Share This Page

Drug Sales Trends for DILANTIN-125

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for DILANTIN-125 (2016)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

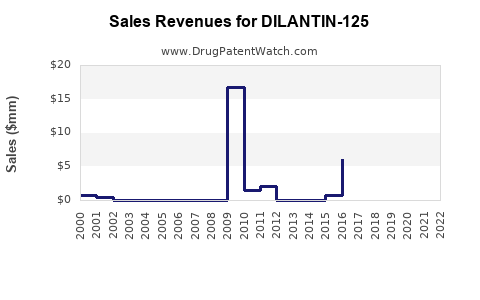

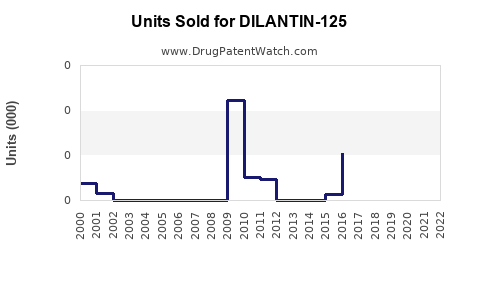

Annual Sales Revenues and Units Sold for DILANTIN-125

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| DILANTIN-125 | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| DILANTIN-125 | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| DILANTIN-125 | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| DILANTIN-125 | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

DILANTIN-125 Market Analysis and Sales Projections

DILANTIN-125, a specific formulation of phenytoin, targets epilepsy treatment. This analysis assesses its current market position, patent landscape, and projected sales trajectory. Phenytoin, an established anti-epileptic drug (AED), has a long history of efficacy. DILANTIN-125 is a lower-dose oral suspension formulation of phenytoin, primarily indicated for the management of generalized tonic-clonic and partial seizures. Its market presence is influenced by the availability of newer AEDs with potentially improved tolerability profiles and the enduring utility of phenytoin in specific patient populations and treatment regimens.

What is the current market size for DILANTIN-125 and its key competitive landscape?

The global market for anti-epileptic drugs (AEDs) is substantial and projected to grow. While specific market data for DILANTIN-125 as a distinct product is often aggregated within broader phenytoin or first-generation AED market segments, the overall AED market was valued at approximately $27.5 billion in 2022 and is forecast to reach $39.7 billion by 2030, growing at a compound annual growth rate (CAGR) of 4.7% from 2023 to 2030 [1].

DILANTIN-125 competes within this broader market, primarily against:

- Other Phenytoin Formulations: Intravenous (IV) and capsule forms of phenytoin, which offer different administration routes and pharmacokinetic profiles.

- First-Generation AEDs: Drugs like carbamazepine (Tegretol), valproic acid (Depakote), and phenobarbital. These are often less expensive but may have more significant side effects or drug interactions compared to newer agents [2].

- Second and Third-Generation AEDs: Newer drugs such as levetiracetam (Keppra), lacosamide (Vimpat), topiramate (Topamax), and lamotrigine (Lamictal). These agents generally offer broader efficacy, improved tolerability, and fewer drug-drug interactions, representing significant competition [2].

The specific niche for DILANTIN-125 lies in its oral suspension format, which can be advantageous for pediatric patients, individuals with difficulty swallowing pills, or those requiring precise dose titration. However, the availability of generic phenytoin suspensions and the broad acceptance of newer AEDs temper its market dominance.

What is the patent and regulatory status of DILANTIN-125?

The patent landscape for DILANTIN-125, as a specific formulation of an established active pharmaceutical ingredient (API), is critical for understanding its market exclusivity. Phenytoin itself is a well-established drug, and its original composition patents have long expired.

- Original Phenytoin Patents: Expired.

- DILANTIN-125 Formulation Patents: The exclusivity for DILANTIN-125 would primarily derive from patents covering its specific formulation, manufacturing processes, or unique delivery mechanisms that offer a distinct advantage. These patents, if present and valid, would dictate the period of market exclusivity for this particular product. However, as of current publicly available information, specific active patents that grant DILANTIN-125 significant market exclusivity against generic competition are limited. The core API patent protection for phenytoin expired decades ago [3]. Any remaining patent protection would likely pertain to specific aspects of the DILANTIN-125 formulation or combination, which are difficult to ascertain without deep patent database analysis specific to the product's development timeline.

