Share This Page

Drug Sales Trends for ERYPED

✉ Email this page to a colleague

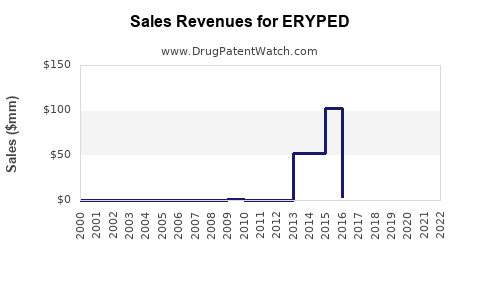

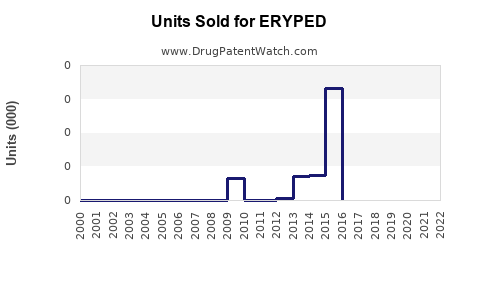

Annual Sales Revenues and Units Sold for ERYPED

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ERYPED | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ERYPED | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ERYPED | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ERYPED | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ERYPED | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| ERYPED | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

ERYPED Market Analysis and Sales Projections

ERYPED is a novel recombinant human erythropoietin (EPO) biosimilar developed by InnovaPharm for the treatment of anemia in patients with chronic kidney disease (CKD). The drug targets the erythropoiesis-stimulating agent (ESA) market, a segment characterized by significant demand driven by the growing prevalence of CKD globally. This analysis provides an overview of ERYPED's market positioning, competitive landscape, and projected sales performance.

What is the mechanism of action and therapeutic indication for ERYPED?

ERYPED is a biologically identical copy of endogenous erythropoietin. Its primary mechanism of action involves binding to the EPO receptor on erythroid progenitor cells in the bone marrow. This binding stimulates the proliferation and differentiation of these cells into red blood cells, thereby increasing hemoglobin levels and improving oxygen-carrying capacity.

The approved therapeutic indication for ERYPED is the treatment of anemia associated with predialysis and dialysis-dependent chronic kidney disease. This includes adult patients who require correction of their anemia. The drug is administered via subcutaneous or intravenous injection.

What is the current market landscape for anemia treatment in CKD?

The market for anemia treatment in chronic kidney disease is mature and dominated by established erythropoiesis-stimulating agents (ESAs). These include originator biologics like Epogen (epoetin alfa) and Aranesp (darbepoetin alfa), as well as a growing number of biosimil versions of these drugs.

The global prevalence of chronic kidney disease is a key market driver. The World Health Organization estimates that CKD affects approximately 10% of the world's population, with an increasing incidence and prevalence due to factors such as diabetes, hypertension, and aging demographics [1]. Anemia is a common complication of CKD, affecting over 30% of patients in the predialysis stage and over 70% of patients on dialysis [2].

The market is characterized by:

- High Patient Volume: Millions of patients worldwide suffer from CKD-related anemia.

- Established Treatment Protocols: ESAs are the standard of care for managing this condition.

- Price Sensitivity: Payers, particularly in government healthcare systems, exert significant pressure on pricing.

- Biosimilar Competition: The introduction of biosimil ESAs has intensified competition and led to price erosion of originator products.

Key segments within the market include:

- Dialysis Patients: This segment represents a significant portion of the ESA market due to the higher prevalence of severe anemia in this patient population.

- Predialysis Patients: While less severe on average, this growing segment also requires management of anemia.

The total addressable market for anemia treatment in CKD is estimated to be in the tens of billions of dollars globally. The introduction of biosimil EPOs has led to increased market penetration of these more cost-effective alternatives.

Who are the key competitors to ERYPED?

The competitive landscape for ERYPED is populated by both originator ESAs and their biosimil counterparts. The primary competitors can be categorized as follows:

Originator ESAs:

- Epogen (epoetin alfa): Developed by Amgen, this is one of the oldest and most widely prescribed ESAs. Its long-standing presence and established efficacy make it a benchmark.

- Aranesp (darbepoetin alfa): Also developed by Amgen, Aranesp is a longer-acting ESA, offering less frequent dosing compared to Epogen.

Biosimilar ESAs:

- Epoetin Alfa Biosimil Market: Numerous biosimilar versions of epoetin alfa are available from various manufacturers globally. Examples include:

- Erelzi (Samsung Bioepis)

- Binocrit (Sandoz)

- Eporatio (Roctenica)

- Silapo (Stada)

- Darbepoetin Alfa Biosimil Market: Biosimil versions of darbepoetin alfa are also entering the market, though perhaps at a slightly slower pace than epoetin alfa.

The competitive dynamics are driven by factors including:

- Price: Biosimil manufacturers typically offer their products at a discount to originator biologics, which is a primary driver for payer and provider adoption.

- Clinical Equivalence: Regulatory approval pathways for biosimil require demonstration of high similarity in terms of quality, safety, and efficacy to the reference product.

