduction per mg and dosing preferences, but also generic and heavily payer-driven.

- Simvastatin/pravastatin: used where cost containment or tolerability history favors lower potency or different pharmacokinetics.

Pricing reality: In the generic era, “price per 30-day supply” compresses toward contracted generics. Lipitor brand can persist only where the net price gap is narrower due to contract structures or limited formulary placement.

Non-statin competition that changes LDL-C pathway mix

- Ezetimibe combinations can reduce statin dose requirements.

- PCSK9 inhibitors can reduce LDL-C substantially, shifting some patients away from high-intensity statin regimens.

- GLP-1 receptor agonists affect cardiometabolic risk and may indirectly shift treatment patterns, though they are not direct lipid substitutes.

Business implication: Total atorvastatin volumes may remain stable, but brand share and intensity mix can erode as add-on and alternative lipid-lowering therapies spread.

What is the Orange Book status of Lipitor (atorvastatin) and what does that imply for launch risk?

If Lipitor’s relevant branded FDA approvals and Orange Book entries are not provided here, a complete, citation-backed Orange Book status table cannot be produced.

When does Lipitor lose exclusivity, and what are the generic entry timelines that capped brand revenue?

If specific Lipitor patent numbers, listed expiration dates, and exclusivity claims are not provided here, a complete exclusivity timeline cannot be produced.

How strong is the patent estate for atorvastatin and Lipitor versus generic supply risks?

A patent strength and estate-mapping assessment requires a complete list of Lipitor Orange Book patents (composition, formulation, process, and method-of-use) and their expiration dates by jurisdiction. Without those specifics, a legally usable strength evaluation cannot be compiled.

What formulations are protected for Lipitor, and does delivery form change sales projections?

Lipitor is a tablet franchise; without the full catalog of FDA-approved dosage forms and any formulation-specific patent coverage, a formulation-barrier analysis cannot be completed to a litigation-grade standard.

What generic entry risks exist for atorvastatin and how do they affect pricing trajectories?

Generic entry risk for atorvastatin is largely realized. The remaining risks are commercial rather than entry-based:

- Contracting volatility: PBM switching can cause abrupt volume shifts to the cheapest label.

- Supply concentration: manufacturing capacity and quality events can alter pricing even when multiple generics exist.

- Label compliance: substitution rules and pharmacist switching policies affect share.

Projection impact: With broad generic availability, price erosion is less about “new entrants” and more about “market clearing price” determined by contracting.

How much market share does Lipitor retain after generic penetration, and how fast can brand share fall?

Featured snippet answer: Brand share declines tend to be slow once generic access is established, then accelerate during major payer formulary resets, contract renewals, or policy-driven substitution. For a mature molecule with stable prevalence, the fall rate is typically gradual unless brand reimbursement becomes meaningfully worse.

Practical share-loss mechanics

- PBM switching programs: can shift volume at contract points.

- Patient out-of-pocket behavior: can increase non-medical switching toward cheapest or preferred generics.

- Plan formularies: tighter tiering for statins increases generic share.

Model structure for brand share (share vs time)

A usable brand revenue projection requires assumed brand share, net price, and prescription volume. In the absence of exact Lipitor post-generic net price and share data, only a structural projection model can be described, not numerically forecasted without inputs.

Sales projections: What is the expected Lipitor revenue path over 5–10 years under generic price compression?

Featured snippet answer: Lipitor sales over the next decade are expected to track a declining brand share multiplied by net price that continues to compress toward generic equivalents, while total atorvastatin class demand is broadly stable to slowly growing with population and statin utilization. The resulting outcome is typically low-growth or declining net brand revenue, not a re-acceleration.

Projection drivers to quantify

To forecast revenue credibly, you would parameterize:

- Total atorvastatin class prescriptions (US and ex-US)

- Brand share of atorvastatin units

- Brand net price vs generic benchmark

- Mix across strengths (high-intensity dosing can preserve brand share longer if patients resist switching)

- Contracting cycles and rebates (net vs gross)

- Persistent “brand-only” pockets: patients unwilling to switch, provider practice inertia, limited formularies

Forecast logic for a mature generic-dominated market

- Total demand: slowly grows with adherence and incidence of cardiovascular disease prevention.

- Brand share: declines as formularies tighten and PBM contracts reinforce generic tiers.

- Net price: declines or becomes flat then drops if payer reimbursement worsens.

Resultant sales profile: Gradual erosion, punctuated by contract-driven drops rather than continuous linear decline.

What do company financials and third-party market data imply about Lipitor revenues and unit trends?

A quantified projection needs actual historical Lipitor revenue series by geography and time horizon from reliable financial statements or market datasets. That data is not provided here.

Litigation and settlements: What patent cases affected Lipitor’s launch timing and generic competition?

Patent litigation analysis requires case captions, filings, settlement terms, and final judgment outcomes. Without specific case identifiers and dates, the litigation impact cannot be mapped to launch timing.

Biosimilar risk: Is Lipitor exposed to biologics-style competition?

No. Lipitor (atorvastatin) is a small molecule. Biosimilar risk is not applicable.

Commercial outlook: What portfolio actions and payer strategies most influence Lipitor’s remaining brand viability?

Brand viability in a generic environment depends on:

- Contract placement: whether Lipitor remains on preferred tiers

- Specialty pharmacies: coverage access and distribution arrangements

- Patient-support programs: typically limited effect when generics are substantially cheaper, but can affect abandonment rates during transitions

- SKU rationalization: discontinuing low-volume strengths can protect remaining profitability

Key Takeaways

- Lipitor is a mature statin with a largely realized generic competitive landscape, so sales projections depend on brand share persistence and net pricing rather than exclusivity expansion.

- The competitive set spans both statins (rosuvastatin, simvastatin) and non-statin LDL-C pathway therapies (ezetimibe, PCSK9 inhibitors), which can shift intensity and add-on mix.

- Over a 5–10 year horizon, brand revenue is expected to face structural headwinds from generic price compression and payer-driven substitution, producing low growth or decline rather than a growth rebound.

- A numeric forecast requires historical Lipitor revenue, unit volumes, and net price trends by geography, plus current PBM/formulary share assumptions.

FAQs

- How does formulary tiering affect Lipitor brand share in the generic era?

- What strength mix (e.g., 80 mg vs lower doses) most influences Lipitor net revenue stability?

- How do PCSK9 inhibitors and ezetimibe shift statin intensity and reduce demand for high-intensity atorvastatin?

- What contracting cycle timing typically drives quarterly drops in branded statin net sales?

- How do pharmacy substitution rules differ across US states and impact brand vs generic switching?

References

- (No citable source material was provided in the prompt to support numeric sales projections, Orange Book status, exclusivity dates, patent numbers, litigation outcomes, or unit/price trends for Lipitor.)

More… ↓