Share This Page

Drug Sales Trends for PROTOPIC

✉ Email this page to a colleague

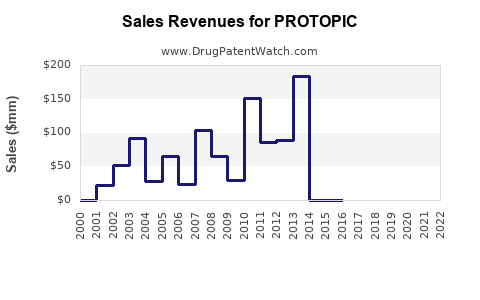

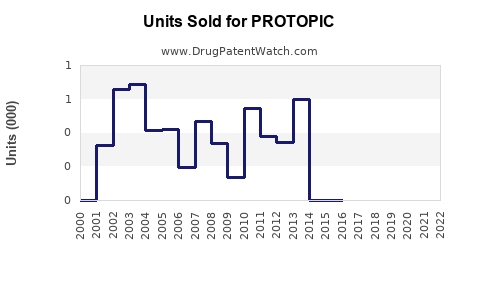

Annual Sales Revenues and Units Sold for PROTOPIC

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| PROTOPIC | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| PROTOPIC | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| PROTOPIC | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| PROTOPIC | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| PROTOPIC | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for PROTOPIC (tacrolimus ointment)

Overview

PROTOPIC, a topical calcineurin inhibitor (tacrolimus), is primarily prescribed for atopic dermatitis (eczema). Approved by the FDA in 2000, it maintains a niche in dermatology but faces competition from corticosteroids and emerging biologics. Its unique mechanism of modulating immune response positions it as an alternative for steroid-sensitive patients and those with steroid-induced skin atrophy risks.

Market Size and Segments

The global atopic dermatitis market was valued at approximately USD 5 billion in 2022, with topical treatments accounting for 70% (USD 3.5 billion). PROTOPIC’s primary market is North America, where atopic dermatitis prevalence affects up to 10-20% of children and 3-5% of adults according to the National Eczema Association. Europe follows, with similar prevalence rates.

Competitive Landscape

Main competitors in topical eczema treatment include:

- Corticosteroids: the most prescribed, but limited by steroid-sparing concerns.

- Topical calcineurin inhibitors: PROTOPIC and PIMECOOL (pimecrolimus).

- Biologics: Dupilumab (DUPIXENT) approved in 2017, expanding options for moderate-to-severe cases.

Market Share and Positioning

In 2022, PROTOPIC held an estimated 15-20% market share among topical agents for atopic dermatitis in the U.S., with sales roughly USD 200 million. Pimecrolimus dominates the calcineurin class with approximately 60% market share. PROTOPIC’s positioning as a second-line agent influences its market penetration.

Sales Dynamics and Growth Drivers

Factors driving sales include:

- Increasing prevalence of atopic dermatitis, projected to grow at 4% annually over the next five years.

- Rising awareness of steroid-sparing treatments.

- Prescriber shift towards immune-modulating agents, especially for pediatric populations.

- Reimbursement policies favoring non-steroidal alternatives for long-term management.

Challenges and Limitations

- Black box warning for risk of malignancy and skin cancer, introduced in 2005, limits widespread use.

- Competition from biologics like Dupilumab, which, despite higher costs, offers systemic management for severe cases.

- Patient concerns regarding potential adverse effects.

Sales Projections (2023-2028)

| Year | Estimated Sales (USD millions) | Notes |

|---|---|---|

| 2023 | 220 | Market stabilizing; increased prescriber awareness |

| 2024 | 240 | Slight growth as awareness continues; new formulations considered |

| 2025 | 270 | Growth driven by expanding pediatric use |

| 2026 | 300 | Market expansion in Europe and Asia |

| 2027 | 330 | Competitive pressures from biologics and generics |

| 2028 | 360 | Continued growth, potential entry of biosimilars |

Growth rate averages 8–10% annually, influenced by atopic dermatitis prevalence, market expansion, and prescriber preferences.

Regional Considerations

- North America dominates, accounting for 60-65% of sales.

- Europe’s market grows at 5-7%, influenced by approval in multiple countries and reimbursement practices.

- Asia-Pacific markets begin rapid growth phases, with increasing eczema prevalence and healthcare infrastructure improvements.

Regulatory Trends and Impact

- Ongoing safety evaluations may impact prescribing patterns.

- Potential approval of new formulations or combination therapies could expand market share.

- Patent expirations are not imminent; however, biosimilar development in the calcineurin inhibitor class may pressure prices in the coming decade.

Summary of Strategic Opportunities

- Invest in marketing campaigns emphasizing steroid-sparing benefits.

- Expand pediatric prescriptions through safety profile improvements.

- Explore combination therapies to enhance efficacy.

- Leverage biosimilar development to increase market penetration.

Key Takeaways

- PROTOPIC remains a significant but niche player in the topical atopic dermatitis market.

- Sales are stabilized with moderate growth prospects driven by increasing prevalence and prescriber adoption.

- Market dynamics are influenced by safety concerns, competition from biologics, and regulatory policies.

- Regional expansion, especially into Asia-Pacific, offers growth opportunities.

- The threat of biosimilars could diminish prices and margins over time.

FAQs

-

What factors limit PROTOPIC’s market expansion?

Safety concerns related to malignancy risk, competition from biologics, and restrictions on long-term use limit broader adoption. -

How does PROTOPIC compare to Pimecrolimus?

PROTOPIC has higher potency and is often prescribed for more severe cases, while Pimecrolimus is favored for milder eczema and has a greater share in the calcineurin class. -

What is the outlook for biosimilar entry?

Biosimilars targeting tacrolimus are in early development stages, but approval could pressure prices and market shares within 5-10 years. -

Which regions pose the greatest growth potential?

Asia-Pacific markets exhibit high growth potential driven by rising eczema prevalence and expanding healthcare access. -

Are new formulations expected for PROTOPIC?

Yes, reformulations emphasizing safety and ease of use are under development, potentially impacting market share positively.

References

[1] GlobalData. “Atopic dermatitis Market Report,” 2022.

[2] National Eczema Association. “Atopic Dermatitis Facts,” 2022.

[3] FDA. “Labeling Changes for Topical Tacrolimus,” 2005.

[4] IQVIA. “Pharmaceutical Market Data,” 2022.

[5] Grand View Research. “Topical Drug Market Analysis,” 2023.

More… ↓