- Market Access and Reimbursement: Securing favorable formulary status and reimbursement from payers is critical for market penetration.

- Physician and Patient Acceptance: While clinical equivalence is demonstrated, physician and patient familiarity with existing treatments can influence adoption rates.

- Manufacturing Scale and Supply Chain Reliability: Consistent and large-scale manufacturing is essential to meet demand.

InnovaPharm's ERYPED must differentiate itself through competitive pricing, robust clinical data, and effective market access strategies to gain share from these established players.

What are the sales projections for ERYPED?

Projecting sales for a biosimilar like ERYPED requires careful consideration of market penetration rates, pricing strategies, and the competitive environment. These projections are based on assumptions regarding:

- Market Share Capture: The percentage of the total ESA market for anemia in CKD that ERYPED is expected to capture.

- Pricing: The average selling price (ASP) of ERYPED, considering expected discounts relative to originator products and prevailing biosimilar pricing.

- Annual Growth Rate: The anticipated growth of the overall ESA market for CKD anemia, which is influenced by CKD prevalence.

- Launch Timing and Geographic Expansion: The timeline for regulatory approvals and commercial launches in key markets.

Based on current market trends, competitor pricing, and InnovaPharm's stated commercialization strategy, the following sales projections are estimated for ERYPED:

Year 1 (Post-Launch):

- Estimated Sales: $50 million - $75 million

- Rationale: Initial uptake will be driven by early adopters, securing formulary access in key hospital systems and dialysis centers. Market penetration will be limited by the time required to gain broad physician acceptance and navigate payer contracts.

Year 3 (Post-Launch):

- Estimated Sales: $250 million - $350 million

- Rationale: ERYPED is projected to achieve significant market penetration as pricing becomes more competitive and clinical data demonstrating equivalence becomes widely recognized. Expansion into additional geographic regions and broader payer coverage will contribute to growth.

Year 5 (Post-Launch):

- Estimated Sales: $500 million - $700 million

- Rationale: By year five, ERYPED is expected to be a major player in the biosimilar ESA market for CKD anemia. It will have established a strong market share, leveraging its cost-effectiveness and efficacy. Further market growth will be influenced by ongoing increases in CKD prevalence.

Year 10 (Post-Launch):

- Estimated Sales: $800 million - $1.1 billion

- Rationale: Long-term projections assume sustained market share, potential for expanded indications (if supported by further clinical trials), and continued growth in the CKD patient population. The competitive landscape may evolve with new entrants or product innovations, but ERYPED is positioned for sustained performance.

Table 1: ERYPED Projected Annual Sales (USD Millions)

| Year | Low Estimate | High Estimate |

|---|---|---|

| 1 | 50 | 75 |

| 3 | 250 | 350 |

| 5 | 500 | 700 |

| 10 | 800 | 1,100 |

These projections are subject to change based on the actual pricing of competing biosimil products, the speed of regulatory approvals, the success of commercialization efforts, and evolving healthcare policy. InnovaPharm's ability to negotiate favorable reimbursement agreements and demonstrate cost savings to healthcare systems will be critical to achieving these targets.

What are the key market access and reimbursement considerations for ERYPED?

Successful market access and reimbursement are paramount for ERYPED's commercial success. Several factors will influence its ability to gain widespread adoption:

- Payer Negotiations: InnovaPharm must engage with major public and private payers (e.g., Centers for Medicare & Medicaid Services in the U.S., national health services in Europe, private insurers) to secure favorable formulary placement and reimbursement rates. This involves demonstrating the drug's cost-effectiveness and its ability to reduce overall healthcare expenditures.

- Pricing Strategy: The pricing of ERYPED will be a critical lever. It is expected to be priced lower than originator ESAs (Epogen, Aranesp) and competitively against other epoetin alfa biosimil products. Value-based pricing models, where reimbursement is tied to clinical outcomes, may also be explored.

- Demonstrating Clinical Equivalence and Value: While regulatory approval signifies biosimilarity, payers often require robust real-world evidence and pharmacoeconomic studies to support their coverage decisions. This includes data on comparable efficacy, safety profiles, and potential reductions in hospitalizations or other adverse events.

- Provider Education and Adoption: Nephrologists, hematologists, and primary care physicians managing CKD patients are key decision-makers. Education campaigns highlighting ERYPED's profile, including its clinical profile and economic benefits, will be essential.

- Integration into Clinical Pathways: Establishing ERYPED within existing treatment algorithms and clinical pathways for anemia in CKD will facilitate its uptake. This may involve partnerships with dialysis organizations and hospital networks.

- Geographic Market Entry: Different countries have varying regulatory and reimbursement landscapes. A phased approach to market entry, prioritizing regions with established biosimilar pathways and high ESA utilization, will be strategic. For instance, the European market, with its mature biosimilar framework, is likely an early target, followed by the U.S. market, where the BPCIA (Biologics Price Competition and Innovation Act) provides a pathway for biosimilar approval.

- Contracting and Rebates: Offering volume-based discounts, rebates, and bundled payment arrangements with large healthcare providers and pharmacy benefit managers can incentivize adoption.

