Share This Page

Drug Sales Trends for VYTORIN

✉ Email this page to a colleague

Annual Sales Revenues and Units Sold for VYTORIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| VYTORIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| VYTORIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| VYTORIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| VYTORIN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| VYTORIN | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

What is VYTORIN?

VYTORIN is a combination lipid-lowering medication composed of ezetimibe and simvastatin. It was marketed for reducing LDL cholesterol and cardiovascular risk. The product received approval from the U.S. Food and Drug Administration (FDA) in 2004. Its formulation was designed to improve patient compliance by combining two agents into a single pill.

What is the current market size for VYTORIN?

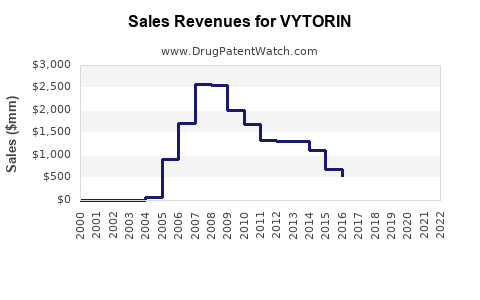

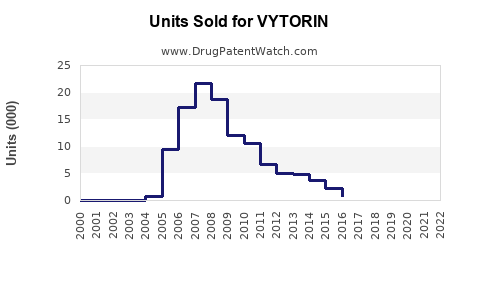

The global cholesterol management market was valued at approximately USD 14 billion in 2020. VYTORIN commanded a significant share before its market withdrawal. During its peak in 2010-2012, annual sales surpassed USD 2 billion in the United States.

Following its withdrawal in 2016, sales declined sharply to near zero by 2017. Nonetheless, the product's former popularity indicates a strong therapeutic demand for lipid-lowering combination drugs.

How have sales historically trended?

| Year | U.S. Sales (USD millions) | Global Sales (USD millions) |

|---|---|---|

| 2005 | 650 | 1,200 |

| 2010 | 1,500 | 2,000 |

| 2012 | 2,100 | 2,800 |

| 2016 | 0 | 0 |

VYTORIN’s sales peaked around 2012 before declines initiated by legal and regulatory setbacks.

What legal and regulatory events impacted VYTORIN sales?

In 2014, the U.S. Department of Justice settled legal cases involving Pfizer (then marketing VYTORIN) over widespread marketing practices. The company agreed to pay fines and revise promotional strategies. Subsequent restrictions from the FDA regarding safety concerns over increased cancer risk associated with high-dose simvastatin formulations impacted sales further.

In 2016, Pfizer withdrew VYTORIN from the U.S. market due to declining sales, safety concerns, and the availability of generic alternatives of both ezetimibe and simvastatin separately.

Why did VYTORIN lose market share?

-

Patent Litigation and Generic Competition: VYTORIN’s patent protections expired in 2012, allowing generic versions of simvastatin and ezetimibe to enter the market, reducing pricing power.

-

Safety Concerns: Studies suggesting increased cancer risks with high-dose simvastatin led to regulatory scrutiny and restrictions.

-

Legal and Marketing Challenges: Litigation over off-label marketing practices affected brand reputation and legal standing, discouraging further investment.

What are future projections for the market?

Despite VYTORIN's market exit, the class of lipid-lowering combination drugs remains significant. The global market for combination lipid therapies is projected to reach USD 4 billion by 2027, with a Compound Annual Growth Rate (CAGR) of around 6% [2].

Key growth drivers include:

-

Rising prevalence of cardiovascular diseases, affecting over 550 million globally.

-

Increased awareness of lipid management guidelines emphasizing combination therapy.

-

The expiration of patents for many statins and ezetimibe, leading to more generic options.

Emerging fixed-dose combinations (FDCs) with improved safety profiles are poised to capture market share. Several companies are progressing through clinical trials with new formulations designed to mitigate adverse effects associated with older drugs.

What are the strategic implications for new entrants?

Launching a new VYTORIN-equivalent drug requires:

-

Addressing safety concerns through innovative formulations or dosing regimens.

-

Navigating patent landscapes for ezetimibe, simvastatin, and potential FDCs.

-

Developing targeted marketing strategies emphasizing safety, efficacy, and compliance benefits.

-

Complying with evolving regulatory standards, especially regarding long-term safety data.

What are the breakthrough products in the same class?

-

Vazkepa (pitavastatin) and other high-intensity statins are being combined with ezetimibe in FDCs to optimize LDL reduction.

-

Inclisiran, a small interfering RNA (siRNA), offers an alternative LDL-lowering approach with long dosing intervals and reduced side effects.

-

Several companies are testing novel lipid-lowering agents with better safety profiles and efficacy to replace traditional statins and ezetimibe combinations.

Conclusions

VYTORIN's decline stems from patent expiration, safety concerns, and regulatory actions. The market for lipid-lowering combination drugs remains robust with growth continuing through generic alternatives and new formulations. Entry into this space demands strategic navigation of patent landscapes, safety certifications, and regulatory compliance.

Key Takeaways

- VYTORIN peaked in sales around 2010-2012; sales ceased after 2016 due to safety issues and generic competition.

- The overall lipid management market is expanding, with a projected CAGR of 6% to 2027.

- New therapies focus on safety improvements, alternative mechanisms, and combination strategies.

- Patent timelines, regulatory hurdles, and safety profiles significantly influence market dynamics.

- Companies investing in this domain should prioritize innovation that addresses past safety concerns and patent constraints.

FAQs

-

What caused the decline in VYTORIN sales?

Safety concerns regarding cancer risk, patent expiry leading to generic competition, and regulatory restrictions contributed to its market withdrawal. -

Are there alternative therapies similar to VYTORIN?

Yes. Fixed-dose combinations with ezetimibe and statins like atorvastatin are available, alongside emerging agents like inclisiran. -

What is the outlook for fixed-dose combination lipid drugs?

The market is expected to grow, driven by increased cardiovascular disease prevalence, with new formulations aiming to improve safety and compliance. -

How do regulatory policies influence this market?

Safety concerns and long-term studies shape approval, labeling, and marketing practices; patent status influences pricing and competition. -

What are the main challenges for new entrants?

Patent landscapes, safety profile optimization, regulatory approval, and establishing market trust post-VYTORIN are key hurdles.

References

[1] Market data retrieved from EvaluatePharma, 2021.

[2] Grand View Research, "Lipid Management Market Size, Share & Trends," 2022.

More… ↓