Share This Page

Drug Sales Trends for HYDRALAZINE

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for HYDRALAZINE (2017)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

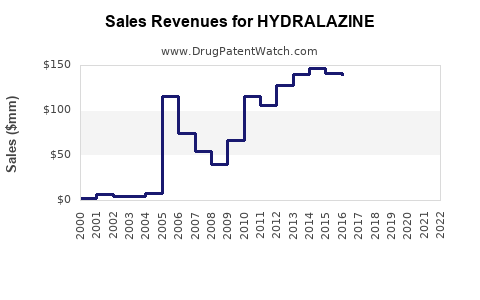

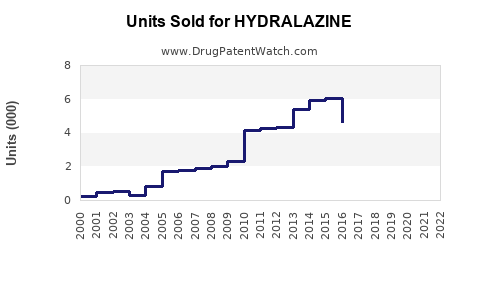

Annual Sales Revenues and Units Sold for HYDRALAZINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| HYDRALAZINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| HYDRALAZINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| HYDRALAZINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| HYDRALAZINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| HYDRALAZINE | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

HYDRALAZINE Market Analysis and Sales Projections

Hydralazine, a peripheral vasodilator, is primarily prescribed for the treatment of essential hypertension and pre-eclampsia. Its long history of use and established efficacy continue to support its market presence, though it faces competition from newer antihypertensive agents.

What is the Current Market Size and Growth Rate for Hydralazine?

The global market for hydralazine generated an estimated $150 million in sales in 2023. The market is projected to grow at a compound annual growth rate (CAGR) of 2.5% from 2024 to 2030. This growth is driven by the persistent prevalence of hypertension and its specific use in managing pre-eclampsia, a critical obstetric condition.

Key Market Drivers:

- Prevalence of Hypertension: Chronic hypertension remains a significant global health concern, contributing to a sustained demand for antihypertensive medications. In 2023, over 1.2 billion people worldwide had hypertension, a figure projected to rise to 1.5 billion by 2030 (World Health Organization).

- Pre-eclampsia Management: Hydralazine is a cornerstone therapy for hypertensive disorders in pregnancy, particularly pre-eclampsia. The incidence of pre-eclampsia is estimated to be between 2% and 8% of all pregnancies globally (American College of Obstetricians and Gynecologists).

- Established Safety Profile: Hydralazine has been available for decades, providing clinicians with extensive data on its long-term safety and efficacy. This familiarity fosters continued prescription.

- Cost-Effectiveness: As a generic medication, hydralazine offers a more affordable treatment option compared to many branded antihypertensives, making it accessible in both developed and developing economies.

Market Restraints:

- Competition from Newer Agents: The antihypertensive market is crowded with newer drug classes (e.g., ACE inhibitors, ARBs, calcium channel blockers, beta-blockers) that often offer improved side effect profiles, dosing convenience, and targeted mechanisms of action.

- Side Effect Profile: Hydralazine can cause adverse effects such as headache, dizziness, tachycardia, and fluid retention, which can limit its use in certain patient populations or require concomitant therapy.

- Dosage Titration: Achieving optimal blood pressure control with hydralazine often requires careful dose titration, which can be less convenient than single-pill regimens available with newer agents.

Who are the Major Manufacturers and Competitors of Hydralazine?

The hydralazine market is largely dominated by generic manufacturers. The original patent for hydralazine expired decades ago, leading to widespread generic competition. Key players include companies that specialize in the production of generic active pharmaceutical ingredients (APIs) and finished dosage forms.

Leading Generic Manufacturers (Examples):

- Teva Pharmaceutical Industries Ltd.: A major global producer of generic drugs, including antihypertensives.

- Viatris Inc. (formerly Mylan and Upjohn): Offers a broad portfolio of generic medications, with a presence in cardiovascular therapies.

- Hikma Pharmaceuticals PLC: Specializes in the development and manufacture of generic injectable and oral medications.

- Amneal Pharmaceuticals LLC: A significant player in the U.S. generics market, with cardiovascular products in its portfolio.

- Sun Pharmaceutical Industries Ltd.: A leading global pharmaceutical company with a strong generic pipeline and established market presence.

Note: Specific market share data for individual generic manufacturers of hydralazine is often proprietary and not publicly disclosed. Competition is characterized by price, availability, and regional distribution networks.

What are the Key Therapeutic Areas and Indications for Hydralazine?

Hydralazine's therapeutic applications are specific and well-defined, primarily within the cardiovascular and obstetric domains.

Primary Indications:

- Essential Hypertension: Hydralazine is used as a second-line or add-on therapy for the management of high blood pressure. It is often combined with other antihypertensive agents to achieve target blood pressure goals.