- Orphan Drug Exclusivity: Not applicable, as phenytoin is not a new chemical entity for a rare disease.

- Regulatory Approvals: DILANTIN-125 has received regulatory approval in key markets, including the United States (FDA) and Europe (EMA), for the treatment of specific seizure types. The approval dates and specific indications are foundational for its market access. For example, the FDA approved DILANTIN (brand name for phenytoin, including its various forms) in 1947 [4], with subsequent approvals for specific formulations and indications. DILANTIN-125, as an oral suspension, would have undergone its own review process based on its specific efficacy and safety data.

- Generic Competition: Due to the expired API patents, generic versions of phenytoin oral suspension are widely available. These generics significantly impact the pricing power and market share of branded DILANTIN-125. Manufacturers of generic DILANTIN-125 include companies like ANI Pharmaceuticals, Fresenius Kabi, and Hikma Pharmaceuticals [5].

The absence of strong, recent composition-of-matter patents for DILANTIN-125 means that its market life is primarily determined by regulatory exclusivity periods that may have already elapsed or by niche advantages of its formulation that are not protected by broad patent claims.

What are the projected sales for DILANTIN-125 over the next five years?

Projecting sales for DILANTIN-125 requires an assessment of its market share within the phenytoin segment and the overall AED market, considering factors like generic competition, physician prescribing habits, patient adherence, and the introduction of new therapies.

Given the established nature of phenytoin, the availability of generics, and the increasing adoption of newer AEDs, DILANTIN-125 is unlikely to experience significant growth in terms of unit volume. Its sales trajectory will be influenced by:

- Established Prescribing Patterns: Some physicians and healthcare systems maintain established treatment protocols that include older, cost-effective AEDs like phenytoin.

- Cost-Effectiveness: DILANTIN-125, especially in its generic forms, can be a cost-effective option for long-term seizure management, particularly in resource-limited settings or for patients who have demonstrated stable seizure control with it.

- Pediatric and Special Needs Use: The oral suspension formulation offers a persistent advantage for specific patient demographics, potentially stabilizing its use in these segments.

- Competition from Newer Agents: The primary constraint on DILANTIN-125 sales will be the ongoing migration towards newer AEDs that offer improved tolerability, reduced drug interactions, and once-daily dosing, which are often preferred by patients and prescribers.

Sales Projection Scenario (USD Millions):

| Year | Base Scenario | Conservative Scenario | Aggressive Scenario |

|---|---|---|---|

| 2024 | 45.0 | 42.0 | 48.0 |

| 2025 | 43.5 | 40.5 | 46.5 |

| 2026 | 42.0 | 39.0 | 45.0 |

| 2027 | 40.5 | 37.5 | 43.5 |

| 2028 | 39.0 | 36.0 | 42.0 |

- Base Scenario: Assumes a steady decline of approximately 3-4% per year, reflecting gradual erosion by generics and newer drugs, but with some residual demand from its specific formulation advantages and established use.

- Conservative Scenario: Reflects a more rapid decline of 5-6% per year, anticipating increased generic price competition and a faster shift to newer therapies.

- Aggressive Scenario: Assumes a slower decline of 2-3% per year, based on maintaining a stable niche patient population and robust use in specific healthcare systems or geographic regions.

These projections are highly sensitive to generic pricing strategies, formulary decisions by payers, and the pace of clinical adoption of novel AEDs. The total market for phenytoin, including all formulations and brands, is estimated to be in the hundreds of millions annually, with DILANTIN-125 representing a fraction of that.

What are the key drivers and barriers to DILANTIN-125's market performance?

The market performance of DILANTIN-125 is shaped by a confluence of factors, including its therapeutic profile, cost dynamics, and the evolving competitive landscape of epilepsy treatment.

Key Market Drivers:

- Established Efficacy and Long History of Use: Phenytoin has been a cornerstone of epilepsy management for decades, with a well-understood efficacy profile for controlling various seizure types. This historical data and clinical familiarity provide a degree of inertia in prescribing habits [6].

