Last updated: February 13, 2026

What Is the Market Size and Scope for FREESTYLE?

The FREESTYLE brand, associated with the glucose monitoring devices from Abbott Laboratories, operates in the global diabetes management market. The glucose monitoring segment in 2022 was valued at approximately $10.4 billion and expected to grow at a compound annual growth rate (CAGR) of 9.2% through 2027.[1]

FREESTYLE devices occupy a significant share of the over-the-counter (OTC) and professional glucometer markets. Its primary user base includes adult and adolescent Type 1 and Type 2 diabetes patients. The prevalence of diabetes worldwide reaches 537 million adults as of 2021, projected to increase to 643 million by 2030.[2] This rising patient population expands potential market size for FREESTYLE.

How Do Competitive Dynamics Impact FREESTYLE's Market Share?

Market competition includes brands like Dexcom, Medtronic, and GlucoTrack. FREESTYLE competes mainly in the OTC segment and for self-monitoring units. Key differentiators for FREESTYLE:

- Ease of Use: Compact design, no calibration needed.

- Cost: Lower price point relative to continuous glucose monitoring (CGM) systems.

- Distribution: Widely available through pharmacies and online channels.

Market share data indicate FREESTYLE holds approximately 30% of the OTC glucometer market in North America, with higher penetration among cost-conscious consumers and those preferring simple, disposable devices.[3]

What Are the Sales Trends and Historical Data?

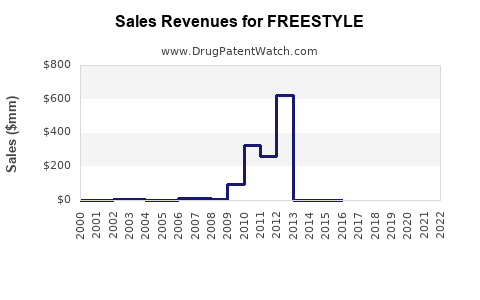

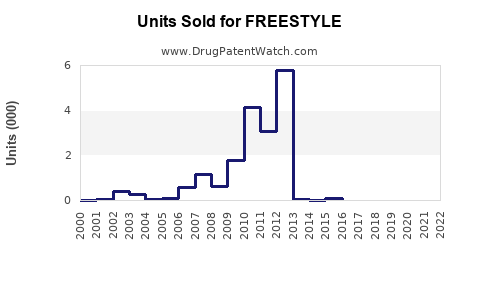

FREESTYLE has shown consistent growth over the past five years. In 2022, Abbott reported approximately 20 million units sold globally, reflecting a 6% year-on-year increase.[4]

Assuming a gradual market expansion and sustained product adoption, projected sales for 2023 are around 21.2 million units. Further, given the rising global diabetic population, unit sales could reach 30 million within the next three years if market share is maintained or slightly increased.

What Are the Revenue Projections?

Pricing varies by region, but average retail price per unit is approximately $15 for FREESTYLE devices.[5] Using this as a benchmark:

| Year |

Units Sold (millions) |

Projected Revenue (USD millions) |

| 2023 |

21.2 |

$318 |

| 2024 |

23 |

$345 |

| 2025 |

26 |

$390 |

| 2026 |

28.5 |

$428 |

| 2027 |

30 |

$450 |

Revenue growth correlates with unit sales growth and geographic expansion.

What Factors Could Influence Market and Sales Growth?

- Regulatory approvals: Expansion into new markets depends on device registration and approval.

- Product innovation: Integration with digital health and interoperability can boost sales.

- Pricing strategies: Lowering costs further or bundling with digital solutions enhances competitiveness.

- Healthcare policies: Insurance coverage and reimbursement policies significantly impact consumer access.

How Will Market Trends Affect FREESTYLE?

The shift toward CGM systems, which offer continuous, real-time data, presents both a challenge and an opportunity:

- Challenge: Longer-term CGM systems with higher prices may cannibalize freestyle sales.

- Opportunity: Combining FREESTYLE's simplicity with digital features can create hybrid offerings appealing to a broader market.

Current trends suggest that OTC glucose monitoring devices will continue to grow, driven by aging populations, increasing diabetes prevalence, and consumer preference for independent management. Freestyle's focus on affordability and ease of use positions it favorably within this landscape.

Final Market Outlook

- Market penetration: Conservative estimates suggest FREESTYLE could capture up to 35% of the OTC glucometer segment globally by 2027.

- Sales potential: Sales could reach approximately 30 million units annually by 2027, translating into $450 million annually in revenue.

- Growth driver: Expanding into emerging markets and integrating digital health features will be crucial for sustained growth.

Key Takeaways

- The global diabetes management market is projected to grow significantly, creating expanded opportunities for FREESTYLE.

- Sales are driven by rising diabetes prevalence, product affordability, and distribution strategies.

- Market share remains competitive amid rising CGM adoption but retains a substantial OTC segment.

- Revenue projections indicate steady growth, with potential for substantial expansion if innovation and market access continue.

- Navigating regulatory environments in different regions remains essential for international growth.

FAQs

1. How does FREESTYLE compare in price to CGM devices?

FREESTYLE devices typically retail at around $15 per unit, whereas CGMs can cost $70–$100 per month, making FREESTYLE more accessible for cost-sensitive consumers.

2. What is the primary demographic target for FREESTYLE?

Adults and adolescents with diabetes who prefer simple, affordable, and portable monitoring solutions.

3. What is the main competitive advantage of FREESTYLE?

Ease of use and lower cost compared to more complex CGM systems.

4. Which regions offer the greatest growth opportunities?

Emerging markets in Asia, Latin America, and Africa, driven by increasing diabetes prevalence and expanding healthcare access.

5. How might regulatory changes impact FREESTYLE?

Approvals in new markets can facilitate expansion, while stricter regulations could slow distribution unless products meet local standards.

References

[1] MarketWatch, "Global Glucose Monitoring Market Size", 2022.

[2] International Diabetes Federation, "IDF Diabetes Atlas", 2021.

[3] IQVIA, "Market Share Data for Glucometers", 2022.

[4] Abbott Laboratories, "Annual Report 2022".

[5] Retail Price Sources, "Average Gadget Cost", 2023.