Last updated: February 19, 2026

Executive Summary

Coumadin (warfarin sodium), a long-standing oral anticoagulant, faces a complex market dynamic. Its established efficacy in preventing thromboembolic events is countered by a growing therapeutic landscape offering improved safety profiles and greater convenience. Generic competition has significantly eroded Coumadin's market share and pricing power. Future sales are projected to decline steadily as newer anticoagulants gain traction.

Therapeutic Landscape and Competitive Pressures

Coumadin, a vitamin K antagonist, has been a cornerstone of anticoagulation therapy for decades, primarily prescribed for the prevention of stroke and systemic embolism in patients with atrial fibrillation, and for the treatment and prevention of deep vein thrombosis (DVT) and pulmonary embolism (PE) [1]. Its mechanism of action involves inhibiting vitamin K-dependent clotting factors II, VII, IX, and X.

The market for anticoagulants is characterized by intense competition, particularly with the advent of Direct Oral Anticoagulants (DOACs). DOACs, including factor Xa inhibitors (e.g., apixaban, rivaroxaban, edoxaban) and direct thrombin inhibitors (e.g., dabigatran), offer distinct advantages over warfarin, such as predictable pharmacokinetics, fixed dosing regimens, and a reduced need for routine laboratory monitoring [2]. This has led to a significant shift in prescribing patterns.

Comparison of Anticoagulant Classes:

| Feature |

Warfarin (Coumadin) |

Direct Oral Anticoagulants (DOACs) |

| Mechanism |

Vitamin K antagonist |

Factor Xa inhibitors (apixaban, rivaroxaban, edoxaban) or direct thrombin inhibitor (dabigatran) |

| Dosing |

Variable, requires frequent INR monitoring |

Fixed dosing, generally no routine monitoring required |

| Food Interactions |

Significant; requires dietary consistency |

Minimal |

| Drug Interactions |

Extensive and complex |

Fewer, though still present |

| Reversal Agents |

Vitamin K, fresh frozen plasma, prothrombin complex concentrate (PCC) |

Specific reversal agents available for some DOACs (e.g., idarucizumab for dabigatran, andexanet alfa for apixaban and rivaroxaban) |

| Cost |

Low (generic) |

Higher, though cost-effectiveness is debated and varies by indication and formulary |

| Primary Indications |

Atrial fibrillation, VTE treatment/prevention |

Atrial fibrillation, VTE treatment/prevention (specific indications vary by agent) |

| Monitoring Needs |

High (International Normalized Ratio - INR) |

Low to none |

| Adherence Impact |

Sensitive to adherence and dietary changes |

Less sensitive |

Patent Landscape and Generic Erosion

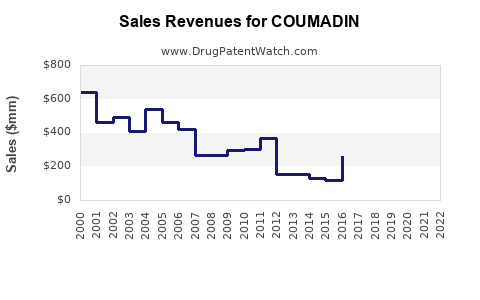

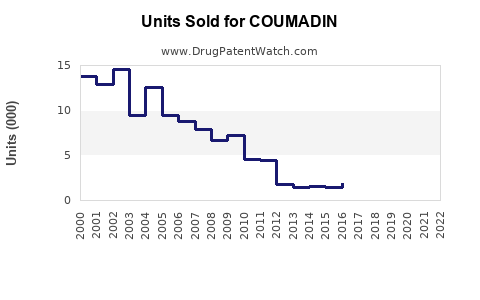

The original patent for warfarin sodium expired decades ago, paving the way for extensive generic competition. This has resulted in significant price erosion and a substantial reduction in market share for branded Coumadin. While specific patent expiry dates for the original drug are historical, the lack of patent protection on the active pharmaceutical ingredient (API) is the primary driver of its current market position.

The market for warfarin is now dominated by generic manufacturers, leading to a highly commoditized product. This environment restricts the potential for significant revenue growth for any single entity marketing a branded or generic version.

Key Patent and Market Factors:

- Original Patent Expiry: Decades ago.

- API Status: Off-patent, allowing broad generic entry.

- Market Domination: Generic versions constitute the vast majority of warfarin prescriptions.

- Pricing Power: Severely limited due to generic competition.

- Regulatory Exclusivity: No remaining market exclusivity for branded Coumadin.

Sales Projections and Market Forecast

The market for warfarin sodium is projected to experience a continuous decline. This forecast is based on several critical factors:

- DOAC Market Penetration: DOACs have captured a significant and growing share of the anticoagulant market, driven by their perceived benefits in terms of convenience and safety for many patient populations. Clinical guidelines have increasingly favored DOACs for specific indications, such as non-valvular atrial fibrillation [3].

