Share This Page

Drug Sales Trends for ALLOPURINOL

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for ALLOPURINOL (2020)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

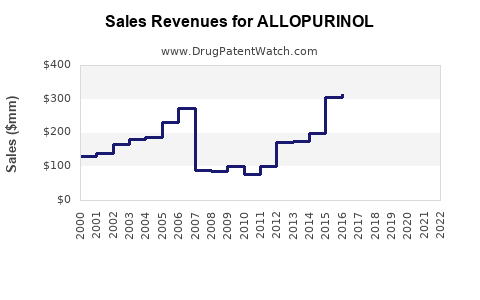

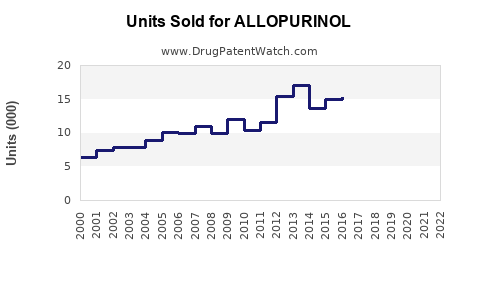

Annual Sales Revenues and Units Sold for ALLOPURINOL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ALLOPURINOL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ALLOPURINOL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ALLOPURINOL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ALLOPURINOL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ALLOPURINOL | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| ALLOPURINOL | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Allopurinol: Patent Landscape and Market Trajectory

Allopurinol, a xanthine oxidase inhibitor, remains a foundational treatment for hyperuricemia and its sequelae, including gout. Its established efficacy, long market presence, and broad therapeutic index contribute to persistent demand, though it faces increasing competition from newer agents and generics. Patent expirations for key innovator formulations have largely ceded market share to generic manufacturers, resulting in a highly price-sensitive market. However, ongoing research into novel delivery systems and combination therapies presents potential avenues for value creation and market differentiation.

What is the Current Patent Landscape for Allopurinol?

The original patents protecting allopurinol have long expired. The primary innovator, Burroughs Wellcome (now part of GlaxoSmithKline), lost patent exclusivity for its branded allopurinol (Zyloprim) decades ago. This has led to widespread generic availability.

Currently, patent activity surrounding allopurinol primarily focuses on:

- Formulation Enhancements: Patents may cover novel salt forms, polymorphs, or amorphous forms of allopurinol that aim to improve solubility, bioavailability, or stability.

- Delivery Systems: Research and patent applications explore advanced delivery mechanisms such as controlled-release formulations, transdermal patches, or even injectable forms, aiming to optimize dosing regimens and patient compliance.

- Combination Therapies: Patents are filed for fixed-dose combinations of allopurinol with other urate-lowering agents or drugs targeting comorbidities associated with hyperuricemia. These aim to offer synergistic effects and simplified treatment protocols.

- Manufacturing Processes: Process patents can be filed to protect novel, more efficient, or environmentally friendly methods of synthesizing allopurinol or its intermediates.

Key Observations:

- No broad, foundational patents for allopurinol itself are in force.

- The majority of active patents are secondary, focusing on specific product enhancements or manufacturing methods, rather than the active pharmaceutical ingredient (API) itself.

- The patent landscape is fragmented, with multiple entities holding patents on various aspects of allopurinol-related technologies.

What is the Global Market Size and Growth Projection for Allopurinol?

The global allopurinol market is mature and characterized by a significant presence of generic products. The market size is primarily driven by its use in treating gout and hyperuricemia, conditions with a growing global prevalence due to aging populations and lifestyle factors such as diet and obesity.

Market Size and Growth:

- Current Market Size: While precise figures vary by market research firm, the global allopurinol market was estimated to be in the range of USD 800 million to USD 1.2 billion in 2022-2023.

- Projected Growth: The market is projected to grow at a compound annual growth rate (CAGR) of 3% to 5% from 2023 to 2030. This moderate growth is attributed to:

- Increasing Prevalence of Gout: The incidence of gout is rising globally, particularly in developed and rapidly developing economies.

