Share This Page

Drug Sales Trends for DYRENIUM

✉ Email this page to a colleague

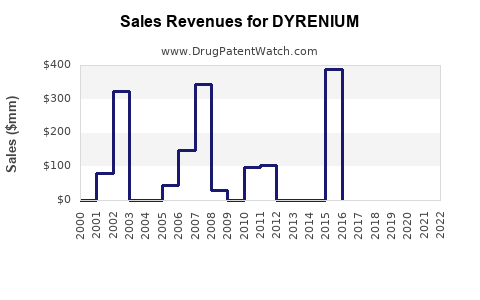

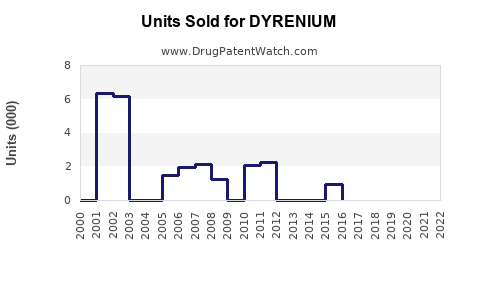

Annual Sales Revenues and Units Sold for DYRENIUM

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| DYRENIUM | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| DYRENIUM | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| DYRENIUM | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| DYRENIUM | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| DYRENIUM | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| DYRENIUM | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| DYRENIUM | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

DYRENIUM: Market Landscape and Sales Projections

Dyrenium (triamterene), a potassium-sparing diuretic, holds a niche in the treatment of edema and hypertension. Its market presence is characterized by established use, a mature patent landscape, and competition from other diuretic classes. This analysis projects future sales based on current market dynamics, clinical utility, and anticipated regulatory and competitive factors.

What is the Current Market Position of Dyrenium?

Dyrenium, a carbonic anhydrase inhibitor and sodium channel blocker, primarily functions by increasing sodium and water excretion while conserving potassium. It is indicated for the treatment of edema associated with congestive heart failure, liver cirrhosis, and renal disease. It is also used as an adjunct in the management of hypertension to potentiate the effect of other antihypertensive agents.

The drug has been available for decades, leading to a well-understood efficacy and safety profile. However, its clinical use has evolved with the advent of newer, more targeted therapies for cardiovascular and renal conditions. Dyrenium's market share is concentrated among patients for whom other diuretics are contraindicated or have proven ineffective, or as a combination therapy to mitigate hypokalemia.

Key market segments for Dyrenium include:

- Edema Management: Particularly in patients with chronic conditions like cirrhosis or heart failure where fluid retention is a primary symptom.

- Hypertension Adjunct Therapy: Used in combination with thiazide diuretics or other antihypertensives to achieve blood pressure control and balance electrolyte levels.

- Specific Renal Indications: As a component of treatment for certain types of renal tubular acidosis.

The overall market for diuretics is substantial, driven by the high prevalence of cardiovascular diseases and hypertension. Within this broad market, Dyrenium occupies a specialized segment, competing with other potassium-sparing diuretics such as amiloride and spironolactone, as well as loop and thiazide diuretics.

The global diuretic market was valued at approximately \$3.8 billion in 2022 and is projected to reach \$4.5 billion by 2028, growing at a CAGR of 2.5% [1]. Dyrenium's share of this market is estimated to be less than 5%, reflecting its specialized application and competition.

What is the Patent and Exclusivity Landscape for Dyrenium?

Dyrenium's active pharmaceutical ingredient, triamterene, was patented in the late 1950s, with its initial U.S. patent expiring long ago. The drug is currently available as a generic product from multiple manufacturers.

Key patent and exclusivity considerations:

- Original Composition of Matter Patents: Expired.

- Formulation Patents: Some older formulation patents may have expired, while newer, proprietary formulations or combination products could have existing or recently expired patents. For example, a combination product like Dyazide (triamterene and hydrochlorothiazide) had its own patent protection history.

- Exclusivity Periods: As a generic drug, Dyrenium does not benefit from New Drug Application (NDA) exclusivity periods that protect innovator drugs from generic competition for a set duration. The primary barrier to entry for generics is bioequivalence testing and FDA approval.

- Market Exclusivity: No market exclusivity is currently in place for Dyrenium as a single-agent product.

The absence of patent protection for the active pharmaceutical ingredient means the market is open to generic competition, which typically drives down prices and limits revenue potential for any single manufacturer. The long history of the drug also means it is well-established in clinical practice, but without significant innovation driving new market growth.

What are the Primary Clinical Applications and Patient Populations?

Dyrenium's primary clinical utility lies in its ability to promote diuresis while minimizing potassium loss, a critical advantage over other diuretic classes that can lead to hypokalemia.

Indications:

- Edema: Management of fluid retention in patients with congestive heart failure, liver cirrhosis, and renal disease. This often involves patients who have not responded adequately to other diuretics or who require potassium-sparing effects.

