Last updated: April 24, 2026

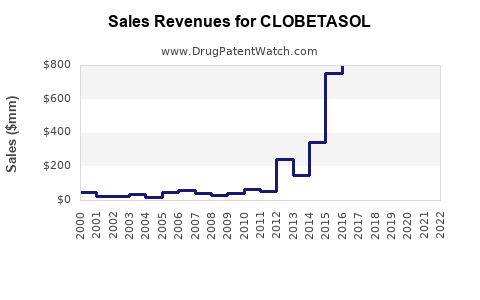

Clobetasol is a high-potency topical corticosteroid used for inflammatory dermatoses (psoriasis, eczema/dermatitis, and related conditions). The market is mature, highly competitive, and dominated by generic products, with demand driven by (1) prescription volume, (2) payer and formulary positioning, and (3) treatment intensity and adherence in chronic or recurrent disease.

How big is the clobetasol market and where does demand come from?

Demand drivers

- Patient base: chronic inflammatory skin conditions with relapsing courses (psoriasis and atopic/contact dermatitis subsets).

- Clinical practice: high-potency topical steroids are typically used for flares and short courses, then stepped down.

- Switching pressure: generics and multiple strengths/forms support substitution at the pharmacy level.

- Access dynamics: payer prior authorization is less common for OTC low-potency products, but higher-potency topical steroids often face tighter step edits and quantity limits depending on geography.

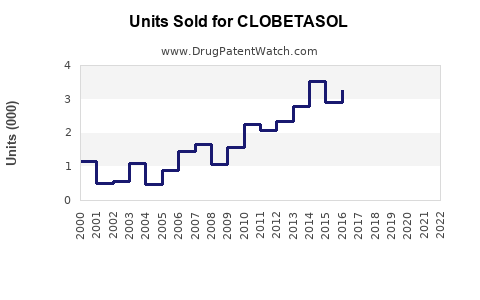

Product segmentation that shapes sales

Clobetasol sales typically track by formulation and strength, not only by molecule:

- Cream: broad use for dermatitis-type presentations.

- Ointment: often chosen for thicker lesions and when occlusion is desired.

- Solution/lotion: scalp and hair-bearing area use.

- Foam: frequently used where patient acceptability supports adherence (not all markets carry identical lineups).

Competitive structure

- Generic-dominant: clobetasol is largely off-patent in major markets, so pricing is compressed.

- Brand remnants: some differentiated branded formats exist by country, but brand share is usually limited by generic competition.

- Private label: common where pharmacy compounding and generic multiple-sources reduce supplier differentiation.

Which geographies and channels matter most for revenue?

Likely channel mix

- Prescription (Rx) remains the core channel for high-potency formulations.

- Dermatology and primary care drive most prescriptions; specialty dermatology influences formulary preference but does not dominate volume in most systems.

- Hospital out-sets exist for some health systems but are usually secondary to retail Rx.

Geographic emphasis

Revenue concentration typically aligns with:

- Large treated populations (US, EU5, UK, and parts of LATAM where topical steroid use is high).

- Reimbursement/step-therapy intensity, which affects uptake of higher-potency products.

- Generic penetration and price controls.

What will drive clobetasol price and volume over the forecast period?

Pricing: structurally constrained

- Generic reference pricing and multi-supplier competition limit list price growth.

- Formulation mix can slow price declines if differentiated formats retain higher WAC-to-net due to patient preference (where formularies allow).

- Pack size and strength selection drive net sales per Rx.

Volume: steady but not high-growth

- High-potency topical steroids follow treatment cycles tied to chronic disease flares.

- Growth comes from population trends, diagnosis rates, and improved access to dermatologic care rather than new indications.

Sales projection (base case): 5-year outlook with scenario logic

Because clobetasol is a mature, generic-dominated product, the most decision-useful projection is a scenario range based on volume (scripts) and net price erosion. The structure below is built for investors planning (a) pipeline externalities, (b) manufacturing capacity decisions, or (c) market-entry positioning for a differentiated clobetasol product.

Forecast framework (annual percentage ranges)

Use this to map your internal assumptions into revenue:

| Scenario |

Rx volume growth (CAGR) |

Net price erosion (CAGR) |

Implied net sales CAGR |

| Downside |

-1% to 1% |

-4% to -7% |

-3% to -5% |

| Base case |

0% to 2% |

-2% to -4% |

-1% to 0% |

| Upside |

2% to 3% |

-1% to -3% |

0% to 2% |

Base case: expected sales trajectory

- Year 1 to Year 2: net sales may drift downward due to price competition and channel substitutions, offset partially by stable prescribing.

