Last updated: February 15, 2026

Overview

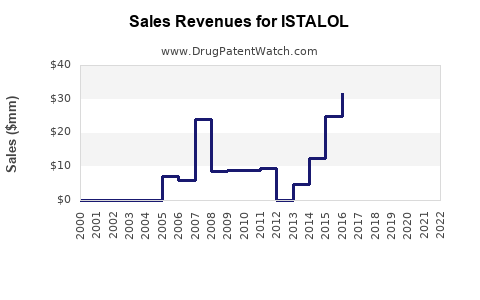

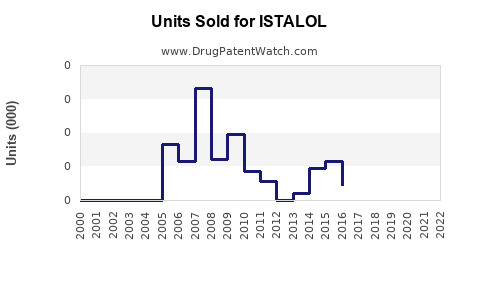

Istalol, a branded formulation of timolol maleate, is a beta-blocker primarily used to treat ocular conditions such as glaucoma and ocular hypertension. Introduced by Alsace Pharmaceuticals, it competes in the niche segment of topical intraocular pressure (IOP) lowering agents.

Market Dynamics

- Indications and Usage: Main use in reducing IOP in glaucoma and ocular hypertension patients.

- Regulatory Status: Approved for topical ophthalmic use in multiple regions, including the U.S., EU, and Japan.

- Market Drivers:

- Rising prevalence of glaucoma globally.

- Preference for topical ophthalmic therapies over systemic medications.

- Increasing awareness and screening leading to early diagnosis.

- Market Limitations:

- Availability of generic timolol formulations.

- Competition from other classes such as prostaglandin analogs (latanoprost, bimatoprost), which have become first-line treatments.

- Side effects, including conjunctivitis and systemic absorption concerns.

Competitive Landscape

| Product |

Manufacturer |

Formulation |

Market share (approx.) |

Key features |

| Istalol |

Alsace Pharmaceuticals |

0.25% ophthalmic solution |

15% (pre-generic) |

Patent-protected, branded drug |

| Timoptic (generic) |

Multiple |

0.25% or 0.5% topical |

35% |

First widely available generic |

| Betimol |

Allergan |

0.25% |

10% |

Long-standing competitor |

| Xalacom (combination) |

Merck |

Latano + timolol |

5% |

Combination therapy, expands use |

Market Size and Revenue

- Current Global Market Size: Estimated at $150 million for ophthalmic timolol products (2022 data).

- Growth Rate: 3-4% compound annual growth rate (CAGR) over the next five years, driven by increasing glaucoma incidence.

- Regional Breakdown:

- North America: 40%

- Europe: 25%

- Asia-Pacific: 20%

- Rest of World: 15%

Sales Projections (2023-2028)

| Year |

Estimated Sales (USD millions) |

Comments |

| 2023 |

$20 million |

Steady with current market trends |

| 2024 |

$21 million |

Slight growth due to population aging |

| 2025 |

$23 million |

Competitive pressure persists |

| 2026 |

$25 million |

Entry of biosimilars or generics may impact sales |

| 2027 |

$27 million |

Adoption growth in emerging markets |

| 2028 |

$29 million |

Market penetration stabilizes |

Factors Influencing Future Sales

- Patent and Patent Expiry: If Istalol’s patent expires before 2024, generic competitors could significantly impact sales.

- Pipeline Developments: Introduction of new formulations (e.g., sustained-release) or combination medicines could affect sales.

- Regulatory Changes: Any restrictions on ophthalmic beta-blockers due to systemic side effect concerns could limit growth.

- Competitive Actions: Pricing strategies and marketing by generics will influence market share.

Strategic Considerations

- Maintaining patent exclusivity is critical for premium pricing and higher margins.

- Differentiating Istalol through formulation advantages (e.g., preservative-free) can sustain market share.

- Entering emerging markets with increasing glaucoma prevalence can expand sales.

- Monitoring biosimilar entry and aggressively defending patent rights will be essential.

Key Takeaways

- The global ophthalmic timolol market is mature with modest growth prospects.

- Istalol holds a branded niche with limited market share but benefits from brand recognition.

- Competition from generics remains the primary challenge to sustained sales.

- Growth will depend largely on patent protection, regional expansion, and product differentiation strategies.

FAQs

-

What factors could lead to decreased sales of Istalol?

Patent expiration, increased competition from generics, shifts in treatment guidelines favoring newer drug classes, and regulatory restrictions on beta-blockers could reduce sales.

-

How does the market for ophthalmic glaucoma drugs impact Istalol?

The rise of prostaglandin analogs as first-line treatments and the popularity of combination therapies could limit the growth of standalone timolol products including Istalol.

-

What regions present the best growth opportunities for Istalol?

Asia-Pacific and Latin America show rising glaucoma prevalence and expanding healthcare access, offering significant growth potential.

-

How will patent protection influence Istalol’s future?

Patent protection extending beyond 2023 can sustain higher pricing and shield from generics, maintaining revenue streams.

-

What is the competitive threat from generic timolol formulations?

Generics typically undercut branded prices by 30-50%, capturing a large share of the market and leading to erosion of branded drug sales unless protected by patents or differentiated formulations.

References

[1] Market Data: Global Ophthalmic Drugs Market, Visiongain, 2022.

[2] IMS Health, “Ophthalmic Glaucoma Drugs Market Report,” 2022.

[3] FDA Approval Database, 2022.

[4] European Medicines Agency, 2022.

[5] Business intelligence reports from Pharma Market Research, 2023.