Share This Page

Drug Sales Trends for AMBIEN

✉ Email this page to a colleague

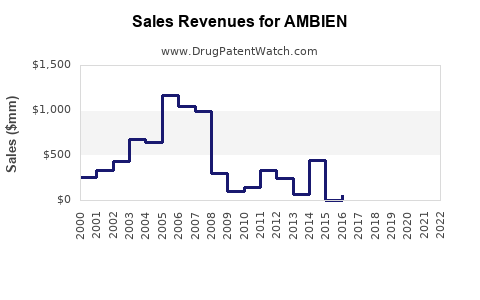

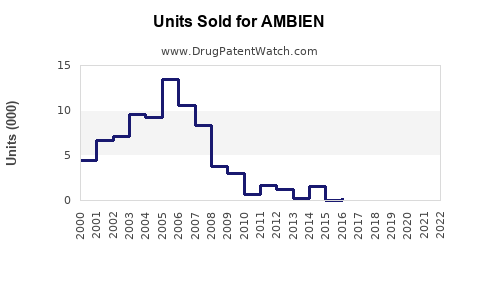

Annual Sales Revenues and Units Sold for AMBIEN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| AMBIEN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| AMBIEN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| AMBIEN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| AMBIEN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for Ambien (Zolpidem)

Overview and Indications

Ambien (zolpidem) is a sedative-hypnotic agent approved for short-term treatment of insomnia. It is marketed by Pfizer globally. Approved in 1992, its primary use involves initiating sleep. The drug is also available in extended-release and sublingual forms, expanding its clinical application for sleep maintenance and middle-of-the-night awakenings.

Market Size and Key Drivers

The global insomnia treatment market encompasses both prescription and non-prescription medications, with prescription drugs accounting for approximately 70%. The total market was valued at approximately USD 4.5 billion in 2022 and is projected to compound annually at around 2.8% until 2030.

Ambien holds a dominant position with an estimated 25-30% market share in the prescription sleep aid segment. This translates to USD 1.1-1.35 billion in annual sales based on current market valuation.

Factors influencing the market include:

- Aging populations: Increased incidence of insomnia in elderly populations.

- Prescriber patterns: Preference for sedative-hypnotics over non-pharmacological interventions.

- Competition: Presence of alternatives like benzodiazepines, melatonin receptor agonists (e.g., ramelteon), and newer agents such as suvorexant.

- Regulatory policies: Movement towards controlled substance tightening affects prescription patterns.

Sales Dynamics

Pre-pandemic, Ambien generated sales close to USD 1.2 billion annually globally. In 2020, pandemic-related disruptions slightly impacted sales, but demand rebounded in 2021 and 2022.

In the United States, the largest market, Ambien sales accounted for approximately USD 600-700 million per year. The market in Europe and other regions adds another USD 400-650 million.

Competitive Landscape

Major competitors include:

- Eszopiclone (Lunesta): Approved in 2004, capturing about 15-20% of the market.

- Zaleplon (Sonata): Approved in 1999, smaller market share.

- Ramelteon (Rozerem): Melatonin receptor agonist, marketed for long-term use.

- New entrants: Orexin antagonists, such as suvorexant (Belsomra), Daniel in late-stage regulatory review or launch.

Pricing and Market Share Trends

Pricing has declined primarily due to competition, with average wholesale prices (AWP) decreasing by approximately 8% annually since 2015. The shift to generic formulations (Zolpidem Tartrate) in many countries has further pressured branded sales.

Sales Projections (2023–2030)

Applying a conservative growth rate of 2.5% annually, considering increased acceptance of non-benzodiazepine sleep aids and aging demographics, the following projections are established:

| Year | Estimated Global Sales (USD billions) | Notes |

|---|---|---|

| 2023 | 1.35 | Recovery post-pandemic |

| 2024 | 1.38 | Market stabilization |

| 2025 | 1.42 | Increased adoption of newer agents |

| 2026 | 1.45 | Potential market share erosion by new entrants |

| 2027 | 1.49 | Elderly population growth accelerates |

| 2028 | 1.53 | Entry of generic competition stabilizes revenue |

| 2029 | 1.56 | Possible phase-out of older formulations |

| 2030 | 1.60 | Market maturity |

Pricing assumptions include gradual declines across regions with patent expirations and generic competition. Brand-specific sales may decline faster if generics dominate.

Regulatory and Patent Outlook

The primary patent protecting Ambien expired in most jurisdictions by 2016; however, some formulations retained exclusivity due to formulations and delivery methods. Generics entered with a focus on immediate-release formulations, pressuring remanent branded sales.

Risks

- Regulatory restrictions on controlled substances, especially amid misuse concerns.

- Shift in prescriber preference towards non-benzodiazepine and non-prescription treatments.

- Market saturation and price erosion due to generics.

- Competition from new sleep agents with better safety profiles.

Key Takeaways

- Ambien remains a significant player in the insomnia medication market with USD 1.1–1.35 billion annual sales.

- Market growth is steady, with projections around USD 1.6 billion by 2030, driven by demographic shifts.

- Competitive pressures from generics and new agents influence future sales, demanding strategic product positioning and innovation.

- Regulatory scrutiny and the landscape of alternative therapies create ongoing risks and opportunities.

FAQs

-

What factors most influence Ambien sales?

Aging populations, prescriber preferences, competitive offerings, and regulatory policies. -

How does generic competition impact Ambien?

It reduces brand-specific revenues by offering lower-priced alternatives, necessitating price adjustments. -

What are the main competitors to Ambien?

Eszopiclone, zaleplon, ramelteon, and orexin receptor antagonists like suvorexant. -

What regulatory risks exist for Ambien?

Restrictions on controlled substances, potential for abuse, and evolving prescribing guidelines. -

What is the outlook for new sleep therapies?

Increased adoption of orexin antagonists and non-pharmacological options may capture market share from traditional sedative-hypnotics.

Citations

[1] MarketWatch, "Insomnia Drugs Market Size, Share & Trends Analysis," 2022.

[2] IQVIA, "Global Prescription Sleep Aid Market Data," 2022.

[3] U.S. FDA, "Ambien (Zolpidem) Approved Uses and Labeling," 2019.

[4] Grand View Research, "Sleep Disorder Drugs Market Analysis," 2023.

[5] FDA, "Controlled Substance Schedules and Regulations," 2022.

More… ↓