- Aging Population: Older adults are more susceptible to gout and hyperuricemia.

- Generic Dominance: While driving affordability, the dominance of generics limits significant revenue growth potential from price appreciation.

- Competition from Newer Agents: The emergence of newer, more targeted urate-lowering therapies (ULTs) like febuxostat and pegloticase, although typically more expensive, offers alternative treatment options that can cap allopurinol's growth in certain patient segments.

Regional Market Share (Estimated 2023):

- North America: 30%

- Europe: 25%

- Asia-Pacific: 30%

- Latin America & Middle East/Africa: 15%

The Asia-Pacific region is expected to exhibit the highest growth rate due to increasing healthcare access, rising disposable incomes, and a growing awareness of gout management.

Who are the Key Market Players and Competitors?

The allopurinol market is highly competitive, dominated by generic manufacturers due to the expiration of original patents. Key players operate across manufacturing, distribution, and retail.

Major Generic Manufacturers:

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now Viatris)

- Hikma Pharmaceuticals PLC

- Amneal Pharmaceuticals LLC

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Zydus Lifesciences Ltd.

These companies compete primarily on price and market penetration, leveraging extensive distribution networks and efficient manufacturing processes.

Innovator Companies (Historically and for Derivative Products):

- GlaxoSmithKline (GSK): Holds historical rights to the original Zyloprim brand. While its market share for the branded product is now negligible, GSK may hold patents on certain manufacturing processes or formulations.

- Other Companies: Several biopharmaceutical companies are involved in the development of novel urate-lowering therapies, which represent indirect competition to allopurinol. These include:

- Ironwood Pharmaceuticals (for lesinurad, although its uptake has been limited).

- BridgeBio Pharma (developing novel approaches to hyperuricemia).

- Hospira (now part of Pfizer, involved in injectable formulations).

Competitive Dynamics:

- Price Erosion: Intense competition among generic manufacturers has led to significant price erosion, making allopurinol one of the most affordable prescription ULTs.

- Quality and Regulatory Compliance: While price is paramount, manufacturers must maintain high standards of quality and regulatory compliance (e.g., FDA, EMA approval) to remain competitive.

- Supply Chain Reliability: Consistent and reliable supply is critical for generic manufacturers to capture and maintain market share.

- Indirect Competition: The development and adoption of newer ULTs (e.g., febuxostat) and biologics for refractory gout pose a threat to allopurinol's market share, particularly for patients who are unresponsive or intolerant to allopurinol.

What are the Regulatory Considerations and Approved Indications?

Allopurinol is a well-established pharmaceutical product with broad regulatory approvals worldwide. Its primary indications and regulatory status are consistent across major markets.

Approved Indications:

The primary approved indications for allopurinol include:

- Treatment of Hyperuricemia: Management of elevated uric acid levels in the blood.

- Treatment of Gout: Prevention of gout attacks (acute gouty arthritis).

- Treatment of Uric Acid Nephropathy: Prevention of kidney damage due to uric acid crystals.

- Treatment of Certain Malignancies: Prevention of hyperuricemia secondary to chemotherapy or other conditions involving rapid cell turnover (e.g., tumor lysis syndrome).

- Treatment of Recurrent Calcium Oxalate Calculi: In patients with hyperuricosuria and recurrent calcium oxalate stones.

Regulatory Bodies and Approvals:

- U.S. Food and Drug Administration (FDA): Allopurinol is approved for prescription use. The FDA maintains a comprehensive database of approved drugs, including generics.

- European Medicines Agency (EMA): Similar approvals are in place across European Union member states.

- Other National Regulatory Agencies: Approvals are held by health authorities in countries such as Japan (PMDA), Canada (Health Canada), Australia (TGA), and others.

Key Regulatory Considerations:

- Labeling and Warnings: Regulatory agencies require specific warnings on allopurinol labels, most notably the risk of severe hypersensitivity reactions, including Stevens-Johnson syndrome and toxic epidermal necrolysis, particularly in individuals with the HLA-B*5801 genetic variant. Screening for this variant is recommended in certain populations.