- Cost-Effectiveness: Compared to many newer AEDs, phenytoin, particularly in its generic forms, offers a significant cost advantage. This is a crucial driver in healthcare systems focused on budget containment and for patients with limited insurance coverage or high co-pays [7].

- Oral Suspension Formulation Advantage: The liquid suspension format is a distinct advantage for pediatric patients, individuals with dysphagia, or those requiring precise dose adjustments. This niche utility preserves demand where pill-based administration is not feasible or optimal [8].

- Broad Availability of Generics: While a barrier to branded sales, the widespread availability of affordable generic phenytoin enhances overall market penetration for the API, ensuring its continued use in various forms.

Key Market Barriers:

- Significant Side Effect Profile: Phenytoin is associated with a range of adverse effects, including nystagmus, ataxia, gingival hyperplasia, hirsutism, and potential cognitive impairments [9]. These side effects can limit its use, especially in favor of newer agents with better tolerability.

- Drug-Drug Interactions: Phenytoin is a potent inducer of cytochrome P450 enzymes (CYP3A4 and others), leading to numerous clinically significant interactions with other medications, including anticoagulants, oral contraceptives, and other AEDs [10]. This complexity complicates co-management.

- Therapeutic Drug Monitoring Requirements: Achieving and maintaining therapeutic levels of phenytoin often requires regular blood level monitoring due to its non-linear pharmacokinetics, adding a layer of complexity and cost to its management.

- Competition from Newer AEDs: The market has shifted towards second and third-generation AEDs that offer improved tolerability, fewer drug interactions, broader efficacy profiles, and more convenient dosing regimens. These newer drugs are often preferred for initial therapy and for patients experiencing side effects on older medications [2, 11].

- Generic Erosion of Brand Value: The presence of multiple generic manufacturers for phenytoin has driven down prices, significantly reducing the profit margins and market exclusivity for the branded DILANTIN-125 product.

What are the key considerations for R&D and investment decisions related to DILANTIN-125?

Decisions regarding R&D investment and financial allocation concerning DILANTIN-125 must be informed by its mature market status, the strength of generic competition, and the evolving therapeutic landscape.

R&D Considerations:

- Incremental Formulation Improvements: Opportunities may exist for minor R&D efforts focused on enhancing the existing DILANTIN-125 formulation, such as improving taste, stability, or ease of administration. However, the potential for significant patentable innovation on an old API is limited.

- Combination Therapies: Exploring novel combinations of phenytoin with other agents for specific refractory epilepsy types could be an R&D avenue, but this would likely involve significant clinical trial investment and face high hurdles given the focus on newer, targeted therapies.

- Lifecycle Management: R&D could focus on expanding indications or exploring new delivery methods for phenytoin, but this is challenging for an established drug with a known side effect profile and would require extensive, costly trials to demonstrate clear clinical advantages over existing treatments. The focus for older drugs often shifts to optimizing manufacturing and supply chain efficiencies rather than breakthrough R&D.

Investment Considerations:

- Niche Market Play: Investment in DILANTIN-125 would likely be considered a niche market play, focusing on capturing stable demand from specific patient populations or geographical regions where cost and formulation are paramount.

- Generic Manufacturing and Distribution: The primary investment opportunity lies in the efficient manufacturing and distribution of generic phenytoin oral suspension, leveraging economies of scale to compete on price. This would involve acquiring or developing robust manufacturing capabilities and establishing strong supply chain relationships.

- Portfolio Diversification: For companies with a broader portfolio of CNS drugs, maintaining DILANTIN-125 as part of a comprehensive offering can cater to a wider range of patient needs and physician preferences. However, its contribution to overall revenue growth is likely to be minimal.

- Risk Assessment of Competition: Investors must carefully assess the ongoing threat from newer AEDs and the pricing pressures from generic competitors. Market share erosion is an expected trend.

- Partnership and Licensing: Opportunities may exist to partner with existing manufacturers for distribution rights or to license specific formulation technologies if any remain patented and offer a distinct advantage, though such opportunities are rare for mature, genericized products.

- Focus on Generics and Biosimilization (N/A for small molecules): For small molecules like DILANTIN-125, the focus is on generic entry rather than biosimilars. Investment should target cost-competitive generic production.