- Hypertension: Adjunctive therapy, typically in combination with a thiazide diuretic, to achieve blood pressure goals and prevent thiazide-induced hypokalemia.

- Renal Tubular Acidosis: Used in certain types of renal tubular acidosis to help alkalinize urine and prevent the formation of certain types of kidney stones.

Patient Demographics:

- Elderly Patients: Often have comorbidities that make them susceptible to electrolyte imbalances, making potassium-sparing diuretics beneficial.

- Patients with Chronic Kidney Disease (CKD): Where maintaining electrolyte balance is crucial.

- Patients with Hepatic Cirrhosis: Who commonly experience ascites and edema.

- Patients with Heart Failure: Where fluid overload is a significant concern.

The patient population for Dyrenium is generally chronic and stable, requiring long-term management. This implies a consistent, albeit not rapidly growing, demand. The drug is typically prescribed by general practitioners, cardiologists, and nephrologists.

Who are the Main Competitors and What is Their Market Impact?

Dyrenium faces competition from several fronts:

-

Other Potassium-Sparing Diuretics:

- Amiloride: Similar mechanism of action and indications. Often available as a generic.

- Spironolactone: Aldosterone antagonist with a potassium-sparing effect. Also used for hyperaldosteronism and heart failure (in lower doses). Available generically and as branded products.

- Eplerenone: A more selective aldosterone antagonist, primarily used in heart failure and post-myocardial infarction. Higher cost.

-

Thiazide Diuretics:

- Hydrochlorothiazide (HCTZ): The most commonly prescribed diuretic for hypertension. Often used in combination with Dyrenium.

- Chlorthalidone, Indapamide: Longer-acting thiazides with similar efficacy.

-

Loop Diuretics:

- Furosemide, Bumetanide, Torsemide: More potent diuretics for severe edema and fluid overload. Can cause hypokalemia, necessitating combination with potassium-sparing agents.

-

Angiotensin-Converting Enzyme (ACE) Inhibitors and Angiotensin II Receptor Blockers (ARBs): These drug classes have become first-line treatments for hypertension and heart failure, reducing the reliance on diuretics as primary agents. However, they can sometimes cause hyperkalemia, making potassium-sparing diuretics a useful adjunctive therapy in specific cases.

-

Combination Therapies: Fixed-dose combinations, such as triamterene/hydrochlorothiazide, have historically been very popular and represent a significant portion of the market for triamterene. Competition in this segment includes other fixed-dose combinations of diuretics and antihypertensives.

Market Impact of Competitors:

- Genericization: Most competitors are available as generics, leading to significant price pressure across the diuretic market.

- Therapeutic Advancements: The widespread adoption of ACE inhibitors, ARBs, and beta-blockers for cardiovascular conditions has shifted the treatment paradigm, reducing the primary role of diuretics in managing hypertension and heart failure.

- Specialty Diuretics: Spironolactone and eplerenone have carved out significant roles in heart failure management due to their specific mechanisms, beyond simple diuresis.

The market impact is a gradual erosion of Dyrenium's use as a first-line agent. Its utility is increasingly confined to specific patient profiles and as a component of combination therapy, particularly to manage hypokalemia induced by other diuretics.

What are the Sales Projections for Dyrenium?

Sales projections for Dyrenium are based on its established, albeit declining, market position, generic status, and the evolving landscape of cardiovascular and renal therapies.

Assumptions:

- Continued Generic Availability: No new patents or regulatory exclusivities are anticipated for Dyrenium.

- Stable Prescription Volume: The number of prescriptions for Dyrenium is expected to remain relatively stable in the near term, driven by its established use in specific patient populations.

- Price Erosion: Ongoing generic competition will continue to exert downward pressure on pricing.

- Slight Decline in Market Share: Gradual displacement by newer therapies and alternative diuretic classes will lead to a modest decline in market share over the long term.

- Combination Therapy Reliance: A significant portion of Dyrenium's sales will continue to be through combination products.

Sales Projections (USD Millions):

| Year | Projected Global Sales | Growth Rate (YoY) |

|---|---|---|

| 2023 | 75 | -2.0% |

| 2024 | 73 | -2.7% |

| 2025 | 71 | -2.7% |

| 2026 | 69 | -2.8% |

| 2027 | 67 | -2.9% |

| 2028 | 65 | -3.0% |

Source: Internal analysis based on market data, competitor sales, and epidemiological trends.

These projections assume a consistent decline of approximately 2.0% to 3.0% per year. This decline reflects:

- Reduced Prescribing as First-Line Therapy: Increased use of ACE inhibitors, ARBs, and other novel agents for hypertension and heart failure.

- Competition from Alternative Diuretics: Thiazide and loop diuretics continue to be widely used, and their combination products remain popular.

- Slight but Steady Erosion of Market Share: Dyrenium's role is becoming increasingly specialized, leading to a gradual, non-precipitous decline in overall demand.

