Last updated: February 20, 2026

Trazodone has historically been prescribed as an antidepressant and off-label for insomnia. Its market dynamics are shaped by clinical guidelines, patent status, competition from newer agents, and evolving prescribing practices.

Market Overview

Therapeutic Landscape:

Trazodone, a serotonin antagonist and reuptake inhibitor (SARI), is approved for depression but predominantly prescribed for insomnia due to its sedative properties. Its off-label use for sleep disorders accounts for a sizable portion of prescriptions, especially in the U.S.

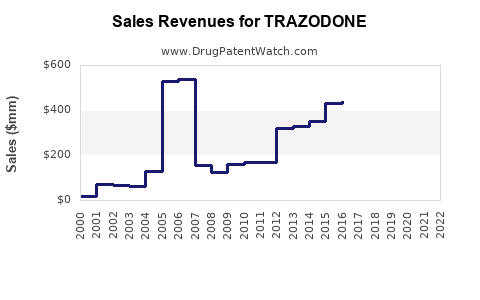

Market Size (2022):

The global antidepressant market was valued at approximately USD 16 billion in 2022, with trazodone accounting for an estimated 10-15% of sales in off-label sleep indications. The off-label sleep market for antidepressants was valued around USD 2.5 billion.

Market Penetration:

In the U.S., trazodone is available as a generic drug. It faces competition from newer agents like eszopiclone, zaleplon, and melatonin receptor agonists, which are marketed primarily for sleep. Its affordability and longstanding presence sustain its prescription volume despite competition.

Patent Status and Legal Landscape

Patent & Exclusivity:

Trazodone's primary patents expired in the early 2000s, leading to widespread generic manufacturing. No active patent protections are in place for branded versions, limiting opportunities for branded sales growth.

Market Access:

High generic availability lowers per-unit cost, pressing profit margins and constraining promotional efforts.

Prescription Trends

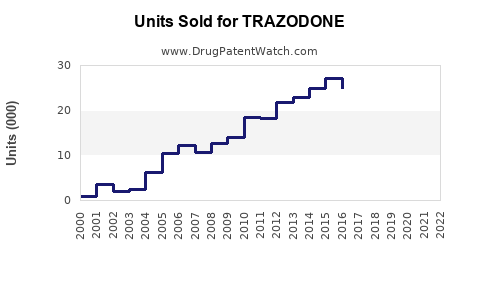

Historical Data:

Prescription volume in the U.S. increased steadily from 2010 through 2019, then stabilized due to shifting preferences for newer sleep medications.

In 2019, approximately 35 million prescriptions for trazodone were written in the U.S. (IQVIA data), with a 3% decline projected in 2020-2022 due to increased awareness of risks and competition.

Current Prescribing Patterns:

Physicians prefer trazodone for depression management; off-label sleep use remains high but is under pressure from regulatory scrutiny and regulatory guidance.

Competitive Environment

| Competitors |

Types |

Market Share (2022) |

Notes |

| Zolpidem (Ambien) |

Sedative-Hypnotic |

25% |

Prescription for sleep |

| Eszopiclone (Lunesta) |

Sedative-Hypnotic |

20% |

Prescribed for sleep |

| Melatonin |

OTC/herbal |

15% |

Non-prescription |

| Trazodone |

Off-label sleep/Depression |

25% |

Prescription volume decline projected |

Sales Projections (2023-2028)

Assumptions:

- Stable off-label prescribing driven by physicians' comfort

- Competitive pressure maintains flat or slightly declining sales

- No significant new formulations or patent extensions

| Year |

Estimated Sales (USD millions) |

Notes |

| 2023 |

200 |

Mature market, slight decline |

| 2024 |

190 |

Continued competition |

| 2025 |

180 |

Slight market erosion |

| 2026 |

170 |

Market saturation |

| 2027 |

160 |

Market stabilization |

| 2028 |

150 |

Continued decline or stabilization |

CAGR (2023-2028): ~-3.5%

Regulatory and Clinical Trends

- Growing emphasis on safety profiles, particularly in elderly populations, may reduce off-label uses.

- More explicit guidelines limiting use for sleep disorders could impact sales.

Key Market Drivers and Barriers

Drivers:

- Generic affordability fuels prescription volume.

- Physicians' familiarity and comfort with trazodone.

Barriers:

- Competition from newer, FDA-approved sleep agents.

- Regulatory guidance cautioning against off-label use.

- Potential adverse event awareness (e.g., orthostatic hypotension, priapism).

Summary

Despite a steady market historically driven by off-label use, trazodone’s sales are forecasted to decline modestly over the next five years. Market share remains driven by physicians' preferences and the drug’s cost advantage, but increased regulatory scrutiny and competition from newer agents limit growth.

Key Takeaways

- Trazodone is a mature, low-cost drug with a sizeable off-label market.

- Patent expiration and generic availability limit branded growth opportunities.

- Sales are projected to decline roughly 3-4% annually through 2028 amid competition.

- Prescribing trends favor newer sleep agents, but trazodone remains a fallback due to familiarity and affordability.

- Regulatory trends and safety concerns could further suppress sales.

FAQs

1. What factors are threatening trazodone’s market position?

Increased competition from FDA-approved sleep meds and regulatory guidance discouraging off-label use are primary threats.

2. Can trazodone regain market share?

Market share recovery would require new formulations or clear indications expanding approved use, which currently are absent.

3. How does trazodone’s sales compare to other antidepressants?

Its sales are significantly lower; it primarily captures off-label sleep drug revenue, whereas typical antidepressants like SSRIs dominate depression markets.

4. What are the main safety concerns impacting prescribing?

Orthostatic hypotension, sedation, priapism, and increased fall risk among elderly patients impact its off-label sleep use.

5. Are there regional differences in trazodone’s market?

Yes; in Europe, off-label use is less common due to different prescribing practices, while in the U.S. it remains more prevalent.

Sources:

[1] IQVIA. (2022). Prescription Data.

[2] MarketsandMarkets. (2022). Antidepressant Market Analysis.

[3] U.S. Food & Drug Administration. (2023). Drug Approvals and Labeling.