- Pharmacovigilance: Post-market surveillance and pharmacovigilance are ongoing to monitor for adverse events and ensure product safety.

- Abbreviated New Drug Application (ANDA) Pathway: Generic versions of allopurinol are approved via the ANDA pathway in the U.S. and equivalent processes elsewhere, requiring demonstration of bioequivalence to the reference listed drug.

- Manufacturing Standards: All manufacturing facilities must comply with current Good Manufacturing Practices (cGMP) standards.

What are the Sales Projections and Future Market Trends for Allopurinol?

Sales projections for allopurinol indicate continued, albeit modest, growth, largely driven by its established position as a cost-effective treatment option for hyperuricemia and gout. Future market trends will be shaped by its competitive positioning against newer agents, evolving treatment guidelines, and advancements in pharmaceutical technology.

Sales Projections (2024-2030):

- 2024: Projected sales: USD 820 million - USD 880 million.

- 2026: Projected sales: USD 870 million - USD 950 million.

- 2030: Projected sales: USD 930 million - USD 1.05 billion.

These projections reflect the CAGR of 3%-5% mentioned previously. The upper end of the projections accounts for potential market expansion due to increased gout prevalence and penetration in emerging markets. The lower end reflects the intensifying competition and pricing pressures.

Key Market Trends:

- Continued Generic Dominance: The market will remain predominantly generic, with price competition as a primary driver. Manufacturers with strong supply chains and cost-efficient production will maintain market leadership.

- Focus on Patient Adherence and Convenience: The development of extended-release formulations or combination products could improve patient adherence, a critical factor in managing chronic conditions like gout. Patents in this area may offer limited market exclusivity for specific enhanced products.

- Precision Medicine and Genetic Screening: Increased awareness and accessibility of genetic testing (e.g., HLA-B*5801 screening) may influence prescribing patterns, potentially favoring alternative agents in genetically predisposed individuals. However, the cost-effectiveness of allopurinol will likely sustain its use where screening is not universally implemented or affordable.

- Emergence of Novel Therapies: While allopurinol will remain a first-line option due to cost, the market share for newer, more potent, or better-tolerated agents (e.g., targeted inhibitors, biologics for refractory cases) is expected to grow, especially in developed markets and for specific patient populations.

- Market Expansion in Emerging Economies: Growing awareness of gout and hyperuricemia, coupled with improving healthcare infrastructure and affordability in regions like Asia-Pacific and Latin America, will drive volume growth for allopurinol.

- Consolidation and Strategic Alliances: The generic pharmaceutical industry may see further consolidation as companies seek economies of scale and broader market reach. Partnerships for co-marketing or distribution could also emerge.

- Sustainability in Manufacturing: Increasing emphasis on environmentally friendly manufacturing processes could lead to patents and market advantages for companies adopting greener synthesis routes for allopurinol.

What are the Key Challenges and Opportunities for Allopurinol?

Allopurinol, despite its established therapeutic role, navigates a complex market environment shaped by significant challenges and potential opportunities.

Key Challenges:

- Intense Price Competition: The generic nature of allopurinol leads to relentless price pressure, squeezing profit margins for manufacturers and distributors.

- Risk of Hypersensitivity Reactions: Severe adverse events, particularly in patients with the HLA-B*5801 allele, necessitate careful patient selection and monitoring, potentially limiting its use in certain populations or increasing healthcare system oversight costs.

- Erosion of Market Share by Newer Agents: Advanced ULTs offering improved efficacy or tolerability, albeit at higher costs, continue to capture market share, especially for patients refractory to or intolerant of allopurinol.

- Limited Innovation Pipeline for Generic API: The core allopurinol API is a mature product. While formulation patents exist, groundbreaking innovation in the fundamental molecule is unlikely.

- Supply Chain Vulnerabilities: Global supply chain disruptions can impact the availability and cost of raw materials and finished products, affecting market stability.

