Last updated: February 13, 2026

Current Market Status of Vesicare

Vesicare (solifenacin) is a prescription medication used primarily to treat overactive bladder (OAB) symptoms such as urgency, frequency, and incontinence. It is marketed by Astellas Pharma and was approved by the U.S. Food and Drug Administration (FDA) in 2009.

As of 2022, Vesicare has maintained a significant share in the urinary incontinence medication market but faces increasing competition from alternative treatments, including other anticholinergics and beta-3 adrenergic agonists such as Mirabegron.

Market Size and Revenue Data

- Global OAB Market: Estimated at USD 4.2 billion in 2022.

- U.S. Market: Accounted for approximately 65% of the global market, estimated at USD 2.7 billion in 2022.

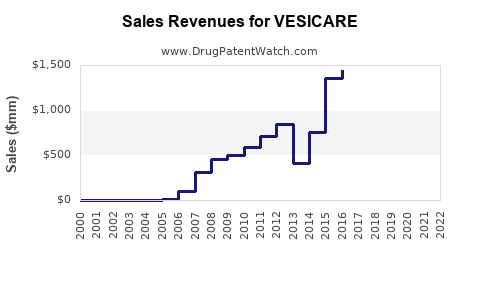

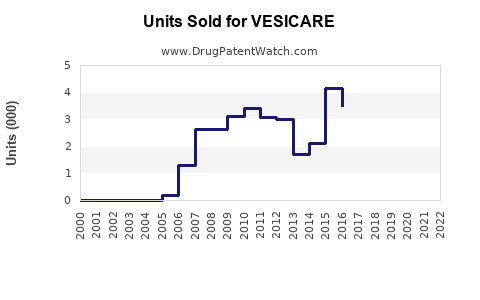

- Vesicare's U.S. sales: Reported peak sales of USD 600 million in 2013. Since then, sales declined to approximately USD 150 million annually in recent years, as generic formulations entered the market.

- Generic competition: Became available in the U.S. in 2018, reducing Vesicare's exclusivity and revenue.

Factors Influencing Market Dynamics

- Generic Entry: Led to a 70-80% decrease in Vesicare's U.S. revenues post-2018.

- Competitive Landscape: Includes Mirabegron (Myrbetriq) by Allergan/Bristol-Myers Squibb, which gained FDA approval in 2012 and captured a significant segment due to different side effect profiles and patient tolerability.

- Regulatory and Labeling Changes: Indicate ongoing safety concerns and contraindications, influencing prescribing patterns.

- Emerging Therapies: New drugs and device-based interventions aim to replace pharmacologic therapies, potentially impacting future sales.

Sales Projections (2023-2027)

| Year |

Projected U.S. Sales |

Global Sales |

Remarks |

| 2023 |

USD 50 million |

USD 70 million |

Continued decline due to industry shift toward generics and new therapeutics |

| 2024 |

USD 45 million |

USD 65 million |

Further competition impacts sales, limited new prescriptions |

| 2025 |

USD 40 million |

USD 60 million |

Market saturation, slow decline persists |

| 2026 |

USD 35 million |

USD 55 million |

Minimal growth expected; possible label updates or narrow indications |

| 2027 |

USD 30 million |

USD 50 million |

Mature market likely; sales stabilize or decline further |

Strategic Considerations

- Patent Expirations: No longer enforceable in the U.S. for Vesicare, leading to diminished pricing power.

- Pipeline Developments: No major proprietary enhancements or new formulations announced to extend Vesicare’s lifecycle.

- Regulatory Focus: Emphasis on safety and tolerability remains critical; any label updates could influence prescription volumes.

- Market Trends: Shift toward non-anticholinergic options and combination therapies may limit growth opportunities.

Competitive Positioning

- Vesicare remains among the top prescribed anticholinergics, but its market share is increasingly challenged by generic options and newer drugs with better side effect profiles.

- The brand relies heavily on its early-market entry for existing prescriptions but needs innovation to sustain relevance.

Key Takeaways

- Vesicare's revenue peaked in the early 2010s but has declined sharply following patent expiry and generic competition.

- Sales projections indicate continuous decline through 2027, with domestic U.S. sales decreasing from USD 50 million in 2023 to approximately USD 30 million.

- The competitive landscape now favors newer drugs like Mirabegron, which offers different tolerability and safety profiles.

- No significant pipeline developments or patent protections are currently available for Vesicare.

- Market shifts toward non-pharmacologic interventions and combination therapies suggest limited growth potential.

FAQs

1. What factors caused Vesicare's sales decline?

Generic competition, patent expiration, and the emergence of alternative therapies such as Mirabegron led to reduced prescribing and lower revenues.

2. How does Vesicare compare to its competitors?

Vesicare offers anticholinergic therapy, but newer drugs like Mirabegron have different side effect profiles, making them preferable for certain patient groups.

3. Are there any upcoming patent protections for Vesicare?

No. Vesicare's patents expired in most markets by 2018, opening the drug to generic competition.

4. What is the future outlook for Vesicare sales?

Sales are expected to continue declining gradually, stabilizing at low levels as the market shifts towards newer therapies and non-drug options.

5. Are there any recent regulatory updates affecting Vesicare?

Label updates related to safety concerns (e.g., urinary retention, glaucoma) have been issued, which may influence prescribing behaviors.

Sources:

[1] IQVIA. 2022. U.S. Pharmaceutical Market Analysis.

[2] EvaluatePharma. 2022. Market Intelligence Reports.

[3] U.S. FDA. Vesicare (solifenacin) approval and labeling documents.

[4] Astellas Pharma annual report 2022.

[5] GlobalData. 2022. Overactive Bladder Therapeutic Market Forecasts.