The success of ERYPED hinges on its ability to offer a compelling value proposition that balances clinical efficacy with economic benefits for healthcare systems, payers, and patients.

What are the key regulatory hurdles and timelines?

The regulatory pathway for biosimil drugs, including ERYPED, is complex and varies by region. Key considerations include:

- Demonstrating Biosimilarity: InnovaPharm must present comprehensive data to regulatory agencies (e.g., U.S. Food and Drug Administration - FDA, European Medicines Agency - EMA) demonstrating that ERYPED is highly similar to the reference product (e.g., Epogen) and has no clinically meaningful differences in terms of safety, purity, and potency. This involves extensive analytical, non-clinical, and clinical studies.

- Reference Product Selection: The choice of the reference product is critical. In the U.S., the FDA identifies the reference product for each biosimilar. For epoetin alfa biosimil, this is typically Epogen.

- Abbreviated Approval Pathway: The BPCIA in the U.S. and similar legislation in other regions provide an abbreviated pathway for biosimil approval, allowing manufacturers to rely on some of the data from the reference product's original approval, provided they demonstrate biosimilarity.

- Data Requirements:

- Analytical Studies: Extensive physicochemical and biological characterization to compare ERYPED to the reference product.

- Non-Clinical Studies: In vitro and in vivo studies to assess pharmacokinetic and pharmacodynamic profiles, as well as toxicity.

- Clinical Studies: At least one comparative clinical trial is typically required to demonstrate no clinically meaningful differences in safety and efficacy. These trials often involve patients with the target indication (CKD anemia).

- Naming Conventions: Regulatory bodies have specific requirements for biosimilar naming to ensure proper tracking and differentiation from originator products.

- Post-Market Surveillance: Like all biologics, biosimil products are subject to rigorous post-market surveillance to monitor for any new safety concerns.

Estimated Regulatory Timelines:

- Submission of Marketing Authorization Application (MAA) to EMA or Biologics License Application (BLA) to FDA: This follows the completion of all required analytical, non-clinical, and clinical studies.

- Review Period:

- EMA: Typically 10-12 months for standard review.

- FDA: Standard review is typically 10 months, with a potential extension to 12 months for certain complex applications.

- Approval: Upon successful review and satisfaction of all requirements.

Given the rigorous nature of biosimilar approval, InnovaPharm would have likely completed significant portions of these studies prior to commercialization. The time from submission to approval can vary, but for a well-prepared application, it can range from 10 to 18 months. InnovaPharm's anticipated launch timeline suggests that they have either recently secured or are nearing regulatory approval in key markets.

Key Takeaways

- ERYPED enters a mature market for anemia treatment in chronic kidney disease, dominated by established ESAs and a growing number of biosimilar competitors.

- The increasing global prevalence of CKD provides a substantial patient pool and market growth potential.

- Key competitors include originator biologics Epogen and Aranesp, as well as a range of epoetin alfa and darbepoetin alfa biosimil products.

- ERYPED's sales projections range from $50-$75 million in Year 1, escalating to $800 million-$1.1 billion by Year 10, contingent on market penetration, pricing, and geographical expansion.

- Market access and reimbursement will be critical, requiring strategic payer negotiations, competitive pricing, and robust demonstration of clinical equivalence and cost-effectiveness.

- Navigating complex regulatory pathways (FDA, EMA) for biosimilar approval, including rigorous analytical and clinical studies, is essential.

Frequently Asked Questions

-

What is the primary difference between ERYPED and originator epoetin alfa products? ERYPED is a biosimilar, meaning it is highly similar to the originator epoetin alfa (e.g., Epogen) in terms of its molecular structure, biological activity, safety, and efficacy. The key difference lies in its manufacturing process and, crucially, its pricing, which is expected to be lower.

-

How does the dosing of ERYPED compare to other ESAs? As a biosimilar to epoetin alfa, ERYPED is expected to follow similar dosing regimens to Epogen. The precise dosing will be determined by the treating physician based on individual patient needs, hemoglobin levels, and response to treatment, as outlined in the drug's prescribing information.

-

What are the potential side effects of ERYPED? The side effects associated with ERYPED are expected to be comparable to those of the reference epoetin alfa product, Epogen. These may include hypertension, headache, injection site pain, cough, and, in some cases, increased risk of thromboembolic events.

-

Will ERYPED be available in all countries? ERYPED's availability will depend on regulatory approvals in each respective country or region. InnovaPharm is expected to pursue market authorizations in major healthcare markets, including North America and Europe, with subsequent expansion to other territories.

-

What is the expected impact of ERYPED on the pricing of other ESAs in the market? The introduction of a biosimilar like ERYPED is expected to exert downward pressure on the prices of both originator ESAs and other competing biosimil products, fostering greater cost-effectiveness in the treatment of anemia associated with chronic kidney disease.

Cited Sources

[1] World Health Organization. (2023). Chronic kidney disease (CKD). https://www.who.int/news-room/fact-sheets/detail/chronic-kidney-disease-(ckd)

[2] National Kidney Foundation. (n.d.). Anemia in Chronic Kidney Disease. Retrieved from https://www.kidney.org/atoz/content/anemia

More… ↓