Share This Page

Drug Sales Trends for GEMFIBROZIL

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for GEMFIBROZIL (2013)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

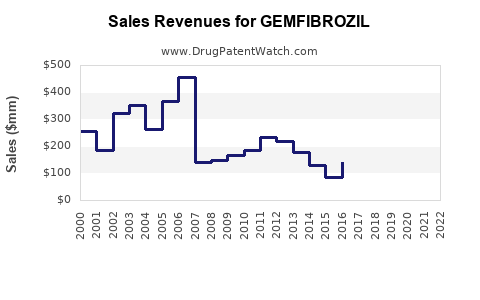

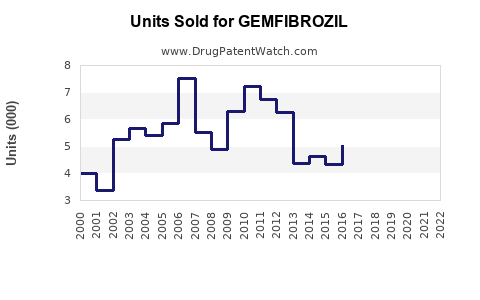

Annual Sales Revenues and Units Sold for GEMFIBROZIL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| GEMFIBROZIL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| GEMFIBROZIL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| GEMFIBROZIL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

GEMFIBROZIL (GEM): Market Analysis and Sales Projections

Gemfibrozil is a fibrate medication used to lower cholesterol and triglyceride levels in the blood. It is primarily prescribed for patients with hypertriglyceridemia, as well as for those with low high-density lipoprotein (HDL) cholesterol and high low-density lipoprotein (LDL) cholesterol.

What is the current market status of Gemfibrozil?

The market for Gemfibrozil is characterized by its generic status, with numerous manufacturers offering the drug. This has led to significant price competition and a mature market. The primary driver for its continued use is its established efficacy and cost-effectiveness in managing dyslipidemia, particularly for patients who do not respond adequately to statins or require combination therapy.

Key Market Characteristics:

- Generic Dominance: Gemfibrozil has been off-patent for an extended period, leading to widespread generic availability. This has suppressed prices and limited opportunities for significant revenue growth for any single manufacturer.

- Established Therapeutic Use: The drug remains a recognized treatment option for hypertriglyceridemia and mixed dyslipidemia, especially in cases where other lipid-lowering agents are contraindicated or insufficient.

- Price Sensitivity: Due to generic competition, the market is highly price-sensitive. Procurement decisions by healthcare systems and pharmacies are often based on the lowest available price.

- Statin Competition: While Gemfibrozil addresses specific lipid profiles, the widespread use and efficacy of statins for primary and secondary prevention of cardiovascular disease represent a significant competitive force. However, Gemfibrozil occupies a niche for specific dyslipidemia types.

- Regulatory Landscape: Generic drug approvals are primarily focused on bioequivalence, meaning new entrants face a lower barrier to market entry provided they meet stringent quality standards.

Market Size and Trends:

The global market for Gemfibrozil is a subset of the broader dyslipidemia market. Precise, up-to-date figures for Gemfibrozil alone are difficult to isolate due to its generic nature and inclusion in broader lipid-lowering drug market analyses. However, industry estimates suggest a modest but stable market size.

- Estimated Global Market Value (Gemfibrozil Segment): While difficult to pinpoint precisely due to generic fragmentation, the global market for Gemfibrozil as a standalone product is estimated to be in the low hundreds of millions of U.S. dollars annually. This figure is largely driven by volume rather than high price points.

- Growth Trajectory: The market is projected to experience minimal to no significant growth in terms of value. Volume may see slight fluctuations based on healthcare policy changes, formulary inclusions, and the emergence of new therapeutic guidelines. Any growth is likely to be incremental and offset by price erosion.

- Regional Variations: The U.S. and European markets represent significant demand centers due to established healthcare infrastructure and prevalence of cardiovascular risk factors. Emerging markets may see modest increases in demand as access to healthcare and lipid-lowering therapies improve.

What are the key therapeutic indications and competitive landscape for Gemfibrozil?

Gemfibrozil's therapeutic utility is well-defined, primarily targeting elevated triglyceride levels. Its competitive positioning is influenced by the availability of alternative lipid-lowering agents and evolving clinical guidelines.

Primary Indications:

- Hypertriglyceridemia: Gemfibrozil is indicated for the treatment of very high serum triglyceride levels (e.g., greater than 500 mg/dL or 5.65 mmol/L) that are associated with an increased risk of pancreatitis. This is its most robust indication.

- Mixed Dyslipidemia: It is also used to treat patients with low HDL cholesterol and high LDL cholesterol, particularly when statins alone are insufficient or not tolerated.

Comparative Efficacy and Safety:

- Against Statins: Statins are generally considered the first-line therapy for most patients with dyslipidemia due to their proven efficacy in reducing cardiovascular events and their favorable safety profile. Gemfibrozil is typically used when statins are insufficient or contraindicated.