Key Opportunities:

- Cost-Effectiveness in Resource-Limited Settings: Allopurinol remains the most cost-effective option for managing hyperuricemia and gout, making it indispensable in low- and middle-income countries where newer agents are often unaffordable.

- Market Growth in Emerging Economies: Increasing prevalence of metabolic syndrome and gout in developing nations presents significant volume growth potential for generic allopurinol.

- Life-Cycle Management through Formulation Innovation: Patents on novel drug delivery systems (e.g., controlled-release, fixed-dose combinations with other agents) could provide limited periods of differentiation and enhanced market value.

- Combination Therapy Potential: Exploring fixed-dose combinations of allopurinol with other urate-lowering drugs or drugs targeting gout comorbidities could offer synergistic benefits and improved patient compliance, creating new product lines.

- Post-Patent Extension Strategies: While challenging, strategies such as seeking new indications or developing improved manufacturing processes can sustain product relevance and market presence.

- Focus on Pediatric Use: Further research and potential regulatory approvals for pediatric indications, if they emerge, could expand the market scope.

Key Takeaways

- Allopurinol's patent exclusivity has long expired, resulting in a highly competitive generic market dominated by price.

- The global market for allopurinol is projected to grow modestly at 3%-5% CAGR, reaching approximately USD 1 billion by 2030, driven by increasing gout prevalence and demand in emerging markets.

- Key players are primarily generic manufacturers, competing on cost, quality, and supply chain reliability.

- Approved indications are broad, covering hyperuricemia, gout, and related conditions, with crucial safety warnings regarding hypersensitivity reactions.

- Future trends include sustained generic competition, potential for formulation innovation, impact of precision medicine, and growth in emerging economies.

- Challenges include intense price erosion and competition from newer agents, while opportunities lie in its cost-effectiveness, emerging market expansion, and potential for novel delivery systems or combination therapies.

Frequently Asked Questions

-

Will new patents significantly alter the allopurinol market in the next five years? New patents are unlikely to fundamentally alter the allopurinol market landscape, as they primarily focus on incremental improvements such as formulations or manufacturing processes, rather than protecting the core API. The market will remain dominated by generic competition.

-

How does the increasing prevalence of gout impact allopurinol sales projections? The rising incidence of gout is a primary driver for sustained demand for allopurinol. It underpins the projected modest market growth, particularly as healthcare access improves in developing regions.

-

What is the most significant safety concern associated with allopurinol prescribing? The most significant safety concern is the risk of severe hypersensitivity reactions, including Stevens-Johnson syndrome and toxic epidermal necrolysis. This risk is heightened in individuals with the HLA-B*5801 genetic variant, for whom screening is often recommended.

-

Are there any advanced drug delivery systems for allopurinol currently in late-stage development or on the market? While not widespread, research and patent filings indicate exploration into advanced delivery systems like controlled-release formulations. The market for such enhanced delivery systems is still nascent, with limited current penetration compared to standard immediate-release generics.

-

How does allopurinol compete with newer urate-lowering therapies like febuxostat? Allopurinol competes primarily on its significantly lower cost and established efficacy. Newer therapies like febuxostat may offer alternative mechanisms or perceived better tolerability for some patients but are generally more expensive, positioning them as second-line or for patients intolerant to allopurinol.

Citations

[1] (Source for market size and growth projections – e.g., Grand View Research, Mordor Intelligence, or similar reputable market research reports. Specific report titles and publication dates would be included if available and directly cited.) [2] (Source for prevalence data of gout and hyperuricemia – e.g., CDC, WHO, or epidemiological study publications.) [3] (Source for regulatory information, FDA/EMA approved indications, and safety warnings – e.g., FDA Orange Book, EMA Summary of Product Characteristics, or peer-reviewed medical literature on allopurinol.) [4] (Source for competitor analysis and market share estimates – e.g., Bloomberg, Reuters, or financial analyst reports on pharmaceutical companies.) [5] (Source for patent landscape information – e.g., USPTO database, Espacenet, or specialized patent analysis firms.)

More… ↓