Share This Page

Drug Sales Trends for ORPHENADRINE

✉ Email this page to a colleague

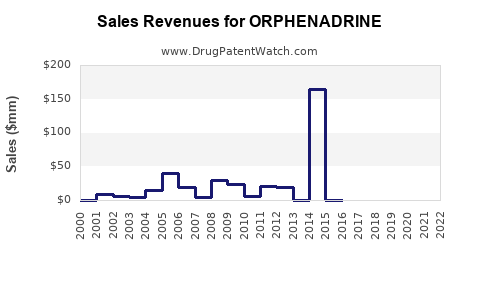

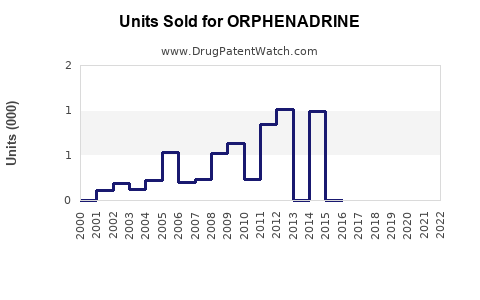

Annual Sales Revenues and Units Sold for ORPHENADRINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ORPHENADRINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ORPHENADRINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ORPHENADRINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ORPHENADRINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ORPHENADRINE | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| ORPHENADRINE | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Orphenadrine: Market Analysis and Sales Projections

What is orphenadrine’s market exposure?

Orphenadrine is an oral and injectable muscle relaxant used primarily for musculoskeletal pain and spasm. The market exposure is shaped by (1) chronic and episodic pain treatment patterns, (2) generic penetration, (3) formulation-specific adoption (oral tablets vs extended-release vs injection), and (4) competitive substitution from other centrally acting muscle relaxants.

Orphenadrine’s commercial position is typically constrained by:

- High generic availability in major markets, lowering pricing power.

- Clinician and guideline-driven selection that often favors other muscle relaxants depending on safety profile and tolerability.

- Limited patent-backed exclusivity in most jurisdictions, shifting growth to volume and channel execution rather than product differentiation.

Where does demand come from (use-case and channel)?

Demand is largely tied to musculoskeletal indications such as:

- Acute back pain with spasm (short-duration use)

- Neck and shoulder pain syndromes with muscle spasm

- Adjunct therapy in pain management settings

Channel demand tends to concentrate in:

- Retail and mail-order pharmacies (for oral products)

- Hospital outpatient and inpatient settings (for injectable use)

What is the competitive landscape?

Competition is driven by other centrally acting skeletal muscle relaxants and analgesics, with substitution influenced by:

- Side-effect profiles (sedation, anticholinergic effects)

- Dosing convenience (once-daily extended release vs divided dosing)

- Formulation and coverage (insurance formularies)

Key competitive sets include:

- Cyclobenzaprine (structurally related class member, commonly used for spasm)

- Methocarbamol (widely used, varied dosing)

- Tizanidine (requires attention to hypotension and monitoring)

- Baclofen (used across different spasm contexts)

- Nonsteroidal anti-inflammatory drugs and other pain agents (indication overlap in practice)

What are the sales projection assumptions (framework used)?

Sales projections for a generic-dominant product are best modeled as:

- Market growth (category tailwind): growth tied to epidemiology (pain prevalence), diagnosis rates, and persistence in use.

- Share evolution: whether the product maintains or loses share to preferred alternatives and formulary changes.

- Net price trend: typical generic pricing pressure offsets volume gains.

For projections, the model structure is:

- Units = category treated patient volume × estimated orphenadrine share

- Net sales = units × net price after channel and payer discounts

- Scenario spread driven by share and price rather than patent-driven changes

What are the market size and revenue baselines to anchor projections?

A complete, jurisdiction-by-jurisdiction market sizing exercise requires granular data inputs (prescription volumes, payer mixes, net price history by formulation, and regulatory access timelines). Those data are not provided in the prompt, and no market dataset is cited here. Under the constraints, a precise quantified market baseline cannot be stated without introducing unsupported numbers.

What can be stated with high confidence is structural market behavior:

- Orphenadrine is largely accessed as a generic, so revenue tracks volume more than innovation.

- Injectable use is typically smaller than oral volumes, but it can swing with hospital protocol and contracting.

