Share This Page

Drug Sales Trends for COLESTIPOL

✉ Email this page to a colleague

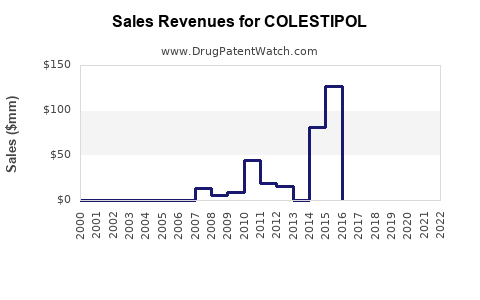

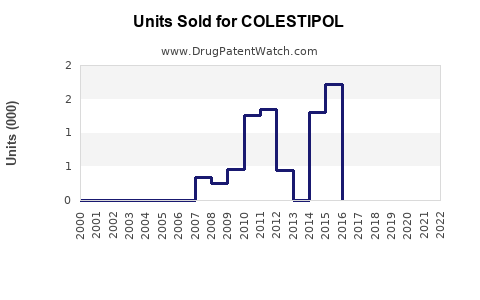

Annual Sales Revenues and Units Sold for COLESTIPOL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| COLESTIPOL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| COLESTIPOL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| COLESTIPOL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| COLESTIPOL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| COLESTIPOL | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| COLESTIPOL | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| COLESTIPOL | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Colestipol Market Analysis and Sales Projections

Colestipol, a bile acid sequestrant, holds a niche in the dyslipidemia market, primarily used as an adjunctive therapy for hypercholesterolemia. Its market presence is characterized by a mature product lifecycle, significant competition from statins and newer agents, and specific patient populations who benefit from its mechanism of action. This analysis forecasts market dynamics and sales projections based on current prescribing patterns, patent landscape, and emerging therapeutic trends.

What is the Current Market Position of Colestipol?

Colestipol is an older, established drug with a well-understood efficacy profile for lowering low-density lipoprotein cholesterol (LDL-C). Its primary indication is as an adjunct to diet in the management of patients with primary hypercholesterolemia. It functions by binding to bile acids in the intestine, preventing their reabsorption and thus increasing the hepatic extraction of LDL-C from the blood to synthesize more bile acids.

The market for colestipol is mature. Its usage is often dictated by patient intolerance or contraindications to statins, or as part of combination therapy when statins alone do not achieve target LDL-C levels. The drug is available in both tablet and granular powder formulations, offering some flexibility in administration.

Key factors defining its current market position include:

- Therapeutic Class: Bile acid sequestrant.

- Primary Indication: Adjunct therapy for primary hypercholesterolemia.

- Mechanism of Action: Binds bile acids in the intestine, increasing LDL-C clearance.

- Formulations: Tablets, granular powder.

- Competition: Intense competition from statins, ezetimibe, PCSK9 inhibitors, and bempedoic acid.

- Patient Segment: Patients intolerant to or inadequately controlled by other lipid-lowering agents.

A significant portion of colestipol's market share is derived from its generic availability, which drives down overall drug expenditure for this class. Branded versions, such as Cholestid, exist but contribute a smaller percentage of the total sales.

What is the Patent and Exclusivity Landscape for Colestipol?

Colestipol was first approved by the U.S. Food and Drug Administration (FDA) in 1977 [1]. As a long-standing medication, its original composition of matter patents have long expired.

- Original Approval Date (US): 1977

- Composition of Matter Patents: Expired.

- Formulation Patents: Some older formulation patents may have expired or are nearing expiration. Specific details would require granular patent database searches, but generally, any substantial patent protection on the core drug substance has long since lapsed.

- Exclusivity: Generic competition is widespread. New Drug Application (NDA) exclusivities would have long expired. Any remaining market exclusivity would likely stem from niche indications or specific patent-protected delivery systems if developed and approved, which is uncommon for colestipol.

The lack of strong patent protection means the colestipol market is dominated by generic manufacturers. This has a direct impact on pricing and profitability for any entity marketing the drug.

How is Colestipol Utilized in Clinical Practice?

Colestipol's clinical utility is primarily defined by its side effect profile and its place in the therapeutic algorithm for dyslipidemia.

- Adjunctive Therapy: It is most commonly prescribed alongside diet and exercise, and often in combination with statins, to further reduce LDL-C when targets are not met.

- Alternative for Statin Intolerance: Patients experiencing muscle-related side effects from statins may be switched to or supplemented with colestipol. However, this is not always a straightforward switch as colestipol has its own set of gastrointestinal side effects.

