Share This Page

Drug Sales Trends for LEVETIRACETA

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for LEVETIRACETA (2018)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

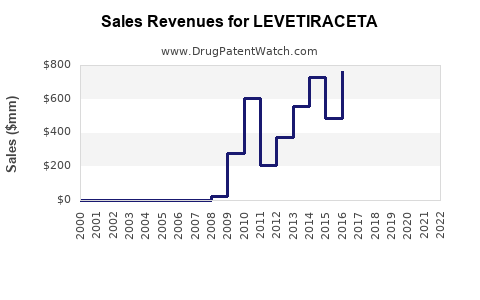

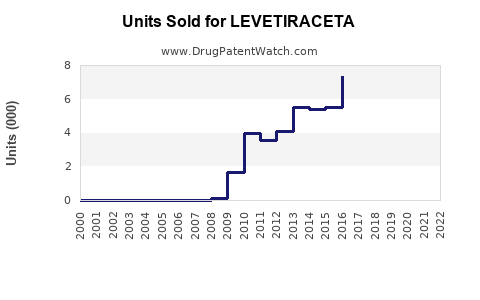

Annual Sales Revenues and Units Sold for LEVETIRACETA

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LEVETIRACETA | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LEVETIRACETA | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LEVETIRACETA | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LEVETIRACETA | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| LEVETIRACETA | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| LEVETIRACETA | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| LEVETIRACETA | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Levetiracetam Market Analysis and Sales Projections

Levetiracetam, an antiepileptic drug (AED), faces a dynamic market influenced by patent expirations, generic competition, and evolving treatment landscapes. The drug, initially launched by UCB Pharma, has seen its market share significantly impacted by the availability of multiple generic versions, leading to price erosion and a shift in market dynamics. Despite these pressures, its efficacy in treating partial-onset seizures, myoclonic seizures, and primary generalized tonic-clonic seizures maintains its relevance in epilepsy management.

Market Overview and Competitive Landscape

The global market for levetiracetam is characterized by a high degree of competition due to its patent expiry in major markets. The original branded drug, Keppra, has been surpassed by a multitude of generic manufacturers. This has resulted in a commoditized market where price is a primary differentiator.

-

Key Market Drivers:

- Increasing prevalence of epilepsy globally.

- Growing awareness and diagnosis of seizure disorders.

- Established efficacy and safety profile of levetiracetam compared to some older AEDs.

- Availability of various formulations (oral tablets, oral solution, intravenous).

-

Key Market Challenges:

- Intense price competition from generic manufacturers.

- Development of newer antiepileptic drugs with potentially improved efficacy or fewer side effects.

- Reimbursement policies and formulary restrictions in different healthcare systems.

- The emergence of biosimil or similar complex generics for newer biologics could indirectly impact the market for small molecule drugs like levetiracetam by shifting R&D focus.

The competitive landscape for levetiracetam includes both originator companies that have seen their market exclusivity wane and a vast array of generic pharmaceutical companies. Major generic players actively involved in the levetiracetam market include Teva Pharmaceutical Industries, Mylan N.V. (now part of Viatris), Sun Pharmaceutical Industries, and numerous others.

| Product Name | Manufacturer(s) | Status | Market Impact |

|---|---|---|---|

| Keppra | UCB Pharma | Branded (Originator) | Initial market leader; reduced market share due to generics |

| Levetiracetam (Generic) | Teva, Mylan, Sun Pharma, etc. | Generic | Dominant market presence; price-driven competition |

The primary therapeutic indications for levetiracetam are:

- Adjunctive therapy for partial-onset seizures in patients one month of age and older.

- Adjunctive therapy for myoclonic seizures in patients 12 years of age and older with juvenile myoclonic epilepsy.

- Adjunctive therapy for primary generalized tonic-clonic seizures in patients six years of age and older with idiopathic generalized epilepsy.

The drug's mechanism of action involves binding to synaptic vesicle protein 2A (SV2A), a protein widely distributed in the central nervous system, though its precise role in seizure control is not fully elucidated. This distinct mechanism differentiates it from many other AEDs.

Patent Landscape and Generic Entry

The patent protection for levetiracetam has long expired in key markets such as the United States and Europe. The primary patents covering the compound and its uses were filed in the late 1980s and early 1990s. For instance, the foundational patent for levetiracetam was filed in the U.S. in 1989 and granted in 1993 [1].

- US Patent Expiration: Key patents expired by the mid-2010s, paving the way for widespread generic manufacturing.

- European Patent Expiration: Similar expiration timelines occurred in European countries, with extensions for pediatric use often expiring around the same period.

