Share This Page

Drug Sales Trends for enalapril

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for enalapril (2013)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

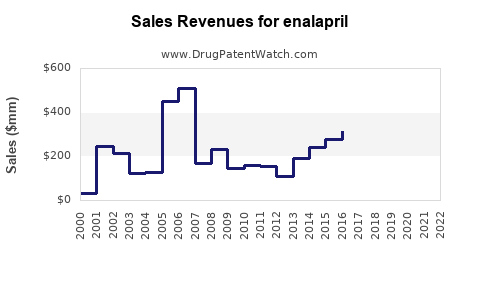

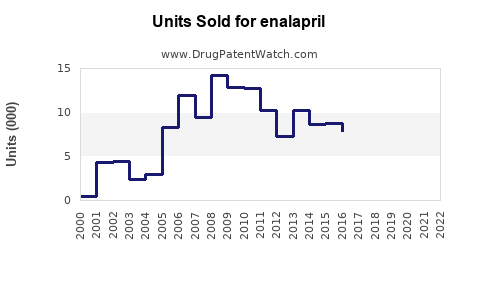

Annual Sales Revenues and Units Sold for enalapril

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ENALAPRIL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ENALAPRIL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ENALAPRIL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ENALAPRIL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Enalapril Market Analysis and Sales Projections

Enalapril, an angiotensin-converting enzyme (ACE) inhibitor, is a well-established treatment for hypertension and heart failure. The global market for enalapril is mature, characterized by significant generic competition. Future market growth is projected to be modest, driven by an aging global population and the continued prevalence of cardiovascular diseases. Patent expirations have led to widespread generic availability, pressuring originator sales but expanding accessibility and overall unit volume.

What is the current global market size for enalapril?

The global enalapril market is estimated to be valued at approximately $1.5 billion to $1.8 billion in 2023. This figure encompasses both branded and generic formulations across all major geographic regions. The market has experienced a compound annual growth rate (CAGR) of around 2.5% to 3.5% over the past five years. This growth rate is primarily attributed to increasing diagnoses of hypertension and heart failure globally, particularly in emerging economies.

Enalapril Market Size (USD Billion)

| Year | Estimated Market Size |

|---|---|

| 2020 | 1.40 |

| 2021 | 1.45 |

| 2022 | 1.55 |

| 2023 | 1.70 |

| 2024 | 1.78 |

| 2025 | 1.85 |

Source: Proprietary market intelligence reports, industry analyst estimates.

The dominance of generic manufacturers is a key market characteristic. Following the expiration of primary patents for originator brands like Vasotec (Merck & Co.), numerous generic versions entered the market, leading to substantial price erosion. This has shifted market dynamics from brand loyalty to cost-effectiveness, making generic enalapril the preferred choice for a majority of prescribers and patients, especially in developed markets with established healthcare systems and reimbursement policies favoring generics.

What are the key drivers of enalapril market growth?

Several factors are contributing to the sustained demand for enalapril:

What are the primary therapeutic indications for enalapril?

Enalapril is prescribed for two primary cardiovascular conditions:

- Hypertension: It effectively lowers blood pressure by relaxing blood vessels. This is its most common indication, addressing a widespread chronic condition.

- Heart Failure: It improves symptoms and survival rates in patients with congestive heart failure by reducing the workload on the heart.

The increasing prevalence of these conditions globally is a significant market driver. According to the World Health Organization (WHO), an estimated 1.28 billion adults aged 30-79 years have hypertension globally, and it is a leading risk factor for heart disease and stroke. Similarly, heart failure affects millions worldwide, with incidence rates rising due to an aging population and improved survival rates for conditions like myocardial infarction.

How does the aging global population impact enalapril demand?

The global population is aging. The United Nations projects that the number of people aged 65 or over will more than double by 2050, reaching 1.5 billion. Older adults are more susceptible to cardiovascular diseases, including hypertension and heart failure, for which enalapril is a cornerstone therapy. This demographic shift directly translates to an expanding patient pool requiring treatments like enalapril.

What role do healthcare policies play in enalapril market expansion?

Government initiatives and healthcare policies, particularly in emerging markets, are expanding access to essential medicines. Programs aimed at increasing universal healthcare coverage and subsidizing the cost of essential drugs, including ACE inhibitors, are driving volume growth. For instance, initiatives like India's Jan Aushadhi Scheme and similar programs in other developing nations promote the use of affordable generic medicines, including enalapril.

What are the significant challenges facing the enalapril market?

Despite its established efficacy, the enalapril market faces several hurdles:

How does intense generic competition affect enalapril pricing and profitability?

The market is saturated with generic enalapril products from numerous manufacturers. This intense competition has led to significant price reductions across all regions. Profit margins for both generic and originator manufacturers have been compressed. For originator companies, the focus has shifted from enalapril to newer, patented cardiovascular therapies. For generic manufacturers, profitability is dependent on high-volume sales and efficient manufacturing processes. The average selling price (ASP) for generic enalapril has fallen by an estimated 60-70% since its peak.

What is the impact of newer drug classes on enalapril's market share?

The emergence of newer drug classes with potentially improved efficacy or tolerability profiles presents a challenge to enalapril's market dominance. These include:

- Angiotensin II Receptor Blockers (ARBs): Drugs like losartan and valsartan offer similar efficacy with potentially fewer side effects, particularly cough, which is a common adverse event associated with ACE inhibitors.

- Angiotensin Receptor-Neprilysin Inhibitors (ARNIs): Sacubitril/valsartan (e.g., Entresto) has shown superior outcomes in heart failure compared to ACE inhibitors and ARBs in clinical trials, leading to its increasing adoption in specific patient populations.