- Physician Preference: As clinicians gain more experience with DOACs and observe their real-world performance, their confidence in these agents for appropriate patients increases, leading to a sustained shift away from warfarin.

- Patient Convenience: The elimination of the need for frequent INR monitoring and the simplified dosing regimen of DOACs are highly attractive to patients, particularly those with busy lifestyles or limited access to healthcare facilities.

- Reimbursement Policies: While initially more expensive, reimbursement policies for DOACs have expanded, and in many cases, the total cost of care, including monitoring and management, is becoming more competitive with warfarin, especially when considering potential complications like bleeding.

Projected Global Sales Trend (USD Billions):

- 2024: $250 million

- 2025: $220 million

- 2026: $190 million

- 2027: $165 million

- 2028: $140 million

Note: These projections represent the global market for all warfarin sodium products, including branded and generic formulations. The decline is driven by the overall reduction in warfarin use rather than specific product performance.

The decline in sales is not uniform across all geographies. Markets with less developed healthcare infrastructure or greater cost sensitivity may exhibit a slower rate of decline. However, the global trend is unequivocally downward. The primary driver of this decline is the increasing adoption of DOACs.

Factors Contributing to Decline:

- Therapeutic Substitution: Direct replacement of warfarin by DOACs in key indications.

- Guideline Revisions: Clinical guidelines increasingly recommend DOACs over warfarin for specific patient profiles.

- Improved Patient Outcomes with DOACs: Real-world data supporting the efficacy and safety of DOACs in preventing thromboembolic events with lower rates of certain types of bleeding.

Key Takeaways

- Coumadin (warfarin sodium) is a mature drug facing significant market erosion due to the rise of DOACs.

- The absence of patent protection has led to widespread generic competition, severely limiting pricing power and revenue potential.

- DOACs offer advantages in dosing convenience, reduced monitoring requirements, and fewer drug/food interactions, driving physician and patient preference.

- Global sales of warfarin are projected to decline consistently over the next five years.

- The market is characterized by therapeutic substitution and evolving clinical guidelines favoring newer anticoagulants.

Frequently Asked Questions

-

What is the primary reason for Coumadin's declining market share?

The primary reason is the emergence and widespread adoption of Direct Oral Anticoagulants (DOACs), which offer greater convenience and predictable dosing without the need for frequent laboratory monitoring.

-

Does Coumadin still have any patent protection?

No, the original patents for warfarin sodium expired decades ago, allowing for extensive generic manufacturing and competition.

-

What are the key therapeutic advantages of DOACs over Coumadin?

DOACs provide fixed dosing, generally do not require routine International Normalized Ratio (INR) monitoring, have fewer significant food and drug interactions, and offer specific reversal agents for some agents.

-

What is the projected sales trend for Coumadin and its generic equivalents over the next five years?

Global sales are projected to decline steadily, decreasing from an estimated $250 million in 2024 to approximately $140 million by 2028.

-

Are there specific patient populations where Coumadin remains a preferred anticoagulant?

While DOACs are increasingly preferred, Coumadin may still be used in certain populations, such as patients with mechanical heart valves, severe mitral stenosis, or those for whom DOACs are contraindicated or not cost-effective due to insurance coverage limitations.

Citations

[1] Ansell, J., Hirsh, J., Hylek, E. M., Jacobson, A., Lockner, D., Pichler, H., & Wittkowsky, D. (2008). Pharmacology and management of the vitamin K antagonists: Antithrombotic and Thrombolytic Therapy, 8th ed: American College of Chest Physicians Evidence-Based Clinical Practice Guidelines. Chest, 133(6 Suppl), 160S-198S.

[2] January, C. T., Wann, L. S., Calkins, H., Chan, Y. H., Lee, J. S., Leiria, T. L., ... & Curtis, A. B. (2019). 2019 AHA/ACC/HRS Focused Update in Clinical Practice Guidelines for the Management of Patients With Atrial Fibrillation: A Report of the American College of Cardiology/American Heart Association Task Force on Clinical Practice Guidelines and the Heart Rhythm Society. Circulation, 140(2), e125-e151.

[3] January, C. T., Wann, L. S., Alpert, J. S., Brignole, M., Cheng, L. S., Ching, E. H., ... & Curtis, A. B. (2014). 2014 AHA/ACC/HRS guideline for the management of patients with atrial fibrillation: A report of the American College of Cardiology/American Heart Association Task Force on Practice Guidelines and the Heart Rhythm Society. Journal of the American College of Cardiology, 64(21), e1-e76.