- Against Other Fibrates: Gemfibrozil competes with other fibrates such as fenofibrate and bezafibrate. Fenofibrate is often preferred due to potentially better efficacy in raising HDL and lowering LDL, and potentially fewer drug-drug interactions compared to Gemfibrozil.

- Combination Therapies: Gemfibrozil can be used in combination with bile acid sequestrants or nicotinic acid. However, caution is advised when combining Gemfibrozil with statins due to an increased risk of myopathy and rhabdomyolysis. The FDA has issued warnings against this combination [1].

Competitive Landscape:

The competitive landscape for Gemfibrozil is saturated with generic manufacturers. Key players are typically large generic pharmaceutical companies that focus on high-volume, low-margin products.

- Major Generic Manufacturers: Companies such as Teva Pharmaceuticals, Mylan (now Viatris), Sandoz, and Apotex are significant suppliers of generic Gemfibrozil.

- Therapeutic Substitutes:

- Statins: Atorvastatin, Rosuvastatin, Simvastatin, Pravastatin, Lovastatin, Fluvastatin.

- Other Fibrates: Fenofibrate, Bezafibrate.

- PCSK9 Inhibitors: Evolocumab, Alirocumab (used for severe hypercholesterolemia not controlled by other means).

- Bile Acid Sequestrants: Cholestyramine, Colesevelam.

- Ezetimibe: A cholesterol absorption inhibitor.

- Niacin (Nicotinic Acid): Used for its effects on HDL and triglycerides.

Patent Expiry and Generic Entry:

Gemfibrozil has long been off-patent. Its original U.S. patent expired in the early 2000s. This has resulted in a mature generic market with a consistent supply from multiple sources.

What are the key challenges and opportunities for Gemfibrozil manufacturers?

The challenges facing Gemfibrozil manufacturers are primarily related to market maturity and pricing pressures. Opportunities, while limited, exist in niche markets and cost-effective supply chain management.

Challenges:

- Intense Price Competition: The generic nature of Gemfibrozil leads to aggressive price erosion. Profit margins are thin, requiring efficient manufacturing and distribution to remain viable.

- Declining Market Share Relative to Statins: As statins have become the dominant first-line therapy for many dyslipidemia types, Gemfibrozil's role has become more specialized, limiting its overall market penetration.

- Drug Interaction Risks: The known increased risk of myopathy when combined with statins necessitates careful prescribing and limits its use in certain patient populations. This has led to FDA warnings and physician caution [1].

- Emergence of Newer Therapies: While not direct competitors for its primary indications, novel therapies for hypercholesterolemia and severe dyslipidemia can influence treatment algorithms and physician preferences.

- Regulatory Scrutiny: Like all pharmaceuticals, Gemfibrozil manufacturers are subject to ongoing regulatory compliance, quality control, and potential post-market surveillance issues.

Opportunities:

- Cost-Effective Treatment for Specific Indications: For patients with severe hypertriglyceridemia where cost is a significant factor, Gemfibrozil remains a viable and affordable option. This is particularly relevant in healthcare systems with budget constraints.

- Emerging Markets: As healthcare access expands in developing economies, there is potential for increased demand for established, low-cost generic medications like Gemfibrozil.

- Supply Chain Efficiency: Manufacturers with highly efficient supply chains and low-cost production can maintain competitiveness even in a price-sensitive market.

- Combination Therapy Niches: In select cases where Gemfibrozil's specific lipid-modifying profile is beneficial and used judiciously with non-statin agents, there remains a therapeutic niche.

- Contract Manufacturing: Companies with robust manufacturing capabilities can leverage these to act as contract manufacturers for other generic or branded companies that may not have in-house production for Gemfibrozil.

Market Access and Reimbursement:

Gemfibrozil is generally well-covered by insurance plans and national health services due to its generic status and established efficacy. However, formularies may prioritize statins or other agents for initial therapy, requiring a prior authorization or specific justification for Gemfibrozil.

What are the sales projections for Gemfibrozil?

Sales projections for Gemfibrozil are characterized by stability rather than growth, reflecting its mature generic market. Growth is expected to be minimal, driven primarily by volume in specific patient segments and emerging markets.

Projected Sales Trajectory (Global):

- 2024-2025: The market is expected to remain largely stable, with minimal year-over-year value change. Slight volume increases in emerging markets may be offset by continued price erosion in developed markets.

- Estimated Global Sales Value: $250 million - $300 million USD.

- 2026-2028: Projections indicate continued stability, with growth rates unlikely to exceed 1-2% annually. Factors such as demographic shifts (aging populations with increased cardiovascular risk) could marginally increase demand. However, this will be counteracted by increasing adoption of newer lipid-lowering agents and stricter formulary controls on older medications.

- Estimated Global Sales Value: $260 million - $320 million USD.