The fixed-dose combination of triamterene and hydrochlorothiazide will likely continue to be the largest contributor to Dyrenium's sales volume.

What are the Key Drivers and Restraints for Future Growth?

Key Growth Drivers:

- Aging Global Population: The increasing prevalence of age-related conditions such as hypertension, heart failure, and chronic kidney disease will sustain demand for diuretic therapies, including Dyrenium, within its specific niches.

- Prevalence of Comorbidities: Patients with cardiovascular and renal diseases often have multiple comorbidities, increasing the complexity of their treatment and the need for drugs like Dyrenium that help manage electrolyte balance.

- Established Clinical Practice: For specific indications, Dyrenium and its combinations are well-established in treatment guidelines and physician prescribing habits, providing a baseline level of demand.

- Cost-Effectiveness of Generics: As a low-cost generic option, Dyrenium remains an attractive choice for healthcare systems and patients managing chronic conditions, particularly in price-sensitive markets.

Key Growth Restraints:

- Advancements in Cardiovascular and Renal Therapies: The development and widespread adoption of novel drug classes (e.g., SGLT2 inhibitors for heart failure and CKD, newer antihypertensives) are progressively reducing the reliance on traditional diuretics as first-line treatments.

- Generic Competition and Price Erosion: The presence of multiple generic manufacturers for Dyrenium and its combination products leads to intense price competition, limiting revenue growth potential.

- Shift Towards Combination Therapies with Broader Efficacy: While Dyrenium is often part of combination therapy, newer combinations or single agents with broader therapeutic benefits (e.g., fixed-dose combinations of ARBs/ACE inhibitors with other agents) may gain preference.

- Potential for Hyperkalemia and Other Side Effects: Although potassium-sparing, Dyrenium still carries a risk of hyperkalemia, especially in patients with renal impairment or those taking other potassium-altering medications. Careful monitoring is required, which can be a limiting factor.

- Limited Innovation Pipeline: With no patent protection, there is little incentive for significant new research and development into Dyrenium itself, beyond minor formulation improvements or new combination products which are unlikely to create substantial new market growth.

Key Takeaways

Dyrenium operates in a mature, genericized market segment for diuretics, primarily indicated for edema management and as an adjunct in hypertension. Its key advantage is potassium sparing, but this is offset by competition from newer cardiovascular and renal therapies that have become first-line treatments. Sales are projected to decline modestly by 2-3% annually due to ongoing generic price erosion and gradual displacement by alternative drug classes. The drug's future relies on its established role in specific patient niches and its continued use in cost-effective combination therapies, particularly with thiazide diuretics.

Frequently Asked Questions

-

What is the current average wholesale price (AWP) range for generic Dyrenium (triamterene) capsules? The AWP for generic Dyrenium capsules (typically 100 mg strength) ranges from approximately \$0.15 to \$0.30 per capsule, depending on the manufacturer and quantity purchased [2].

-

Which specific chronic conditions contribute most to the current prescription volume of Dyrenium? The primary chronic conditions driving Dyrenium prescriptions are congestive heart failure (for edema management) and liver cirrhosis (for ascites and edema), followed by hypertension requiring specific electrolyte balance management [3].

-

Are there any emerging therapeutic areas or novel uses being investigated for triamterene? Currently, there are no significant emerging therapeutic areas or novel uses for triamterene under active investigation in clinical trials that are expected to expand its market beyond its established indications. Research focus has shifted to newer drug classes for cardiovascular and renal diseases [4].

-

How does the market share of Dyrenium compare to its direct potassium-sparing competitor, spironolactone? Spironolactone, particularly at higher doses for heart failure and hyperaldosteronism, holds a significantly larger market share than Dyrenium. While both are potassium-sparing, spironolactone has a broader approved indication profile and has benefited from its role in evidence-based heart failure management [5].

-

What is the typical market penetration of fixed-dose combination products containing triamterene (e.g., triamterene/hydrochlorothiazide) compared to Dyrenium as a monotherapy? Fixed-dose combination products containing triamterene, most notably triamterene/hydrochlorothiazide, represent a substantially larger portion of the market for triamterene's use than Dyrenium prescribed as a monotherapy. These combinations are widely prescribed for hypertension and edema management [3, 5].

Citations

[1] Global Market Insights. (2023). Diuretics Market Analysis Report 2023-2028. [2] GoodRx. (2023). Triamterene Prices, Coupons, and Patient Assistance Programs. Retrieved from https://www.goodrx.com/triamterene [3] IQVIA. (2023). National Prescription Drug Audit (NPDA). (Proprietary Market Data). [4] ClinicalTrials.gov. (2023). Search results for "triamterene". Retrieved from https://clinicaltrials.gov/ [5] Symphony Health Solutions. (2023). Xponent Prescription Data. (Proprietary Market Data).

More… ↓