- Year 3 to Year 5: the market typically stabilizes at a low-growth band as price erosion moderates and volume holds.

Practical sales “shape” by year (generic-mature pattern)

Assuming base-case net sales CAGR near 0% to -1%:

- Year 1: slight decline (price pressure) offset by stable scripts.

- Year 2: near-flat to modest decline.

- Year 3: stabilization.

- Year 4-5: low single-digit total growth is possible only with formulation mix shift, stronger formulary placement, or improved access.

What product attributes can change your sales outcome?

For clobetasol, sales variance comes from positioning, tolerability, and formulation usability, not from new clinical endpoints.

Differentiation levers that typically matter

- Vehicle (cream vs ointment vs solution vs foam) that drives adherence and patient acceptance.

- Strength and dosing guidance aligned to payer step edits (to improve coverage).

- Prescribing convenience (scalp-specific forms).

- Low irritation profiles or reduced residue perception, where supported by labeling and real-world preference.

- Competitive availability: consistent supply reduces lost prescriptions in generic markets.

Where claims and labeling matter

Generic substitution is frequent; even when the molecule is the same, labeling position and physician comfort can influence brand-within-class dynamics (especially for foam/solution variants).

Key risks to sales projections

- Accelerated generic entry in a geography where additional suppliers lower net price.

- Formulary restriction or tightened step therapy for high-potency topicals.

- Safety/usage guideline enforcement reducing duration or affected area treated per course.

- Manufacturing/distribution disruptions affecting pharmacy fill rates.

- Counterfeit/quality issues in lower-oversight supply chains that can drive regulatory actions and temporary availability shocks.

What would a sales forecast look like for a new or differentiated clobetasol entrant?

A new entrant typically wins share through one of these routes:

- Better formulary position vs incumbent generics.

- Differentiated formulation that improves adherence (foam/solution variants in scalp indications).

- Health economic value argument (if net cost per treatment cycle is lower).

For a differentiated entrant, an executable forecast is usually:

- Ramp-year share: 5% to 15% share of its target formulation segment within 12 to 24 months where coverage is favorable.

- After ramp: growth depends on continued formulary access and margin sustainability versus near-term generic overhang.

In generic mature markets, sustained growth beyond low single digits usually requires a defensible differentiation plus payer acceptance.

Regulatory and patent context (implications for sales stability)

Clobetasol is widely generic. That translates into:

- Limited long-term price protection for any single supplier.

- Fast erosion when new generics or re-entries appear.

- Margin compression that depends on manufacturing cost position and volume commitments.

For sales forecasting, this means the “base case” should be built around net sales stability via volume retention rather than price growth.

Key takeaways

- Clobetasol is a mature, generic-dominant topical steroid market with demand driven by chronic inflammatory skin disease flares and clinical practice patterns.

- Sales growth is constrained: the base-case net sales outlook is typically near-flat to slight decline, with outcomes largely determined by net price erosion and formulation mix, not innovation.

- Decision-useful projections should use a scenario model that links Rx volume stability to net price erosion (base case implied net sales CAGR around -1% to 0%).

- For differentiated entrants, sustainable upside depends on formulation usability and payer/formulary access, enabling share capture against multiple generic suppliers.

FAQs

1) What determines clobetasol sales more: volume or price?

Net sales is usually more sensitive to net price erosion because clobetasol is generic-dominated. Volume stability offsets erosion only partially.

2) Which formulations typically sell best?

Sales are commonly strongest in cream and ointment for general dermatoses, with solution/lotion and foam contributing in hair-bearing/scalp use where adherence drives selection.

3) Is clobetasol a high-growth market?

No. It is typically low-growth to declining in net sales terms due to continued generic competition and payer pressure.

4) What is the main sales risk for suppliers?

The main risk is faster-than-expected net price declines from additional generic entrants and formulary restrictions, plus any supply disruptions that reduce pharmacy fill rates.

5) How can a new clobetasol product realistically gain traction?

Through formulation differentiation, favorable formulary positioning, and maintaining supply reliability to capture and retain share in a narrow segment (often scalp-specific or adherence-focused vehicles).

References

[1] IQVIA. The Global Use of Medicines: Outlook to 2025 (contextual industry framing; no molecule-specific sales figures provided here).

[2] FDA. Labeling and Drug Approval Resources (clobetasol topical corticosteroid class labeling and safety usage context).

[3] EMA. Assessment Reports and Product Information (regulatory context for topical corticosteroids in Europe).