- Formulation Patents: While compound patents have expired, some companies may hold patents on specific formulations or delivery methods. However, these typically offer limited market protection against straightforward generic equivalents.

The generic entry of levetiracetam commenced in earnest following these patent expiries. This event is consistently a major disruptor in the pharmaceutical market, leading to a significant decline in the market share and revenue for the originator brand and a proliferation of affordable generic alternatives.

The legal challenges surrounding patent expiry and generic challenges are a constant feature. In the case of levetiracetam, the expiry of core patents allowed generic manufacturers to launch their products without significant patent-related litigation that would delay market entry, unlike cases involving more recent drug approvals with extended patent lifecycles or complex formulation patents.

Sales Performance and Market Projections

Levetiracetam's sales performance has transitioned from high growth during its patent-protected period to a mature, volume-driven market post-genericization. The originator brand, Keppra, experienced peak sales before generic erosion. The total market value is now largely determined by the aggregate sales of all levetiracetam products, including generics.

- Originator Sales Decline: UCB Pharma's Keppra sales peaked in the billions of dollars annually. Post-patent expiry, these sales have significantly contracted, with the company focusing on newer drugs and specialty markets.

- Generic Market Growth: The market value for levetiracetam is now driven by the volume of units sold by numerous generic manufacturers. While the total market value might be lower than during the branded era, the volume of prescriptions remains substantial.

Global Levetiracetam Market Value (Estimated 2020-2025, USD Billions)

| Year | Estimated Market Value (USD Billion) |

|---|---|

| 2020 | 1.8 - 2.2 |

| 2021 | 1.7 - 2.1 |

| 2022 | 1.6 - 2.0 |

| 2023 | 1.5 - 1.9 |

| 2024 | 1.4 - 1.8 |

| 2025 | 1.3 - 1.7 |

Note: These figures represent the total market value including branded and generic versions. Projections are based on current trends of price erosion and volume stability.

Factors Influencing Future Sales Projections:

- Epidemiological Trends: The incidence and prevalence of epilepsy are critical. According to the World Health Organization, epilepsy affects approximately 50 million people worldwide [2]. A stable or increasing prevalence will sustain demand.

- Competition from Newer AEDs: The development of novel antiepileptic drugs offering improved tolerability, broader efficacy spectrums, or specific benefits for refractory epilepsy could gradually displace levetiracetam in certain patient populations. For example, drugs targeting sodium channels or GABA receptors with novel mechanisms continue to emerge.

- Generic Competition Intensification: As more companies enter the generic levetiracetam market, price competition is likely to intensify, potentially leading to further price reductions and a stable or slightly declining market value in nominal terms, even if unit sales remain high.

- Geographic Market Variations: Developed markets like North America and Europe will continue to be dominated by generics, with stable but declining revenues for branded Keppra. Emerging markets in Asia-Pacific and Latin America may see sustained demand and a slower transition to generics, offering some growth potential for generic manufacturers.

- Treatment Guidelines: Updates to epilepsy treatment guidelines by professional organizations (e.g., American Academy of Neurology, American Epilepsy Society) can influence prescribing patterns. Levetiracetam's position as a first or second-line agent for certain seizure types supports its continued use.

- Formulation Innovation: While unlikely to be a major driver, any successful development of novel formulations (e.g., extended-release, improved palatability for pediatric use) could capture a niche market segment, but this is less probable for a mature genericized drug.

Sales projections for levetiracetam indicate a mature market characterized by volume sales and price sensitivity. The overall market value is expected to continue a gradual decline in nominal terms, driven primarily by aggressive generic pricing. However, the sustained need for effective epilepsy treatments ensures a stable demand for levetiracetam in terms of units.

Regulatory Environment and Market Access

The regulatory landscape for levetiracetam is well-established, with approvals granted by major regulatory bodies worldwide, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA).

- FDA Approval: Levetiracetam was first approved by the FDA in 1999.

- EMA Approval: Approval was granted by the EMA shortly thereafter.

- Pediatric Exclusivity: Extensions for pediatric use were granted, providing additional market exclusivity for the branded product in certain indications. These extensions have also expired.

Market Access Considerations:

- Reimbursement: Levetiracetam is widely reimbursed by public and private health insurance providers globally. The significant price reduction offered by generics has made it an attractive option for payers aiming to control healthcare costs.

- Formulary Placement: Due to its efficacy and cost-effectiveness as a generic, levetiracetam is commonly included on hospital and insurance formularies. Interchangeable biosimilar substitution rules in some regions might also apply, although this is more common for biologics.

