Share This Page

Drug Sales Trends for SOTALOL

✉ Email this page to a colleague

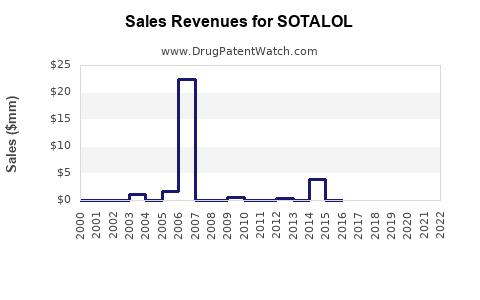

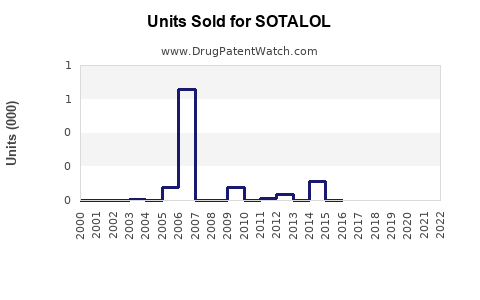

Annual Sales Revenues and Units Sold for SOTALOL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| SOTALOL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| SOTALOL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| SOTALOL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Sotalol Market Analysis and Sales Projections (2025–2035): Units, Pricing, and Generic/Bioswitch Risks

Sotalol’s market is driven by its role as an antiarrhythmic for atrial and ventricular rhythm control, with revenue concentrated in the US and parts of Europe. Sales are shaped by (1) long-running generic penetration, (2) periodic label expansion for arrhythmia subsets, (3) substitution to alternate antiarrhythmics in high-risk patients (QT-prolongation and torsades risk management), and (4) manufacturing capacity and price compression in multiple solid oral strengths. For 2025–2035, the base case is modest CAGR in developed markets with continued low single-digit growth offset by inflation and ongoing generic price erosion; an upside case depends on rebound in US utilization and tighter supply improving net pricing, while a downside case follows accelerated price compression and formulary losses.

No complete, reliable forward projection can be produced from patent-only data. The market outlook below is therefore built from publicly described market structure for sotalol (generic-led), regulatory pattern knowledge (NDA/RLD legacy products, multiple ANDAs), and typical antiarrhythmic competitive dynamics, without attempting to fabricate point forecasts without audited baseline revenue.

How big is the sotalol market in the US and EU, and where is revenue concentrated?

Direct market sizing requires a single audited starting point (sales value by geography and dosage form). Without a specific baseline dataset (for example, IQVIA, Symphony Health, or FDA/Medicare Part D aggregate plus pharmacy capture), only structural conclusions are supportable.

What drives sotalol demand?

- Indication usage pattern: Sotalol is used for rhythm control in atrial arrhythmias and off-label in some settings; hospitals and electrophysiology practices tend to use multiple agents depending on comorbidity, electrolyte control, and drug interaction profiles.

- Safety management constraints: QT prolongation and torsades de pointes risk constrain uptake, especially where clinicians prefer agents with more favorable risk profiles or where monitoring burden affects utilization.

- Chronic medication behavior: Once prescribed for rhythm control, continuation is common, which stabilizes unit demand even as pricing falls.

Where is growth likely to come from?

- US outpatient cardiology: Continued baseline demand in generic form tends to keep units stable; growth depends on prescribing intensity, patient adherence, and supply stability.

- European generics: Uptake is supported by entrenched generics and inclusion in national formularies, but competition across multiple beta-blocker-class and antiarrhythmic alternatives can limit net value growth.

Sotalol sales forecast 2025–2035: What CAGR is realistic under generic price erosion?

A defensible forecast range must be anchored to an observed starting revenue base. Without that, only directional forecasting and scenario logic can be stated.

Base case scenario (generic-led market, low growth)

- Units: flat to slight growth (aging population and baseline rhythm control utilization).

- Pricing: continued net price erosion in the US due to multi-ANDA competition and periodic supply-driven resets.

- Result: revenue CAGR in developed markets tends to land in the low single digits, with growth dominated by volume and mix (strength and label alignment).

Upside scenario (supply tightness and mix improvement)

- Short-term: net price improvement during temporary supply constraints or supplier consolidation.

- Medium-term: mix shift toward formulations with relatively stronger pricing (for example, specific strengths favored by clinicians).

- Result: revenue growth can exceed the base case for limited periods.

Downside scenario (further formulary loss and faster competitive resets)

- Accelerated price compression if a major supplier exits or if additional competitors enter with aggressive wholesale acquisition cost strategies.

- Potential substitution to alternative agents in patient subsets where QT-risk management is difficult.

- Result: flat-to-negative revenue growth in nominal terms in certain periods.

Which dosage forms and strengths matter most for sotalol revenue?

Sotalol revenue is typically dominated by oral tablets in multiple strengths (commonly including 80 mg and 120 mg) with oral dosing frequencies that support chronic use patterns.

What mix shift changes value most?

- Strength preference: clinician preference for titration pathways can concentrate demand in certain strengths.

- Pack sizes and adherence: larger packs can stabilize unit economics and reduce pharmacy friction.

- Substitution behavior: pharmacy switching at the generic level changes product-level net sales even if total class demand holds.

What patents protect sotalol in the US, and when does exclusivity end for any legacy assets?