Key Assumptions for Projections:

- No Major Expiry of Related Generic Compounds: The continued presence of numerous generic competitors will maintain price pressure.

- Continued Clinical Relevance for Specific Indications: Gemfibrozil will retain its utility for severe hypertriglyceridemia and specific mixed dyslipidemia cases not adequately managed by other therapies.

- Stable Regulatory Environment: No significant new regulatory restrictions or safety concerns are anticipated that would drastically alter its prescribing patterns.

- Absence of Major Novel Therapeutic Breakthroughs: While new lipid-lowering agents continue to emerge, their primary targets and cost profiles are often different, limiting direct substitution for Gemfibrozil's core indications.

- Healthcare Budgetary Constraints: In many regions, cost-effectiveness will continue to favor generic options for established indications.

Factors that Could Impact Projections:

- Increased Focus on Cardiovascular Prevention: Greater emphasis on primary and secondary prevention of cardiovascular disease could indirectly increase the overall dyslipidemia market, potentially benefiting all lipid-lowering agents, including Gemfibrozil, in terms of volume.

- New Clinical Guidelines: Revisions in treatment guidelines by major cardiology organizations could shift prescribing patterns, either favorably or unfavorably for Gemfibrozil.

- Emergence of Significant Drug Interactions: Discovery of previously unknown severe drug interactions could lead to restricted use.

- Manufacturing Disruptions: Global supply chain issues or quality control problems affecting major manufacturers could temporarily impact availability and pricing.

- Increased Adoption of PCSK9 Inhibitors and other Novel Agents: While more expensive, broader adoption of these agents for specific high-risk patient groups could indirectly reduce the use of older drugs like Gemfibrozil in certain complex cases.

Overall Market Outlook:

The Gemfibrozil market is a mature, price-driven segment of the cardiovascular drug landscape. Manufacturers must focus on operational efficiency, cost control, and targeted market access to maintain profitability. The market is expected to remain stable with low single-digit growth, primarily driven by volume in specific therapeutic niches and developing regions.

Key Takeaways

- Gemfibrozil operates within a mature, highly competitive generic drug market.

- Its primary indication is the treatment of severe hypertriglyceridemia, with secondary use in mixed dyslipidemia.

- Intense price competition limits revenue growth, with profitability reliant on efficient manufacturing and distribution.

- Statins remain the dominant first-line therapy for most dyslipidemia cases, positioning Gemfibrozil in more specialized therapeutic niches.

- Sales are projected to remain stable, with minimal growth anticipated through 2028, largely driven by volume in emerging markets and specific patient segments.

Frequently Asked Questions

- What is the primary mechanism of action for Gemfibrozil? Gemfibrozil belongs to the fibrate class of drugs and works by activating peroxisome proliferator-activated receptors (PPARs), primarily PPAR-alpha. This activation leads to a reduction in triglyceride synthesis and secretion by the liver and an increase in the clearance of triglyceride-rich lipoproteins. It also increases HDL cholesterol levels and may have a modest effect on lowering LDL cholesterol.

- What are the most significant safety concerns associated with Gemfibrozil? The most notable safety concern is the increased risk of myopathy, including rhabdomyolysis, particularly when Gemfibrozil is co-administered with statins. This interaction has led to warnings from regulatory bodies like the FDA. Other potential side effects include gastrointestinal disturbances, gallstones, and liver enzyme elevations.

- How does Gemfibrozil compare to fenofibrate in treating dyslipidemia? Both Gemfibrozil and fenofibrate are fibrates. Fenofibrate is generally considered to have a broader lipid-modifying profile, potentially offering greater reductions in LDL cholesterol and greater increases in HDL cholesterol compared to Gemfibrozil. Additionally, fenofibrate may have a more favorable drug interaction profile, particularly with statins, compared to Gemfibrozil, although caution is still advised.

- What is the typical patient profile for whom Gemfibrozil is prescribed? Gemfibrozil is typically prescribed for patients with severe hypertriglyceridemia (serum triglycerides > 500 mg/dL) who are at risk of pancreatitis. It is also used in patients with mixed dyslipidemia (high LDL and low HDL) who have not achieved adequate lipid control with lifestyle modifications and statins, or in whom statins are contraindicated.

- What is the impact of Gemfibrozil's generic status on its market availability and pricing? Gemfibrozil's generic status means it is available from multiple manufacturers worldwide at significantly reduced prices compared to its branded origins. This has led to widespread availability and affordability but also intense price competition among generic producers, suppressing overall market value growth.

Citations

[1] U.S. Food & Drug Administration. (2012, February 22). FDA Drug Safety Communication: FDA cautions against combining gemfibrozil (Lopid) with statins. Retrieved from https://www.fda.gov/drugs/drug-safety-and-availability/fda-drug-safety-communication-fda-cautions-against-combining-gemfibrozil-lopid-statins

More… ↓