- Off-Label Use: While primarily used for epilepsy, research has explored its potential use in other neurological conditions, but epilepsy remains its principal indication.

The generic market access is facilitated by the drug's established safety and efficacy profile, which simplifies the regulatory approval process for generic manufacturers. Companies can rely on bioequivalence studies to demonstrate comparability to the reference listed drug.

Comparative Drug Analysis

Levetiracetam competes within the broader antiepileptic drug market. Its key differentiators include its unique mechanism of action and generally favorable tolerability profile compared to some older AEDs.

Levetiracetam vs. Key Competitors:

| Drug Name | Mechanism of Action | Primary Indications | Key Differentiators | Market Position Relative to Levetiracetam |

|---|---|---|---|---|

| Levetiracetam | Binds to SV2A | Partial-onset, myoclonic, generalized tonic-clonic seizures | Unique mechanism, generally good tolerability, broad efficacy | Mature, genericized market; volume-driven; price competitive. |

| Valproic Acid | Increases GABAergic neurotransmission, blocks Na+ channels | Broad spectrum (partial, generalized, absence, myoclonic) | Long history of use, effective for multiple seizure types; teratogenicity concerns | Mature, genericized market; still a first-line option for some indications, but side effect profile limits use. |

| Lamotrigine | Blocks voltage-gated sodium channels | Adjunctive for partial-onset, generalized tonic-clonic seizures | Broad efficacy, relatively good tolerability; potential for rash (SJS) | Also widely genericized; competitive with levetiracetam, particularly for certain patient profiles. |

| Topiramate | Blocks Na+ channels, potentiates GABA, inhibits glutamate receptors | Adjunctive for partial-onset, generalized tonic-clonic seizures | Broad efficacy, multiple mechanisms; cognitive side effects, kidney stone risk | Genericized; competes with levetiracetam, but tolerability profile may favor levetiracetam for some patients. |

| Lacosamide | Slows voltage-gated sodium channel inactivation | Adjunctive for partial-onset seizures | Novel mechanism, potential for better tolerability than some older AEDs | Newer, branded products often command higher prices; still in a growth phase relative to levetiracetam. |

| Brivaracetam | High affinity for SV2A (more than levetiracetam) | Adjunctive for partial-onset seizures | Higher affinity for SV2A, potentially improved efficacy/tolerability | Developed by UCB; positioned as a next-generation SV2A binder, targeting niche improvements. |

The existence of newer AEDs like lacosamide and brivaracetam, which offer potentially enhanced efficacy or different tolerability profiles, poses a long-term competitive threat. However, their higher cost and more specialized indications mean they are unlikely to fully displace levetiracetam, especially in price-sensitive markets or for patients who tolerate levetiracetam well. The generics of levetiracetam will continue to offer a cost-effective standard of care.

Key Takeaways

- The levetiracetam market is characterized by widespread generic competition following patent expirations, leading to significant price erosion and a shift to a volume-driven sales model.

- Demand for levetiracetam remains robust due to the prevalence of epilepsy and its established efficacy and tolerability profile.

- Sales projections indicate a mature market with a gradual decline in nominal value driven by aggressive generic pricing, though unit sales are expected to remain high.

- Newer antiepileptic drugs offer competition but are unlikely to entirely supplant levetiracetam due to cost, indication breadth, and established generic availability.

- Market access is generally favorable due to levetiracetam's inclusion on formularies as a cost-effective treatment option.

Frequently Asked Questions

-

What is the primary driver of levetiracetam sales today? The primary driver is the volume of prescriptions filled by generic levetiracetam products, serving as a cost-effective treatment for epilepsy.

-

How do new antiepileptic drugs impact levetiracetam sales? Newer drugs offer potential for improved efficacy or tolerability and may capture market share in specific patient segments, but levetiracetam's established profile and low cost continue to support its broad use.

-

What is the expected trend for levetiracetam pricing in the next five years? Pricing is expected to continue its downward trend due to intense generic competition, with further incremental reductions as market dynamics evolve.

-

Are there any significant patent challenges ongoing for levetiracetam? The primary patents covering the levetiracetam compound have expired; current market activity is focused on generic manufacturing and distribution rather than patent litigation for market exclusivity.

-

Which geographic regions represent the largest markets for levetiracetam? North America and Europe currently represent the largest markets, with significant contributions from emerging markets in Asia-Pacific and Latin America as generic adoption increases.

Citations

[1] U.S. Patent No. 5,637,712. (1997). 1-substituted-2-pyrrolidinone derivatives.

[2] World Health Organization. (2023, October 27). Epilepsy. https://www.who.int/news-room/fact-sheets/detail/epilepsy

More… ↓