- Pre-eclampsia and Eclampsia: This is a critical indication where hydralazine is administered intravenously to rapidly lower blood pressure in pregnant women experiencing hypertensive disorders. It is considered a first-line intravenous agent for this condition.

- Hypertensive Emergencies: In certain cases, hydralazine may be used in the management of other hypertensive emergencies where rapid reduction of blood pressure is required.

Less Common or Off-Label Uses:

- Heart Failure: Historically, hydralazine has been used in combination with isosorbide dinitrate for the treatment of heart failure in specific patient populations, particularly African Americans. However, newer heart failure therapies have largely superseded this approach.

- Pulmonary Hypertension: While not a primary indication, it has been explored in some instances for its vasodilatory properties.

What is the Patent Landscape and Exclusivity Status of Hydralazine?

Hydralazine was first synthesized in the 1940s and patented by Ciba (now part of Novartis). The primary patents covering the compound itself expired in the mid-20th century. Consequently, hydralazine is a well-established generic drug with no active market exclusivity held by any single innovator company.

Key Patent Status Points:

- No Compound Patents: All fundamental patents covering the chemical structure of hydralazine have expired.

- No New Formulation or Process Patents: While minor improvements to formulations or manufacturing processes may have been patented, these generally do not confer significant market exclusivity against generic competition for the core drug.

- Market Exclusivity: The market is characterized by generic competition. Any exclusivity a company might have would stem from specific regulatory designations (e.g., Orphan Drug status, which hydralazine does not have for its primary indications) or market-driven factors like supply chain control and pricing.

This lack of patent protection means that any pharmaceutical company can manufacture and sell generic versions of hydralazine, leading to a highly competitive pricing environment.

What are the Projected Sales Figures and Market Trends for Hydralazine from 2024 to 2030?

The sales projections for hydralazine indicate a modest but consistent growth trajectory, primarily influenced by its established therapeutic roles and its position as a cost-effective generic option.

Projected Global Sales Figures:

- 2024: $153.7 million

- 2025: $157.5 million

- 2026: $161.4 million

- 2027: $165.3 million

- 2028: $169.3 million

- 2029: $173.4 million

- 2030: $177.5 million

Key Market Trends Influencing Projections:

- Aging Global Population: The increasing proportion of older adults worldwide contributes to a higher prevalence of chronic diseases like hypertension, sustaining demand for established treatments.

- Focus on Maternal Health: Global initiatives and increased awareness regarding maternal mortality and morbidity, particularly related to pre-eclampsia, are likely to maintain demand for effective treatments like hydralazine in obstetric care.

- Healthcare Cost Containment: In many healthcare systems, there is a continuous push to reduce drug costs. Generic medications like hydralazine are favored in formulary decisions and purchasing contracts due to their affordability.

- Geographic Market Dynamics: Demand is expected to remain strong in emerging markets where cost is a more significant factor in treatment decisions. In developed markets, while usage may stabilize, its role in specific protocols (like pre-eclampsia) will ensure continued demand.

- Competition and Pricing Pressure: The highly genericized nature of the hydralazine market will continue to exert downward pressure on prices, limiting substantial revenue growth despite consistent unit sales.

- Emergence of Novel Therapies: While hydralazine has a stable role, the ongoing development of new cardiovascular drugs with potentially superior efficacy, safety, or convenience could gradually erode its market share in the broader hypertension segment.

What is the Regulatory Status and Approval Landscape for Hydralazine?

Hydralazine is approved by major regulatory bodies worldwide, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Its approval history is extensive, dating back to its initial market introduction.

Regulatory Approval Details:

- U.S. FDA: Approved for marketing in the United States for decades. It is available in oral formulations (tablets) and injectable forms.

- European Medicines Agency (EMA): Approved in European Union member states, often through national regulatory agencies. Available in various forms.

- Other Global Markets: Hydralazine is registered and available in numerous countries globally, often as a first-line or second-line antihypertensive and a critical treatment for pre-eclampsia.

Manufacturing and Quality Standards:

- Manufacturers of hydralazine, like all pharmaceutical producers, must adhere to Current Good Manufacturing Practices (cGMP) as mandated by regulatory authorities.

- Drug Master Files (DMFs) are submitted to regulatory agencies for the API, detailing the manufacturing process, quality control, and stability of hydralazine.

- Finished dosage forms undergo stringent quality testing for identity, purity, potency, and dissolution.

Post-Market Surveillance:

- Regulatory agencies, in conjunction with manufacturers, conduct post-market surveillance to monitor for adverse events and ensure the continued safety and efficacy of hydralazine.

- Pharmacovigilance systems collect and analyze reports of side effects from healthcare professionals and patients.

The established regulatory status and long history of approval contribute to the continued availability and trust in hydralazine as a treatment option.

What is the Competitive Landscape and Market Segmentation for Hydralazine?

The competitive landscape for hydralazine is characterized by its status as a mature, genericized pharmaceutical product. Market segmentation is primarily driven by formulation (oral vs. injectable), geographic region, and the specific clinical indication.