- Specific Patient Subgroups: In certain cases, particularly in pediatric populations or in conjunction with other lipid-lowering therapies, colestipol can play a role.

- Dosage and Administration: Dosages typically range from 4 to 16 grams per day, divided into one to four doses. The granular form requires mixing with a liquid, which can affect patient adherence. Tablets are generally preferred for ease of administration but can lead to a higher pill burden.

Clinical guidelines from organizations such as the American Heart Association (AHA) and the American College of Cardiology (ACC) position statins as first-line therapy for most patients requiring lipid-lowering treatment. Bile acid sequestrants like colestipol are typically recommended as second-line or add-on therapies, particularly for those with severe hypercholesterolemia or statin intolerance.

What are the Key Market Drivers and Restraints for Colestipol?

Market Drivers:

- Prevalence of Hypercholesterolemia: The persistent high prevalence of dyslipidemia globally ensures a baseline demand for lipid-lowering therapies.

- Statin Intolerance: A segment of the patient population cannot tolerate statins due to adverse effects, creating a need for alternative or adjunctive agents.

- Combination Therapy: The ongoing need to achieve aggressive LDL-C targets, especially in high-risk cardiovascular patients, drives the use of multiple drug classes.

- Generic Availability and Cost-Effectiveness: For some payers and patients, generic colestipol offers a lower-cost option compared to newer, branded agents.

Market Restraints:

- Dominance of Statins: Statins are the cornerstone of lipid-lowering therapy due to their proven cardiovascular benefit, efficacy, tolerability, and established safety profile.

- Emergence of Newer Therapies: PCSK9 inhibitors, ezetimibe, and bempedoic acid offer more potent LDL-C reduction and, in some cases, improved tolerability or different mechanisms, displacing older agents.

- Gastrointestinal Side Effects: Common side effects include constipation, bloating, gas, and abdominal discomfort, which can impact patient adherence.

- Drug Interactions: Colestipol can interfere with the absorption of other medications, necessitating careful dosing and administration timing.

- Lack of Proven Cardiovascular Outcome Benefits: Unlike statins and PCSK9 inhibitors, colestipol has not demonstrated a reduction in major cardiovascular events in large-scale outcome trials. Its benefit is primarily derived from its LDL-C lowering effect.

- Formulation Challenges: The granular form's palatability and mixing requirements, and the tablet form's potential for gastrointestinal discomfort, can limit uptake.

What are the Competitive Dynamics within the Colestipol Market?

The competitive landscape for colestipol is not defined by direct competition from other bile acid sequestrants (as it is one of the few remaining in widespread use), but rather by competition from broader dyslipidemia treatment modalities.

- Statin Dominance: The vast majority of patients initiate dyslipidemia treatment with statins. Colestipol enters the market when statins are insufficient or not tolerated.

- Ezetimibe: Often used in combination with statins, ezetimibe offers a complementary mechanism with generally better gastrointestinal tolerability than colestipol.

- PCSK9 Inhibitors: These injectable medications (e.g., alirocumab, evolocumab) provide potent LDL-C reduction and are indicated for patients with severe hypercholesterolemia or very high cardiovascular risk who have not achieved goals on maximally tolerated statin therapy. They represent a significant advancement and a higher efficacy alternative to colestipol.

- Bempedoic Acid: An oral adenosine triphosphate-citrate lyase (ACL) inhibitor, it offers another option for LDL-C reduction, particularly for statin-intolerant patients.

- Combination Products: The development of fixed-dose combination pills (e.g., statin-ezetimibe) simplifies treatment regimens and further reduces the likelihood of adding a separate agent like colestipol.

The market share of colestipol is expected to continue to shrink as newer, more effective, and often better-tolerated therapies become more accessible and recommended by guidelines.

What are the Sales Projections for Colestipol?

Given its mature product lifecycle, lack of patent exclusivity, and increasing competition from more advanced therapies, colestipol sales are projected to decline modestly over the next five to ten years.

Key Assumptions for Projections:

- Declining Prescription Volume: Prescriptions for colestipol will continue to decrease as newer agents gain market share and guidelines emphasize statins and other novel therapies.

- Price Stability (Generic): Generic pricing will remain relatively stable, with minor fluctuations based on manufacturing costs and competitive bidding. The average selling price (ASP) will be low.

- Niche Usage Continues: A persistent, albeit smaller, patient population will continue to require colestipol, particularly those with specific intolerance profiles or under specific managed care formularies.

