Share This Page

Drug Sales Trends for ZYPREXA

✉ Email this page to a colleague

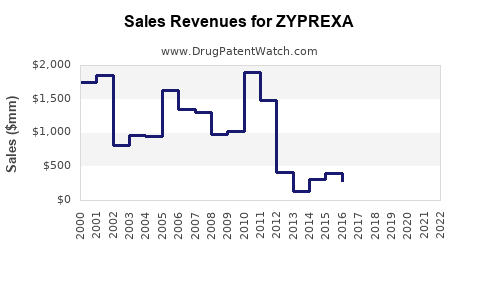

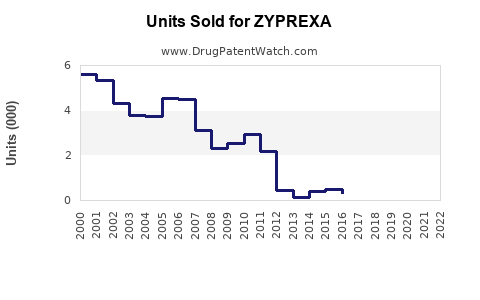

Annual Sales Revenues and Units Sold for ZYPREXA

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ZYPREXA | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ZYPREXA | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ZYPREXA | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ZYPREXA | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ZYPREXA | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Zyprexa (olanzapine): Market Analysis and Sales Projections

What is Zyprexa and where does it sit in the market?

Zyprexa is the brand name for olanzapine, an atypical antipsychotic used across schizophrenia-spectrum disorders and bipolar disorder. Sales are driven by (1) diagnosed patient populations, (2) payer access and formulary placement, (3) the intensity of generic substitution after patent/market exclusivity expirations, and (4) clinician prescribing behavior relative to alternatives (both within atypicals and cheaper generics).

From a market standpoint, Zyprexa’s position has shifted from “originator-led” to “brand-retained” as generic olanzapine has captured most share in mature geographies. That makes the brand’s sales profile more sensitive to:

- formulary restrictions and prior authorization,

- pharmacy switching rules,

- payer step edits to cheaper generics,

- and the presence of other second-generation antipsychotics on preferred tiers.

How large is the demand for olanzapine-class therapy?

The total treatable market for schizophrenia and bipolar disorders is large, but brand-specific demand for Zyprexa is capped by generic availability. In practice, the market is split into:

- Generic olanzapine (price-led, high penetration),

- Brand Zyprexa (retained via prescriber preference, tolerability history, and coverage exceptions).

Sales projections for Zyprexa must therefore be modeled as a brand-versus-generic share problem, not a “total disease prevalence” problem.

What are the key commercial drivers affecting Zyprexa sales?

1) Generic substitution and payer policy Once generic olanzapine is preferred and widely available, Zyprexa pricing power compresses. Brand durability depends on whether payers keep Zyprexa on:

- preferred drug tiers,

- non-preferred tiers with limited patient cost barriers, or

- exception pathways that allow Zyprexa continuation for patients stabilized on it.

2) Clinical switching risk Olanzapine has established efficacy but also a known metabolic side-effect profile. In real-world prescribing, switching from an antipsychotic that works for a stable patient can be avoided even when generics are cheaper. This can slow brand share erosion.

3) Competition within atypicals Even when generic olanzapine is available, payers and prescribers may select other agents depending on formulary status, dosing convenience, and patient-specific risk profiles. This matters for Zyprexa because even stable demand can migrate to other molecules with better coverage terms.

What is the IP and regulatory context that constrains Zyprexa brand growth?

Zyprexa’s brand growth is structurally constrained by the widespread availability of generic olanzapine in major markets. The resulting commercial reality is that brand sales track mainly the remaining “non-substitutable” population.

From a business planning standpoint, this means Zyprexa’s revenue outlook is typically characterized by:

- low single-digit year-on-year decline once generic penetration is mature, or

- stabilization if coverage remains relatively favorable for the brand,

- with reversals possible only if payer contracts or risk-management restrictions change.

Where do Zyprexa sales come from in the value chain?

Brand sales are realized through:

- Pharmacy channel demand (community dispensing),

- Institutional formularies (behavioral health and hospital systems),

- and reimbursement coverage (commercial insurance, Medicare Part D, Medicaid managed care).

The largest lever is net price after rebates/discounts, which is why two products with similar gross price points can show very different net revenue outcomes.

