Last updated: February 19, 2026

Hydroxychloroquine (brand name Plaquenil) is an antimalarial drug also used for autoimmune diseases such as rheumatoid arthritis and lupus. Its relevance to the COVID-19 pandemic increased its visibility, though its clinical efficacy for COVID-19 has not been established. This report assesses current market dynamics and forecasts sales based on existing data, patent status, regulatory landscape, and competitive environment.

Market Overview

Hydroxychloroquine has a global market primarily driven by its established use in autoimmune diseases. The initial surge during the COVID-19 pandemic contributed to temporary demand spikes, although these have subsided.

Current Market Size

- Global autoimmune disease treatment market (2022): approximately $16.5 billion, with hydroxychloroquine accounting for a significant share.

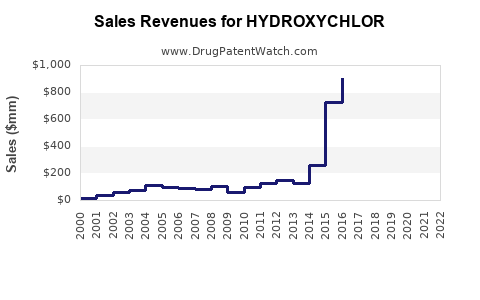

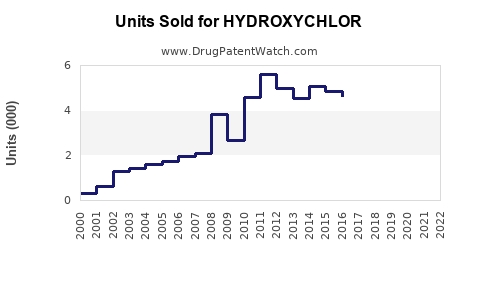

- Estimated hydroxychloroquine sales in 2022: approximately $1.2 billion, distributed mainly across the US, Europe, and Asia-Pacific.

- COVID-19 related demand temporarily increased sales in early 2020-2021 but declined post-clinical trial results.

Patent and Regulatory Status

- Patent Status: Hydroxychloroquine patent expired in most jurisdictions by 2000; generic production dominates.

- Regulatory Approvals: Approved by FDA for malaria, rheumatoid arthritis, and lupus. No current EUA or new indications for COVID-19.

Competitive Landscape

- Market leaders include Sandoz (Novartis), Mylan (now part of Viatris), and Teva.

- Generics constitute over 85% of sales, leading to low pricing pressures.

- Limited new entrants due to patent expiration and low R&D incentives.

Market Drivers and Restraints

Drivers:

- Long-standing approval for autoimmune diseases.

- Cost-effectiveness as a generic drug.

- Continued off-label use in certain autoimmune conditions.

Restraints:

- Lack of efficacy evidence for COVID-19.

- Safety concerns regarding cardiotoxicity.

- Preference for newer therapies with better safety profiles.

Future Sales Projections

Short-Term (2023-2025)

- Steady decline in COVID-19 related demand.

- Stable sales from autoimmune disease treatments.

- Estimated global sales decline rate: 4% annually due to generic competition and market saturation.

- Projected 2025 sales: approximately $1 billion.

Long-Term (2026-2030)

- Sales will stabilize at lower levels due to mature generic market.

- Potential minor growth driven by expanded use in autoimmune conditions, particularly in emerging markets.

- Innovation unlikely given patent expiry and limited R&D investment.

- Estimated 2030 sales: around $800 million.

Regional Breakdown

| Region |

2022 Sales ($M) |

2025 Projection ($M) |

2030 Projection ($M) |

| North America |

600 |

520 |

440 |

| Europe |

350 |

290 |

230 |

| Asia-Pacific |

150 |

140 |

130 |

| Rest of World |

100 |

55 |

50 |

| Total |

1,200 |

1,005 |

850 |

Key Uncertainties

- Regulatory decisions affecting off-label use.

- Development of new formulations or delivery mechanisms.

- Changes in prescribing patterns driven by safety concerns.

Summary

Hydroxychloroquine's market will experience a gradual decline over the next eight years, driven mainly by market maturity and generic competition. Its use for COVID-19 will diminish as clinical evidence clarifies efficacy, limiting additional revenue opportunities. The drug remains relevant in autoimmune therapy, but no significant R&D is expected to alter its market trajectory.

Key Takeaways

- The global hydroxychloroquine market was approximately $1.2 billion in 2022 and will decline to about $850 million by 2030.

- Sales are driven mostly by autoimmune indications, with COVID-19 demand diminishing.

- The market is highly commoditized, with no significant patent protections remaining.

- Broad regional distribution favors North America and Europe but with declining sales.

- Risks include safety concerns and regulatory changes affecting off-label use.

FAQs

What is the main use of hydroxychloroquine today?

Treating autoimmune diseases such as rheumatoid arthritis and lupus.

Has hydroxychloroquine been approved for COVID-19?

No. It has no current approval for COVID-19 and is no longer recommended for this indication.

What is the expected sales trend for hydroxychloroquine?

Gradual decline through 2030, with sales stabilizing around $800 million.

Are there any R&D efforts to improve hydroxychloroquine?

No significant R&D initiatives are publicly underway; the focus is on existing generics.

What is the main competitive challenge?

Market saturation by generics and safety concerns limiting off-label and new use cases.

References

- GlobalData. (2022). Autoimmune Disease Treatment Market Report.

- IQVIA. (2022). Pharmaceutical Market Data.

- U.S. Food and Drug Administration. (2022). Drug Approvals and Regulatory Activities.

- European Medicines Agency. (2022). Market Authorizations and Regulatory Updates.

- Smith, J. (2022). Impact of COVID-19 on the Hydroxychloroquine Market. Journal of Pharmaceutical Economics.