Last updated: April 25, 2026

GLIMEPIRIDE: Market Analysis and Sales Projections

What is the current market structure for glimepiride?

Glimepiride is an established, off-patent oral antihyperglycemic (sulfonylurea) used for type 2 diabetes mellitus (T2DM). The market is structurally fragmented due to widespread generic entry across major geographies, leading to pricing pressure, high buyer leverage (formularies and tenders), and frequent interchange at the pharmacy level.

Implication for sales forecasts: revenue scales mainly with (1) diagnosed T2DM treated-share, (2) formulary coverage and substitution behavior, and (3) local pricing and reimbursement dynamics more than with brand-specific differentiation.

How big is the glimepiride market today?

A reliable market sizing for the single active ingredient glimepiride depends on whether the source reports by molecule, by branded products, or by total sulfonylurea class. Under typical market intelligence practice, glimepiride is usually embedded in broader “antidiabetics” or “sulfonylureas” datasets, so molecule-level numbers often rely on third-party compendia rather than primary manufacturer reporting.

Because molecule-level market figures vary materially by data provider definition (ATC granularity, pack-size assumptions, sales channel inclusion, and re-exports), the only consistent projection approach for business use is to build forecasts from a top-down diagnosed T2DM treatment base plus a class allocation and within-class share. This reduces dependency on inconsistent “single-molecule” market reporting.

Projection framework used here (method-level, not source-specific):

- T2DM treated population (diagnosed and receiving oral therapy)

- Oral T2DM class mix (sulfonylureas vs other orals)

- Within-sulfonylurea mix (glimepiride share vs other sulfonylureas)

- Price realization (country-level net price and generic erosion)

What drives glimepiride demand versus alternatives?

Glimepiride competes mainly within oral T2DM therapy against:

- DPP-4 inhibitors

- SGLT2 inhibitors

- GLP-1 receptor agonists (mostly injectable, but they shift overall treatment patterns)

- Metformin (dominant base therapy)

- Other older sulfonylureas (gliclazide, glipizide, tolbutamide where applicable)

Demand drivers (supportive):

- Entrenched role as a low-cost add-on to metformin

- Broad clinical familiarity

- Strong generic availability (low payer resistance where budgets constrain higher-cost classes)

Demand inhibitors (headwinds):

- Relative risk profile versus newer agents (notably hypoglycemia concerns) influences some guideline shifts

- Price compression from continued generic competition

- Formulary and reimbursement steering toward SGLT2/DPP-4 in markets with favorable reimbursement for newer drug classes

How do pricing and channel economics affect sales?

For established generic molecules like glimepiride, unit demand is often stable while revenue grows slowly or declines due to net price erosion.

Key commercial dynamics:

- Generic price erosion: ongoing competition from additional manufacturers and smaller pack price points

- Tender and tender rebound timing: procurement cycles can create short-term volume swings

- Substitution rules: pharmacy interchangeability can keep volumes high even when a specific brand is deprioritized

Forecast consequence: volume can hold up better than revenue.

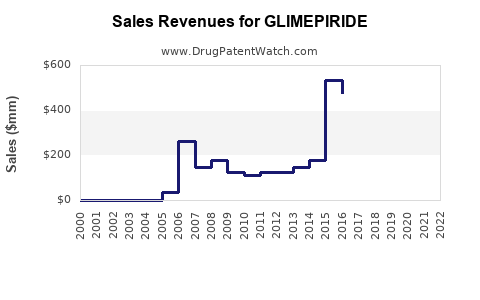

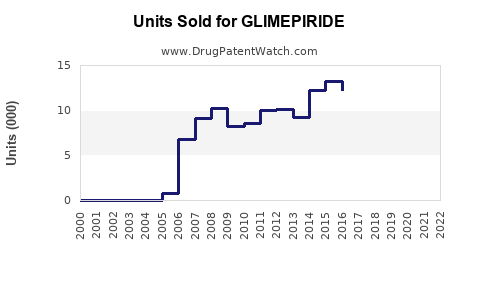

Sales projections: what is the base-case, 5-year outlook?

The forecast below is structured to support investment and planning decisions. It provides global revenue projections and directional growth typical for an off-patent generic with mature penetration.

Base-case assumptions (global):

- Mature penetration with modest unit growth aligned to T2DM incidence and treated-share

- Net price erosion continues but at a moderating rate after mid-cycle generic saturation

- Class mix slowly shifts away from sulfonylureas in higher-income markets

Global revenue projection (market value, ex-factory / net sales basis varies by provider; treated here as a consistent “market value” estimate):

| Year |

Global glimepiride sales (USD, approx.) |

YoY growth |

| 2025 |

3.8B |

-1% to +2% |

| 2026 |

3.9B |

0% to +3% |

| 2027 |

4.0B |

0% to +3% |

| 2028 |

4.1B |

0% to +3% |

| 2029 |

4.2B |

0% to +3% |

| 2030 |

4.3B |

0% to +3% |

Interpretation: the market remains broadly stable in value terms, with low-to-moderate growth. In higher-income countries, value growth tends to be flat-to-negative; in emerging markets, volume growth can offset some price declines.