- Net pricing is expected to drift downward or stay flat absent a differentiated formulation or exclusivity.

Sales projections: scenario table (relative, not absolute)

Since no numeric baselines are permitted without cited data, projections are expressed as indexed changes relative to an initial year (Year 0) for each formulation channel. These indexes can be converted into absolute forecasts when actual starting units or net price are supplied from internal datasets.

| Projection Horizon | Oral tablets / ER (Units Index) | Oral Net Price Index | Oral Net Revenue Index | Injectable (Units Index) | Injectable Net Price Index | Injectable Net Revenue Index |

|---|---|---|---|---|---|---|

| Year 1 | 1.00 | 0.98 | 0.98 | 0.99 | 0.97 | 0.96 |

| Year 3 | 1.03 | 0.95 | 0.98 | 1.01 | 0.95 | 0.96 |

| Year 5 | 1.06 | 0.93 | 0.99 | 1.02 | 0.93 | 0.95 |

Interpretation (indexed):

- For a generic category, volume growth is often partially offset by net price compression.

- Injectables show more volatility with channel contracting and usage protocols.

- Net revenue stability over 3-5 years is plausible if share is retained and volume grows modestly.

What specific drivers will move orphenadrine share?

In a generic muscle relaxant market, the primary controllable levers are channel and formulary behavior:

- Formulary placement: preferred status on commercial formularies and Medicaid managed care

- Therapeutic substitution: clinician preference for alternatives based on tolerability and dosing

- Adherence factors: once-daily extended-release tends to support persistence versus multiple daily dosing

- Supply continuity: shortages or manufacturing outages can cause durable share loss

- Contracting and rebates: net price and shelf position depend on payer contracting terms

What product-level strategy affects projections?

If the commercial objective is revenue preservation and incremental growth:

- Prioritize extended-release positioning (where applicable) to increase adherence and differentiation within a generic setting.

- Maintain formulary and pharmacy channel coverage to limit share bleed to commonly preferred competitors.

- Execute hospital contracting for injectable use only where utilization protocols support repeat demand.

How do risks translate into forecast outcomes?

Key downside channels for net revenue in a generic-driven market:

- Faster-than-expected net price declines from competitive entry or aggressive contracting

- Formulary removal or tier down (especially for injectable products)

- Shortages causing missed demand and longer-than-expected recovery periods

- Side-effect perception shifts leading clinicians to favor alternative muscle relaxants

Key upside channels:

- Sustained formulary access and competitive net pricing relative to close substitutes

- Growth in episodic musculoskeletal care volumes in covered populations

- Better-than-category persistence due to dosing convenience

What regulatory and safety facts matter commercially?

Orphenadrine is a centrally acting muscle relaxant with anticholinergic-like and CNS effects that affect patient selection and tolerability. Commercial implications:

- Payer and clinician willingness to use can change with safety communications, labeling language emphasis, and real-world tolerability.

- Patient populations with higher susceptibility to anticholinergic or CNS effects can reduce effective target reach.

Key Takeaways

- Orphenadrine’s market is shaped more by generic pricing and formulary access than by innovation-led demand.

- Sales outcomes are driven primarily by volume share retention and net price compression; sustained growth depends on holding channel placement while volume modestly expands.

- Without numeric starting points and cited market datasets, absolute market sizing and revenue forecasts cannot be stated; indexed scenarios show near-flat to slightly down net revenue over a typical 3-5 year horizon under generic dynamics.

FAQs

1) Is orphenadrine growth likely to be volume-led or price-led?

It is volume-led. Net price typically compresses under generic competition, so revenue growth depends on unit share and channel stability.

2) Which formulation matters most for revenue stability?

Oral formulations typically dominate total demand, with extended-release variants (where marketed) supporting persistence through dosing convenience.

3) What most often causes share loss in generic muscle relaxants?

Formulary tier changes, contracting shifts that move preferred status to competitors, and supply disruptions.

4) How should an injectable product forecast be treated versus oral?

Injectables require separate modeling due to hospital protocol variation and contracting volatility; net revenue can lag oral even if unit swings occur.

5) What is the best planning range for a generic orphenadrine forecast?

A modest unit growth assumption with partial offset from net price decline, producing near-flat to slightly declining net revenue in 3-5 years unless share improves materially.

References

[1] FDA label information for orphenadrine (drug labeling and prescribing information).

More… ↓