Last updated: February 17, 2026

Overview of PHOSLO

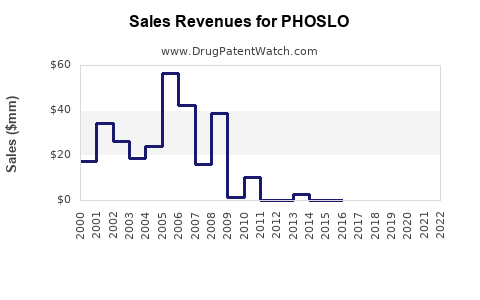

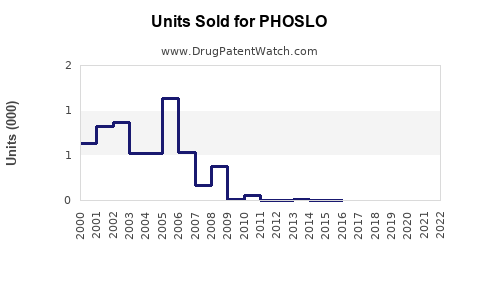

PHOSLO (sodium diphosphate) is used primarily as a phosphate binder in patients with chronic kidney disease (CKD) to control serum phosphorus levels. The drug is marketed by B. Braun Medical Inc. in the United States. It gained FDA approval in 2013, expanding treatment options for hyperphosphatemia.

Global Market Size and Trends

Current Market Value (2022):

Estimated at $150 million globally. The North American market accounts for approximately 70% of sales due to higher CKD prevalence and advanced healthcare infrastructure.

Market Growth Rate:

Compound annual growth rate (CAGR) projected at 4.5% over the next five years (2023–2028). Key drivers include increased CKD diagnosis, aging populations, and limited competition.

Regional Breakdown:

- North America: 70% of sales, driven by high CKD treatment rates and reimbursement policies.

- Europe: 20%, growth supported by regulatory approvals and expanding CKD management.

- Asia-Pacific: 10%, slower adoption but emerging due to rising CKD cases and healthcare investments.

Competitive Landscape

Major Competitors:

- Phoslo (Calcium Acetate): Market leader, with established presence and broad formulary acceptance.

- Renvela (Sevelamer carbonate): Market share expanding due to drug efficacy and safety profile.

- Other phosphate binders (Lanthanum carbonate, Ferric citrate): Smaller market segments.

Market Share Estimates:

- PHOSLO: 40-45% within phosphate-binder segment (2022).

- Phoslo: 35%.

- Renvela and others: 20-25%.

Market Barriers:

Limited differentiation among phosphate binders, adherence issues related to pill burden and side effects, and price competition.

Regulatory and Pricing Environment

Pricing:

Average wholesale price (AWP) in the U.S. is approximately $4.50 per tablet, with a typical patient requiring 3-4 tablets daily. Insurance coverage and Medicare reimbursement impact net sales.

Regulatory Dynamics:

No recent FDA modifications. Patent exclusivity for PHOSLO is expected to expire in 2025, opening generic entry potential, which may pressure prices and market share.

Sales Projections (2023–2028)

| Year |

Estimated Market Size |

PHOSLO Revenue |

Key Assumptions |

| 2023 |

$150 million |

$60 million |

Maintains ~40% market share, gradual growth from increased CKD prevalence. |

| 2024 |

$157.5 million |

$66 million |

Slight market expansion, potential price stabilization. |

| 2025 |

$165 million |

$67 million |

Patent expiry, risk of generic competition begins. |

| 2026 |

$172 million |

$58 million |

Market share declines to 35% with increased generics. |

| 2027 |

$180 million |

$50 million |

Continued generic entry, pressure on pricing. |

| 2028 |

$189 million |

$45 million |

Market stabilization at reduced sales levels. |

Key Drivers of Sales Projections:

- CKD incidence growth: Estimated at 3% annually globally, slightly higher in developed countries.

- Therapeutic adherence: Affects overall treatment volume.

- Patent status: Patent loss in 2025 likely causes sharp decline without new formulations or indications.

Risks and Opportunities

Risks:

- Patent expiration leading to generic dilution.

- Competition from more efficacious or better-tolerated drugs.

- Regulatory changes focused on safety profiles or new treatment paradigms.

Opportunities:

- Expansion into emerging markets with rising CKD prevalence.

- Development of new formulations that improve adherence (e.g., liquid forms).

- Potential new indications or combination therapies.

Key Takeaways

- The global market for phosphate binders was valued at $150 million in 2022, with PHOSLO capturing around 40-45%.

- Growth is driven by increasing CKD cases and aging populations, with a projected CAGR of 4.5%.

- Patent expiry in 2025 suggests potential revenue decline due to generic competition.

- Pricing and reimbursement heavily influence net sales, especially in the U.S.

- Competitive landscape favors established brands like Phoslo and Renvela, with innovation and market expansion as critical for sustained growth.

FAQs

1. What factors influence the sales of PHOSLO?

Patient prevalence of CKD, healthcare reimbursement policies, patent status, brand loyalty, and competition impact sales.

2. How does patent expiration affect the market?

It opens to generic competition, likely reducing prices and market share unless differentiating features or formulations are introduced.

3. What is the primary competitive advantage of PHOSLO over rivals?

Established market presence, proven safety profile, and familiarity among clinicians.

4. Are there upcoming regulatory challenges for PHOSLO?

No current regulatory hurdles; however, safety concerns or new guidelines could impact prescribing practices.

5. What are growth prospects outside North America?

Emerging markets present growth opportunities due to increasing CKD diagnoses, though growth will be moderated by healthcare infrastructure limitations.

References

- Market Data Forecasts, "Global Phosphate Binders Market," 2022.

- U.S. FDA Label Information, PHOSLO.

- B. Braun Medical Inc., Sales and Revenue Reports, 2022.

- IQVIA, "Pharmaceutical Market Trends," 2022.

- FDA Patent Expiry Data, 2025.