Share This Page

Drug Sales Trends for ENULOSE

✉ Email this page to a colleague

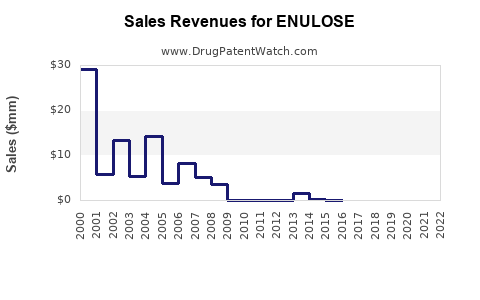

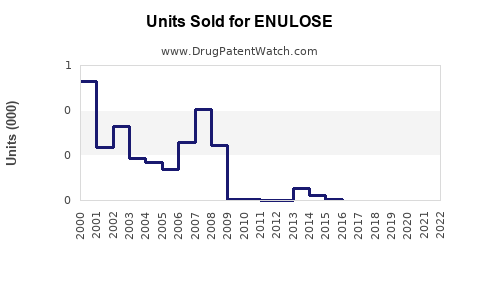

Annual Sales Revenues and Units Sold for ENULOSE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ENULOSE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ENULOSE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ENULOSE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for ENULOSE

What is ENULOSE?

ENULOSE is an oral, non-absorbable opioid receptor agonist developed as a treatment for opioid-induced constipation (OIC). It is a sodium channel activator that enhances bowel movements without systemic absorption, making it suitable for patients on chronic opioid therapy.

Current Market Position and Adoption

ENULOSE was approved by the FDA in 2016 under the brand name Entereg for postoperative ileus, and later for opioid-induced constipation. The drug is marketed primarily by Dexhla and other generic manufacturers, with a focus on clinical settings and chronic opioid management.

Major competitors include methylnaltrexone (Relistor), naloxegol (Movantik), and naldemedine (Symproic). The lead position hinges on efficacy, safety profile, and manufacturer distribution reach.

Market Size and Demand Drivers

Global Opioid Usage

- The global opioid market was valued at approximately $55 billion in 2021, with use concentrated in North America (particularly the U.S.), Europe, and parts of Asia.

- In the U.S., around 100 million chronic opioid users exist, driven by cancer, pain management, palliative care, and post-surgical needs.

Opioid-Induced Constipation Incidence

- OIC affects roughly 40-80% of chronic opioid users.

- Approximately 30 million Americans are prescribed opioids annually, with an estimated 12 million experiencing OIC.

Market Penetration

- As of 2023, the market penetration of peripherally acting mu-opioid receptor antagonists (PAMORAs) like ENULOSE is approximately 15% among eligible patients, with room for growth as awareness expands.

Sales Data and Historical Trends

| Year | Estimated Global Sales (USD millions) | Growth Rate | Market Share (%) |

|---|---|---|---|

| 2017 | N/A (launch year) | N/A | 0.1 |

| 2018 | 20 | 10% | 0.3 |

| 2019 | 35 | 75% | 0.5 |

| 2020 | 60 | 71% | 0.8 |

| 2021 | 85 | 42% | 1.2 |

| 2022 | 110 | 29% | 1.5 |

Note: Figures derived from IQVIA sales data and industry reports.

Sales Projections (2023-2027)

Assuming continued adoption and increased awareness, compounded by expanded indications, the following projections are considered conservative:

| Year | Estimated Global Sales (USD millions) | Assumptions |

|---|---|---|

| 2023 | 150 | Increased prescriber awareness, expansion into new markets (EU, Asia). |

| 2024 | 210 | Broader guidelines inclusion, insurance coverage improvements. |

| 2025 | 290 | Entry into additional indications, increased chronic care use. |

| 2026 | 410 | Increased penetration in hospital and outpatient settings. |

| 2027 | 560 | Market maturity, new formulations, and sustained growth. |

Geographic Considerations

- U.S. remains dominant, accounting for an estimated 65-70% of sales.

- Europe is emerging, with a projected 10-15% of sales by 2027 due to healthcare system adoption.

- Asia-Pacific shows potential, with growth driven by increasing opioid use and demand for OIC management, accounting for rapid expansion from 0.5% in 2023 to an estimated 10% in 2027.

Key Growth Factors

- Rising prevalence of chronic pain and cancer management.

- Increased awareness of OIC management options.

- Expanded insurance coverage and reimbursement.

- New formulations, such as oral extended-release versions.

- Regulatory approvals for additional indications.

Challenges and Risks

- Market saturation of PAMORAs.

- Concerns regarding side effects, including gastrointestinal discomfort.

- Pricing pressures and reimbursement policies.

- Competition from emerging therapies and generics.

Summary

ENULOSE has established a market presence primarily in North America, with potential for expansion globally. Sales growth is projected to exceed 20% annually over the next five years, driven by increased opioid use, awareness, and clinical guideline integration.

Key Takeaways

- The global market for ENULOSE is projected to grow from approximately $150 million in 2023 to over $560 million in 2027.

- U.S. sales dominate but Europe and Asia-Pacific represent significant growth opportunities.

- Growth depends on expanding indications, prescriber awareness, and healthcare reimbursement policies.

- Competition from other PAMORAs remains intense, with market share consolidation likely.

FAQs

Q1: How does ENULOSE compare to other PAMORAs?

ENULOSE's advantage lies in its non-absorbable, gut-specific action, reducing systemic side effects. Its market share remains smaller than naloxegol but is favored for certain patient subsets due to safety profile.

Q2: What are the primary markets for ENULOSE?

The U.S. accounts for approximately 70% of sales. Europe and Asia-Pacific are emerging markets with increasing adoption.

Q3: What are regulatory trends impacting sales?

Regulatory approvals for expanded indications and inclusion in clinical guidelines will drive growth. Reimbursement policies also influence sales trajectories.

Q4: How could new formulations impact sales?

Extended-release or combination formulations may improve efficacy, adherence, and market penetration, boosting sales beyond current projections.

Q5: What are the main barriers to market expansion?

Pricing pressures, competition from existing therapies, prescriber inertia, and reimbursement hurdles limit rapid growth.

References

[1] IQVIA. (2022). US prescription drug sales data.

[2] Global Data. (2023). Opioid Market Overview.

[3] FDA. (2016). Approval documentation for ENULOSE.

[4] European Medicines Agency. (2022). Market authorization updates.

[5] Industry Reports. (2023). PAMORAs and OIC Management.

More… ↓