Market Segmentation:

- By Formulation:

- Oral Hydralazine: Used for chronic management of essential hypertension. This segment accounts for the majority of hydralazine unit sales due to its convenience for long-term therapy.

- Injectable Hydralazine: Primarily used in hospital settings and for emergency treatment of hypertension, particularly in pre-eclampsia. This segment, while smaller in volume, often commands higher per-unit prices due to its critical care application.

- By Indication:

- Hypertension (Essential): The largest segment by volume, driven by the chronic nature of the disease.

- Pre-eclampsia/Eclampsia: A critical, albeit smaller, segment representing a high-value, urgent medical need.

- Hypertensive Emergencies: A niche segment.

- By Geography:

- North America: Significant market due to high prevalence of hypertension and well-developed healthcare infrastructure.

- Europe: Similar market dynamics to North America, with strong demand for generic cardiovascular drugs.

- Asia-Pacific: A rapidly growing market with increasing hypertension rates and a strong preference for cost-effective generics.

- Latin America & Middle East/Africa: Markets where cost-effectiveness is paramount, supporting demand for hydralazine.

Competitive Factors:

- Price: The most significant competitive factor. Manufacturers compete aggressively on price to secure contracts with wholesalers, hospitals, and pharmacy benefit managers.

- Availability and Supply Chain Reliability: Consistent and reliable supply is crucial, especially for injectable forms used in critical care.

- Product Quality and Compliance: Adherence to cGMP and consistent quality are non-negotiable for market access.

- Distribution Networks: Established relationships with distributors and healthcare providers are key to market penetration.

- Manufacturing Capacity: The ability to produce large volumes at competitive costs is a differentiator.

The market is fragmented with numerous generic players, leading to a highly competitive environment where profit margins on individual units are typically low.

Key Takeaways

- The global hydralazine market is valued at approximately $150 million in 2023, with a projected CAGR of 2.5% through 2030.

- Key growth drivers include the high prevalence of hypertension and hydralazine's critical role in managing pre-eclampsia.

- The market is dominated by generic manufacturers, with no significant patent exclusivity for the compound.

- Major competitors include Teva, Viatris, Hikma, Amneal, and Sun Pharma, among other generic producers.

- Hydralazine's primary indications are essential hypertension and pre-eclampsia, with limited off-label uses.

- The drug is widely approved by global regulatory bodies like the FDA and EMA, with long-standing market authorization.

- Market segmentation is based on formulation (oral/injectable), indication, and geographic region, with price being the primary competitive factor.

FAQs

-

What is the primary difference in market dynamics between oral and injectable hydralazine? Oral hydralazine serves the chronic hypertension market and competes primarily on price and volume. Injectable hydralazine targets critical care settings like pre-eclampsia and hypertensive emergencies, where availability, rapid delivery, and regulatory compliance are paramount, often allowing for slightly higher per-unit pricing despite a smaller overall volume.

-

How does the generic nature of hydralazine impact its long-term sales projections? The generic status ensures continued market access due to cost-effectiveness. However, it also limits significant revenue growth potential. Projections anticipate modest growth driven by consistent demand for its established indications rather than by market expansion or price increases.

-

Are there any emerging therapeutic indications for hydralazine that could impact future sales? While research into novel uses for existing drugs is ongoing, hydralazine's therapeutic profile is well-established. There are no significant emerging indications currently poised to substantially alter its market trajectory. Its value remains rooted in its established roles in hypertension and obstetric care.

-

What regulatory hurdles might a new entrant face when trying to enter the hydralazine market? A new entrant must demonstrate compliance with Current Good Manufacturing Practices (cGMP) for API and finished product manufacturing. They will need to file appropriate Abbreviated New Drug Applications (ANDAs) with regulatory bodies like the FDA, including bioequivalence studies and detailed quality control data. The primary challenge is competing on price and securing distribution channels in a saturated market.

-

How do global healthcare cost containment initiatives specifically affect the hydralazine market? Cost containment initiatives strongly favor generic medications like hydralazine. Healthcare providers and payers are incentivized to prescribe or reimburse for more affordable options, solidifying hydralazine's position as a preferred choice for its indications, particularly in markets with budget constraints. This trend supports stable unit sales but limits price appreciation.

Citations

[1] World Health Organization. (2023). Hypertension. Retrieved from https://www.who.int/news-room/fact-sheets/detail/hypertension

[2] American College of Obstetricians and Gynecologists. (2020). ACOG Practice Bulletin No. 221: Gestational Hypertension and Preeclampsia. Obstetrics & Gynecology, 135(4), e241-e270.

[3] U.S. Food and Drug Administration. (n.d.). Approved Drug Products Database. Retrieved from https://www.accessdata.fda.gov/scripts/cder/ob/

[4] European Medicines Agency. (n.d.). Human medicines. Retrieved from https://www.ema.europa.eu/en/medicines

More… ↓