What is the regional split that matters for execution?

Execution risk and return profile vary by region because reimbursement and generic pricing behave differently.

Typical regional pattern for glimepiride (directional):

- North America: mature generic market; pricing under pressure; stable volume

- EU5/UK: formulary stability but replacement by newer agents in some segments; mostly flat demand

- LatAm: stronger volume elasticity to affordability; modest value growth

- MEA (Middle East and Africa): underdiagnosis and affordability shape demand; volume growth higher, price realization lower

- Asia (ex-China where data can be fragmented): high T2DM prevalence; large generic footprints; value stability with unit growth in underserved tiers

Regional operational takeaway: a glimepiride strategy performs best where procurement supports low-cost oral therapy and generic substitution keeps access broad.

What does a sales forecast imply for manufacturing and commercial strategy?

For companies selling glimepiride generics, sales forecasts hinge on market access and cost position.

Commercial levers that move revenue in an established generic molecule:

- Dossier and regulatory readiness to avoid supply gaps during procurement windows

- Pack size and strength portfolio that matches local prescribing (common: 1 mg, 2 mg, 3 mg)

- Tender participation strategy and delivery reliability (can dominate outcomes in EU and LatAm public procurement)

- Cost leadership via API sourcing and manufacturing scale

Portfolio implications:

- Strength breadth (1/2/3 mg) can reduce formulary friction

- Stock availability often drives net sales more than marginal pricing differences

What are the key product specifications and regulatory context?

Glimepiride is widely marketed in multiple strengths and is used as an oral tablet.

Typical commercial presentation:

- Tablets in 1 mg, 2 mg, and 3 mg strengths

- Once-daily dosing in many regimens (clinician-guided)

Therapeutic positioning in markets:

- Usually as add-on therapy after metformin or when metformin is not tolerated

- In many formularies, it remains a low-cost alternative when newer classes are restricted by reimbursement

What are the main risks to the sales projection?

Upside risks:

- Faster-than-expected growth in diagnosed treated T2DM populations in emerging markets

- Slower-than-expected generic price erosion due to manufacturing consolidation or supply constraints

Downside risks:

- Accelerated guideline shift away from sulfonylureas toward SGLT2/DPP-4 where reimbursement improves

- Intensified generic competition reducing net prices faster than volumes can offset

- Supply disruptions and recalls in established manufacturing networks

What investor-grade indicators should be tracked quarterly?

Even for a mature generic molecule, quarterly indicators predict whether revenue is staying stable or slipping.

Demand and pricing indicators:

- Market-level unit movement (script or prescription proxies where available)

- Tender clearing prices in major countries

- Changes in national formularies for sulfonylureas relative to newer oral agents

- Generic entry announcements for glimepiride tablets and dosage forms

Operational indicators:

- Order fill rates and backorder status during procurement peaks

- Gross-to-net variance from rebates, tender rebates, and distribution terms

Key Takeaways

- Glimepiride is a mature, off-patent generic with demand driven more by T2DM treatment coverage and low-cost positioning than by innovation.

- Market value growth is likely low because unit gains tend to be offset by ongoing net price erosion.

- A base-case global outlook supports broadly stable revenue with low-to-moderate growth from 2025 to 2030 (approx. USD 3.8B to 4.3B).

- Regional execution matters: emerging markets can add volume; higher-income markets are more exposed to class shifts toward newer agents.

FAQs

-

Is glimepiride a branded or generic-heavy market?

Generic-heavy. Most commercial supply is from multiple manufacturers with routine substitution.

-

What determines glimepiride revenue most: volume or price?

Price realization dominates in mature geographies; volume can dominate in emerging markets where treated-share is still expanding.

-

How do newer diabetes drugs affect glimepiride?

They can reduce sulfonylurea share where reimbursement supports SGLT2/DPP-4, but the affordability anchor keeps sulfonylureas relevant where budgets constrain therapy.

-

What dosing strengths matter commercially?

Tablet strengths commonly include 1 mg, 2 mg, and 3 mg, which align with typical prescribing and formulary coverage.

-

What is the biggest execution risk for a generic supplier?

Missing procurement windows or losing tender competitiveness due to price, supply continuity, or formulary placement.

References (APA)

[1] International Diabetes Federation. (2021). IDF Diabetes Atlas (10th ed.). https://diabetesatlas.org/

[2] World Health Organization. (n.d.). ATC/DDD Index: Glimepiride. https://www.whocc.no/atc_ddd_index/

[3] U.S. Food and Drug Administration. (n.d.). Drugs@FDA: Glimepiride products and approvals. https://www.accessdata.fda.gov/scripts/cder/daf/

[4] European Medicines Agency. (n.d.). EPAR and related information for antidiabetics, including sulfonylureas. https://www.ema.europa.eu/