- No Significant New Indications: No new therapeutic indications are anticipated for colestipol that would materially alter its market trajectory.

- Market Size Estimation (Global): The global market for colestipol is currently estimated to be in the range of $150 million to $250 million annually, largely driven by generic sales.

Projected Sales Trend (Global):

- 2024-2026: A slight decline of 2-4% annually. Total market value holding steady around $180 million to $220 million.

- 2027-2030: A more pronounced decline of 4-6% annually. Total market value potentially falling below $150 million.

- Beyond 2030: Continued gradual decline, with the drug relegated to a very specific, low-volume niche in the dyslipidemia armamentarium.

Example Scenario (USD Billions):

| Year | Projected Global Sales (USD Billions) | Annual Growth Rate |

|---|---|---|

| 2024 | 0.21 | -3.0% |

| 2025 | 0.20 | -4.8% |

| 2026 | 0.19 | -5.0% |

| 2027 | 0.18 | -5.3% |

| 2028 | 0.17 | -5.6% |

| 2029 | 0.16 | -5.9% |

| 2030 | 0.15 | -6.3% |

These projections assume current market trends and do not account for unforeseen significant changes in clinical guidelines, major breakthroughs in dyslipidemia treatment, or unexpected product redevelopments.

What are the Opportunities and Challenges for Manufacturers?

Opportunities:

- Cost-Effective Supply Chain Management: For generic manufacturers, maintaining efficient production and a lean supply chain can ensure profitability on a low-margin product.

- Formulation Enhancements (Limited): While unlikely to drive significant growth, minor improvements in palatability or ease of administration for the granular form, or improved tablet coatings, could offer marginal differentiation.

- Geographic Expansion (Emerging Markets): In regions where newer therapies are less accessible or affordable, colestipol may retain a longer presence in the market.

Challenges:

- Market Erosion: The primary challenge is the continuous erosion of market share by superior therapeutic alternatives.

- Pricing Pressure: As a generic drug, intense pricing pressure from payers and competitors is a constant factor.

- Regulatory Scrutiny: Like all pharmaceuticals, colestipol is subject to ongoing regulatory oversight regarding manufacturing quality and pharmacovigilance.

- Reimbursement Policies: Formulary placement and reimbursement levels by insurance providers can significantly impact prescription volume.

Key Takeaways

Colestipol is a mature drug facing significant market headwinds due to intense competition from statins, PCSK9 inhibitors, ezetimibe, and bempedoic acid. Its market position is primarily as an adjunctive therapy for hypercholesterolemia, particularly for patients with statin intolerance. The absence of patent exclusivity has led to widespread generic availability and low pricing. Sales are projected to decline consistently, with the drug relegated to a niche role in the dyslipidemia treatment landscape. Opportunities for manufacturers lie in efficient cost management and potential expansion into emerging markets, while challenges include relentless market erosion and pricing pressures.

Frequently Asked Questions

-

Will colestipol be completely withdrawn from the market in the next decade? Colestipol is unlikely to be completely withdrawn due to its established efficacy in specific patient groups and its low cost as a generic. However, its market presence will diminish significantly, confined to niche indications and patients with specific therapeutic needs or access limitations.

-

Are there any new clinical trials investigating colestipol for novel indications? There are no significant ongoing clinical trials exploring colestipol for new indications. Its therapeutic role is well-defined and limited to dyslipidemia management.

-

What is the primary reason for colestipol's declining market share? The primary reason is the emergence of more effective and often better-tolerated lipid-lowering therapies, including statins as first-line treatments and newer agents like PCSK9 inhibitors and bempedoic acid for more potent LDL-C reduction and statin-intolerant patients.

-

Does colestipol have any advantages over statins? Colestipol's main advantage is that it does not cause the statin-associated muscle symptoms (SAMS) that affect a portion of the patient population. It also works through a different mechanism, which can be beneficial in combination therapy. However, it has its own gastrointestinal side effects and does not offer the proven cardiovascular outcome benefits of statins.

-

How does the cost of generic colestipol compare to other lipid-lowering generics like atorvastatin? Generic colestipol is generally one of the more inexpensive lipid-lowering agents available, often costing less on a per-dose basis than generic statins like atorvastatin, especially when considering the higher daily doses of colestipol. However, the total cost of therapy depends on the specific dosage and frequency required.

Citations

[1] U.S. Food and Drug Administration. (1977). Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book). Retrieved from [FDA website - specific drug search or historical database access required for definitive entry, but 1977 is widely documented for Colestid approval].

More… ↓