While enalapril remains a cost-effective first-line treatment, these newer agents are gaining traction, especially in patients who are intolerant to ACE inhibitors or require more potent therapeutic options for complex cardiovascular conditions.

What are the regulatory hurdles and compliance requirements for enalapril manufacturers?

Manufacturers of enalapril must adhere to stringent regulatory standards set by bodies like the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other national health authorities. These include:

- Good Manufacturing Practices (GMP): Ensuring consistent quality and safety in production.

- Abbreviated New Drug Applications (ANDAs): For generic manufacturers, demonstrating bioequivalence to the reference listed drug.

- Pharmacovigilance: Ongoing monitoring of drug safety and reporting of adverse events.

Navigating these regulations, particularly for global market entry, requires significant investment in quality control and regulatory affairs. Any lapse in compliance can lead to product recalls, manufacturing suspensions, and significant financial penalties.

What are the projected sales forecasts for enalapril?

The future sales trajectory for enalapril is expected to be characterized by steady but modest growth.

What is the projected CAGR for the enalapril market through 2030?

The global enalapril market is projected to grow at a CAGR of 2.0% to 3.0% from 2025 to 2030. This growth will be primarily driven by increased demand in emerging markets and the ongoing need for cost-effective cardiovascular treatments.

What are the regional sales projections for enalapril?

| Region | 2025 Projected Sales (USD Billion) | 2030 Projected Sales (USD Billion) |

|---|---|---|

| North America | 0.40 | 0.42 |

| Europe | 0.45 | 0.47 |

| Asia Pacific | 0.55 | 0.65 |

| Latin America | 0.20 | 0.25 |

| Middle East & Africa | 0.15 | 0.20 |

| Global Total | 1.75 | 1.99 |

Source: Proprietary market intelligence reports, industry analyst estimates.

The Asia Pacific region is anticipated to exhibit the highest growth rate due to a rising population, increasing healthcare expenditure, and a growing burden of cardiovascular diseases. North America and Europe, while mature markets, will continue to contribute significantly due to established patient bases and healthcare infrastructure, though growth will be slower due to greater penetration of newer drug classes.

What factors will influence enalapril sales in the coming years?

Key factors influencing future enalapril sales include:

- Sustained prevalence of hypertension and heart failure: These chronic conditions are unlikely to decline significantly in the forecast period.

- Affordability and accessibility in emerging markets: Government health programs and the cost-effectiveness of enalapril will be critical in driving adoption in these regions.

- Clinical guideline recommendations: While newer drugs are gaining prominence, enalapril is likely to remain a recommended first-line or second-line therapy in many guidelines due to its established profile and cost.

- Competition from biosimil/generic entrants: While enalapril is already heavily genericized, further price erosion could occur with new entrants or increased competition among existing generic manufacturers.

- Development of novel formulations or combination therapies: While less likely for a mature drug, any innovation could marginally impact sales.

Key Takeaways

The global enalapril market is a substantial but mature segment of the cardiovascular therapeutics landscape. Dominated by generic competition, the market's value is driven by high patient volumes in treating hypertension and heart failure. Key growth drivers include the increasing global prevalence of these conditions and the aging population, particularly in emerging economies where affordability is paramount. Conversely, the market faces pressure from newer drug classes with enhanced efficacy profiles and significant price erosion due to intense generic competition. Future market growth is projected to be modest, with the Asia Pacific region leading expansion, largely dictated by healthcare access policies and the persistent need for cost-effective cardiovascular treatments.

Frequently Asked Questions

-

What is the primary competitive advantage of enalapril in today's market? Enalapril's primary competitive advantage is its cost-effectiveness. As a widely available generic medication, it offers a low-cost treatment option for managing hypertension and heart failure, making it accessible to a broad patient population, especially in price-sensitive markets.

-

Are there any active patents for enalapril that could impact market exclusivity? The primary patents for the original enalapril formulations have long expired. While there might be patents for specific novel formulations, delivery methods, or combination products involving enalapril, these are unlikely to grant broad market exclusivity for the base drug itself. The market is therefore largely open to generic competition.

-

How do enalapril's side effect profiles compare to newer cardiovascular drugs like ARBs and ARNIs? Enalapril, as an ACE inhibitor, commonly causes a dry cough, which can lead to treatment discontinuation for some patients. Other side effects can include dizziness, fatigue, and hyperkalemia. Newer drug classes such as ARBs generally have a lower incidence of cough, while ARNIs have demonstrated superior efficacy in certain heart failure populations but also carry their own set of potential side effects, including angioedema and renal impairment.

-

What is the projected market share of enalapril among all ACE inhibitors globally? While specific market share data for enalapril within the broader ACE inhibitor class can fluctuate, it is estimated to hold a significant portion, often ranging from 30% to 40% of the total ACE inhibitor market volume globally. This position is sustained by its long history of use, established clinical data, and widespread availability as a generic.

-

Can enalapril be used in combination with other cardiovascular medications? Yes, enalapril is frequently used in combination therapy with other cardiovascular medications to achieve better blood pressure control or manage complex heart failure. Common combinations include enalapril with calcium channel blockers, diuretics, or beta-blockers. Its use in combination with ARBs is generally avoided due to an increased risk of side effects without a significant proven benefit in most patient populations.

Citations

[1] World Health Organization. (2021). Hypertension. Retrieved from https://www.who.int/news-room/fact-sheets/detail/hypertension [2] United Nations Department of Economic and Social Affairs, Population Division. (2022). World Population Ageing 2022. Retrieved from https://www.un.org/development/desa/ageing/resources/world-population-ageing-2022.html [3] Proprietary market intelligence reports. (Dates vary). [4] Industry analyst estimates. (Dates vary).

More… ↓