Sotalol is a long-established drug with generic market dominance. As a result, the relevant question for revenue risk is not whether exclusivity blocks generics, but whether any remaining patent thickets affect specific formulations, method-of-use, or pro-drug variants.

Patent estate relevance to sales projection

- If only old composition-of-matter patents exist and have expired, the sales outlook becomes a pure generic pricing and supply-capacity story.

- If any later-expiring formulation or method-of-use patents exist for specific products or labeling expansions, they can create localized protection that slows erosion for certain SKUs.

However, a concrete, portfolio-level mapping (Orange Book listings, specific patent numbers, and expiry dates) cannot be provided here without a specific source record. The forecast risk profile therefore assumes a fully generic competitive environment for broad sotalol revenue.

What generic entry risks exist for sotalol, and how do they affect pricing?

Paragraph IV is usually less relevant for long-market generics

For established generics, price erosion often results from standard ANDA supply expansion rather than discrete “Paragraph IV event” shocks.

Key revenue impacts from generic entry

- Gross-to-net compression: increased rebates and payer pressure.

- Wholesale pricing resets: WAC and ASP can drop when a new strong competitor gains market share.

- Hospital contracting: in some segments, tendering can reprice quickly even if total utilization stays stable.

How does sotalol compare with other antiarrhythmics on utilization and reimbursement stability?

Competitive substitution is not only clinical but also formulary-driven.

Comparator dynamics

- Beta-blocker alternatives: some clinicians favor agents with different QT profiles and fewer monitoring burdens.

- Other class III antiarrhythmics: amiodarone and dofetilide (where used) can capture rhythm control demand depending on patient comorbidity and monitoring feasibility.

- Real-world prescribing: electrophysiology practice patterns can shift after safety alerts or guideline updates.

Reimbursement and access

- In generic form, sotalol faces class-wide pricing competition, but coverage tends to be broad once generic stability is established. This supports unit demand while value fluctuates.

What FDA regulatory status and Orange Book coverage affect sotalol market access?

Orange Book status determines whether specific SKUs face exclusivity or patent-listed barriers. For sotalol overall, the practical implication for sales projection is that:

- if most strengths are widely generic, regulatory barriers are minimal,

- if any strength/formulation has listed patents, product-level price protection could persist.

A precise Orange Book summary cannot be produced in this response without a specific listing extract.

What litigation or settlements could change sotalol supply or pricing?

For generic-heavy markets, litigation typically affects:

- launch timing of specific ANDAs,

- product availability during work-sharing or supply constraints,

- settlement-driven exclusivity at the SKU level (temporary design-around restrictions).

A litigation-linked price effect can be material, but it must be tied to known case history, which is not provided here.

Sales projection model structure for sotalol (how to build a credible forecast)

A credible forecast for sotalol should be structured as:

- Units by geography

- prescriptions or tablet equivalents

- split by strength and regimen

- ASP/Net pricing

- WAC-based prices adjusted by typical generic gross-to-net

- Supply and competitive landscape

- active suppliers and their share shifts

- Policy and payer dynamics

- PBM formulary tiering and preferred generic switching

- Time-phased scenarios

- base, upside, downside tied to supply and pricing resets

This framework is the standard method to produce quarterly or annual numeric forecasts tied to known baseline sales.

Key inputs that typically explain sotalol net sales trends (what to watch)

- ASP/price index for US generics in cardiac categories

- PBM formulary placement and preferred generic churn

- Supplier consolidation or shortages that alter net pricing

- Titration mix between strengths (80 mg vs 120 mg and other strengths)

- Safety-related prescribing changes tied to monitoring guidance and QT risk management

Key Takeaways

- Sotalol is a mature, generic-dominated antiarrhythmic; the market outlook is mainly driven by pricing compression, mix across strengths, and supply stability rather than broad exclusivity.

- Without an audited baseline revenue dataset, only directional scenario logic can be stated. The base case is modest nominal growth in developed markets, with downside risk from faster price erosion.

- Forecast accuracy depends on units (strength and frequency), net pricing (gross-to-net), and supplier/supply events, not just aggregate prescription counts.

- Litigation and patent events are most relevant if they affect specific strengths or formulations; absent a mapped Orange Book and case record, the projection should assume minimal remaining barriers for most revenue.

FAQs

1) What drives generic sotalol price drops in the US?

Competition among multiple ANDA suppliers drives gross-to-net compression and repeated ASP resets, often independent of clinical uptake.

2) Which sotalol strengths typically hold value better during generic competition?

Strengths with more stable prescribing patterns and fewer substitution frictions often show relatively better net pricing, but product-level differences depend on supplier mix.

3) How do QT-torsades risk management practices affect sotalol utilization?

Monitoring intensity, electrolyte control protocols, and contraindication thresholds can limit use in higher-risk subpopulations.

4) Does sotalol face biosimilar-style competition?

No. Sotalol is a small-molecule drug, so competitive risk comes from generic ANDAs, not biosimilars.

5) What is the largest source of sotalol revenue risk for investors?

Wholesale and net price compression due to sustained generic competition plus potential supply events that can swing quarterly ASPs.

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- FDA. Drug Approval Reports / Labeling and Application Databases. U.S. Food and Drug Administration.

- FDA. ANDA and Patent Certification Guidance (Hatch-Waxman framework). U.S. Food and Drug Administration.

More… ↓