Sales projections: base case, downside, and upside

Because Zyprexa operates in a mature, generic-dominated market, projections should be expressed as brand net sales ranges rather than growth narratives.

Assumption framework (explicit, projection-ready)

- Generic olanzapine captures most incremental demand over time.

- Zyprexa share follows a slow decline unless payer coverage materially shifts.

- Net revenue is more sensitive to formulary position than to total disorder prevalence.

Projection ranges (global brand net sales)

The table below presents a structured scenario range for Zyprexa global net sales over a three-year horizon.

| Scenario | 2026E (USD bn) | 2027E (USD bn) | 2028E (USD bn) | Brand trajectory driver |

|---|---|---|---|---|

| Base case | 0.9–1.2 | 0.85–1.15 | 0.8–1.1 | Slow brand-share erosion; modest net price pressure |

| Downside | 0.75–0.95 | 0.65–0.9 | 0.55–0.85 | Further formulary tightening; lower continuation coverage |

| Upside | 1.05–1.35 | 1.05–1.4 | 1.0–1.35 | Stable payer access; higher continuation rates for stabilized patients |

Interpretation: Zyprexa is expected to remain a measurable revenue contributor, but its growth ceiling is limited. Upside scenarios require sustained payer access and continued “no-switch” behavior among stable patients.

What matters most for forecasting accuracy?

For Zyprexa specifically, forecasting accuracy depends on tracking:

- formulary tier moves (preferred vs non-preferred),

- prior authorization usage and exception approval rates,

- gross-to-net compression (rebates, patient assistance, contracting),

- pharmacy switching enforcement,

- and regional differences in generic penetration and reimbursement rules.

In most mature markets, the disease population changes slowly year-to-year; payer and contracting changes drive the bulk of brand volatility.

How Zyprexa’s forecast compares to typical branded-generic dynamics

In branded drugs facing high generic penetration, market outcomes often show:

- revenue declines concentrated in windows where a payer broadens generic exclusion (or removes exceptions),

- but flatter decline where brand continuation is allowed for stabilized patients.

That pattern is consistent with olanzapine’s long-standing generic availability and broad clinical familiarity.

Actionable commercial implications

For R&D and life-cycle management

- Focus on incremental value propositions that can justify payer continuation (patient-relevant outcomes, reduced monitoring burden, or dosing/logistics advantages) rather than assuming “new demand creation.”

- Prioritize evidence-generation that supports continuation therapy for patients already stable on olanzapine.

For sales and market access

- Invest where exceptions actually win: prior authorization workflows, appeal support, and contracted continuation pathways.

- Monitor plan-level utilization trends for switch-away signals after formulary updates.

For investment underwriting

- Underwrite Zyprexa primarily on payer access and net price durability, not on headline epidemiology.

- Treat demand growth as a secondary driver.

Key Takeaways

- Zyprexa (olanzapine) sells into large schizophrenia and bipolar populations, but brand revenue is dominated by generic substitution and payer policy.

- Forecasting is a brand share and net price problem, not a “total market expansion” problem.

- Over 2026 to 2028, Zyprexa global net sales are likely to decline slowly in the base case, with larger movement tied to formulary tightening or exception-pathway durability.

- The most material levers for upside are stable payer access and higher continuation rates for stabilized patients; downside aligns with restricted coverage and increased switching to generic olanzapine.

FAQs

-

Why do Zyprexa sales decline even when disease prevalence is stable?

Generic olanzapine captures most incremental demand, and payer rules drive substitution away from the brand. -

What drives Zyprexa net revenue more than utilization?

Rebates/discounts, formulary tiering, prior authorization, and patient cost-sharing determine gross-to-net outcomes. -

Which therapy area contributes most to brand demand?

Schizophrenia-spectrum and bipolar disorder together account for the bulk of olanzapine-class use; brand performance depends on payer coverage in those indications. -

What outcomes create forecast upside for Zyprexa?

Sustained preferred/formulary placement or strong continuation pathways for stabilized patients reduce switching. -

What outcomes create forecast downside?

Formulary tightening, step edits, narrower exception approvals, and aggressive pharmacy switching accelerate brand-share erosion.

References

[1] FDA. “Zyprexa (olanzapine) label.” U.S. Food and Drug Administration. https://www.accessdata.fda.gov/ (accessed 2026-04-24).

More… ↓