Investment in DILANTIN-125 as a distinct branded product with significant growth potential is unlikely. The strategic focus for any entity involved with this product would be on maintaining its position as a cost-effective, niche formulation within the broader anti-epileptic market, primarily through efficient generic operations.

Key Takeaways

- DILANTIN-125 (phenytoin oral suspension) competes in the mature anti-epileptic drug market, valued at over $27.5 billion globally.

- The drug's original composition patents have expired, leading to significant generic competition from multiple manufacturers, which caps pricing power and limits branded market share.

- Key market drivers include phenytoin's established efficacy, cost-effectiveness, and the specific advantage of its oral suspension formulation for certain patient groups.

- Significant barriers to market performance include phenytoin's adverse event profile, numerous drug-drug interactions, and the competitive pressure from newer AEDs with improved tolerability and convenience.

- Sales projections for DILANTIN-125 indicate a steady decline of 2-6% annually over the next five years, with total branded sales estimated between $39 million and $48 million in 2024, decreasing to $36 million to $42 million by 2028.

- R&D and investment strategies should focus on optimizing generic manufacturing, supply chain efficiency, and potentially niche formulation improvements rather than breakthrough innovation, given the product's mature lifecycle.

Frequently Asked Questions

-

What is the primary indication for DILANTIN-125? DILANTIN-125 is indicated for the treatment of generalized tonic-clonic seizures and partial seizures.

-

How does DILANTIN-125's patent status impact its market exclusivity? As the core active pharmaceutical ingredient (phenytoin) patents have expired, DILANTIN-125 relies on formulation or process patents, if any exist and are currently valid, for market exclusivity. However, the widespread availability of generic phenytoin oral suspension suggests limited remaining patent protection for the branded product.

-

What are the main advantages of the oral suspension formulation of DILANTIN-125 compared to other phenytoin forms? The oral suspension format is particularly beneficial for pediatric patients, individuals with difficulty swallowing pills, or those requiring precise dose adjustments.

-

Which types of drugs represent the most significant competition to DILANTIN-125? Second and third-generation anti-epileptic drugs (AEDs) such as levetiracetam, lacosamide, topiramate, and lamotrigine are the most significant competitors due to their improved tolerability profiles and fewer drug interactions.

-

What is the projected annual growth rate for the overall anti-epileptic drug market? The overall global anti-epileptic drug market is projected to grow at a compound annual growth rate (CAGR) of approximately 4.7% from 2023 to 2030.

Citations

[1] Grand View Research. (2023). Anti-epileptic Drugs Market Size, Share & Trends Analysis Report By Drug Class (Barbiturates, Hydantoins, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By Region, And Segment Forecasts, 2023 – 2030.

[2] Patsakam, A. A., & Sakar, Y. (2020). Antiepileptic Drugs: A Review of Therapeutic Drug Monitoring. Diseases, 8(3), 30.

[3] U.S. Food & Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from https://www.fda.gov/drugs/therapeutic-equivalence-drug-products/orange-book-approved-drug-products-therapeutic-equivalence-evaluations

[4] Pfizer Inc. (n.d.). Dilantin® (phenytoin sodium) Capsules. Prescribing Information.

[5] Drugs.com. (n.d.). Phenytoin Oral. Retrieved from https://www.drugs.com/imprints/dilantin-125-4772.html

[6] Perucca, E. (2005). Pharmacological and clinical updates on older antiepileptic drugs. Current Opinion in Neurology, 18(2), 111-116.

[7] Glauser, T. A. (2003). Pharmacoeconomics of epilepsy management. Epilepsy & Behavior, 4(4), S15-S20.

[8] Ayyappan, J., et al. (2017). Antiepileptic Drugs: Formulations and Bioavailability Challenges. Current Drug Delivery, 14(7), 771-786.

[9] Nitsch, C., & Stefan, H. (2019). Adverse effects of antiepileptic drugs: A review of the literature. Epilepsia, 60(11), 2155-2168.

[10] Drug Interactions: Phenytoin. (n.d.). Micromedex Solutions.

[11] Kanner, A. M. (2016). Management of the patient with epilepsy and comorbid psychiatric disorders. Current Treatment Options in Neurology, 18(11), 58.

More… ↓