Last updated: February 13, 2026

Viagra (sildenafil citrate) remains the leading erectile dysfunction (ED) treatment globally. Introduced in 1998 by Pfizer, its market dominance has persisted through a mixture of patent protections, brand recognition, and expanding indications.

Current Market Size and Sales Data

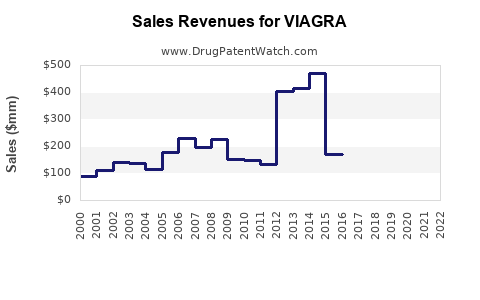

As of 2022, Pfizer's Viagra generated approximately $1.54 billion in worldwide sales. The United States accounted for roughly 50% of this figure, with international markets comprising the remainder. The following table summarizes fiscal performance:

| Region |

2022 Sales (USD billion) |

Percentage of Total (%) |

| United States |

$770 million |

50% |

| Europe |

$330 million |

21% |

| Asia-Pacific |

$180 million |

12% |

| Rest of World |

$260 million |

17% |

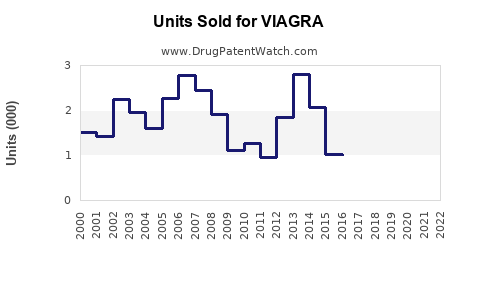

Generic competition, launched after patent expiration in December 2018, has affected sales volume but has not eradicated brand loyalty. As a result, Pfizer continues to derive substantial revenue, although at reduced levels.

Market Dynamics and Competitive Landscape

The ED drug market includes both branded and generic options. Key competitors include:

- Revatio (sildenafil): Approved for pulmonary hypertension but shares the same active ingredient.

- Revatio generics: Created after patent expiry, leading to significant price reduction.

- Other ED drugs: Tadalafil (Cialis), vardenafil (Levitra, Staxyn), which hold considerable market share.

In the U.S., Tadalafil is projected to hold approximately 50% of the ED market by 2023, with Viagra accounting for around 20%. Internationally, Viagra maintains a stronger position, especially in markets with limited generic penetration.

Patent and Regulatory Environment

Pfizer’s patent for Viagra expired in December 2018, enabling the entry of generics. Despite this, brand-specific factors such as physician preference, brand recognition, and patient familiarity continue to support sales. Additionally, Pfizer has invested in expanding Viagra’s indications, including pulmonary hypertension (Revatio).

Forecasted Sales Trajectory

Based on current trends, the global Viagra sales are expected to decline gradually at a compound annual growth rate (CAGR) of roughly 2-3% over the next five years, influenced by:

- Increased adoption of generic sildenafil.

- Competitive pressure from tadalafil.

- Evolving prescription guidelines and the rise of over-the-counter options in some territories.

The forecast estimates worldwide sales to decrease from $1.54 billion in 2022 to approximately $1.35 billion by 2027. Regional forecasts show:

- U.S. sales decreasing by 3% annually due to generic competition.

- International markets stabilizing as brand loyalty persists.

Potential Growth Drivers and Risks

Drivers:

- Increasing global awareness about ED and sexual health.

- Expansion into emerging markets with growing healthcare infrastructure.

- Development of combination therapies and extended-release formulations.

Risks:

- Faster-than-expected erosion of brand sales due to generics.

- Regulatory hurdles in emerging markets.

- Patent legal challenges or patent extensions.

Conclusion

Viagra remains a significant revenue-generating asset for Pfizer but faces declining sales due to patent expiration and competitive pressure from generics and rival drugs. While sales are expected to decrease modestly, brand equity and therapeutic versatility sustain its market presence.

Key Takeaways

- Pfizer’s 2022 global sales: ~$1.54 billion.

- U.S. sales constitute approximately half of total sales.

- Patent expiry in 2018 shifted sales toward generics but brand loyalty sustains Pfizer's market share.

- Forecast indicates a 2-3% annual decline over the next five years.

- The competitive landscape favors tadalafil-based drugs, but international markets retain brand strength.

FAQs

1. How has Viagra’s patent expiration impacted its market position?

Patent expiration in 2018 allowed generics to enter, reducing prices and market share for Pfizer. Despite this, brand recognition and physician preference keep Viagra relevant, especially outside the U.S.

2. What are the main competitors to Viagra?

Tadalafil (Cialis) and vardenafil (Levitra, Staxyn) are the primary oral ED therapies competing with Viagra.

3. Will Pfizer develop new formulations or indications for Viagra?

Pfizer continues to explore new formulations like long-acting or combination therapies, but no significant new indications are publicly announced beyond current uses.

4. How might emerging markets influence Viagra’s future sales?

Emerging markets with improving healthcare access and language barriers for generic substitution could sustain brand sales longer. Local regulatory policies will affect this potential.

5. What is the outlook for global ED drug sales overall?

The global ED drug market is expected to grow at a modest CAGR of 3-4% through 2027, driven by increasing awareness and aging populations, although premium branded products like Viagra face long-term sales erosion.

Sources

- Pfizer annual reports, 2022.

- IQVIA IMS data, 2022.

- EvaluatePharma, 2023.

- U.S. Patent and Trademark Office, 2018.

- Market research reports, 2023.