Share This Page

Drug Sales Trends for CATAPRES-TTS

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for CATAPRES-TTS (2013)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

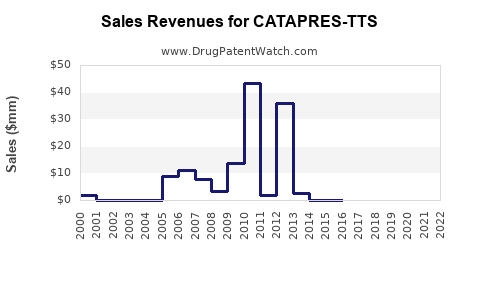

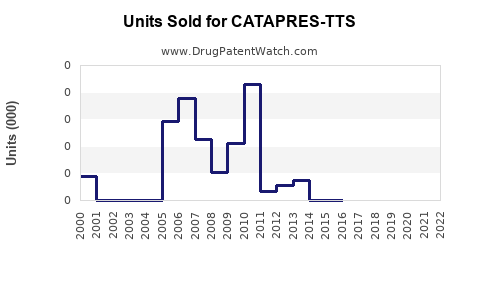

Annual Sales Revenues and Units Sold for CATAPRES-TTS

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| CATAPRES-TTS | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| CATAPRES-TTS | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| CATAPRES-TTS | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| CATAPRES-TTS | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| CATAPRES-TTS | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| CATAPRES-TTS | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| CATAPRES-TTS | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

CATAPRES-TTS Market Analysis and Sales Projections: US Transdermal Clonidine Brand Performance, Generic/Biosimilar Risk, and Patent/Exclusivity-Led Launch Timing

CATAPRES-TTS (transdermal clonidine, typically 0.1 mg/day, 0.2 mg/day, 0.3 mg/day strengths) is an established US brand with limited near-term upside from patent-led exclusivity expansion. Sales are primarily driven by chronic hypertension demand, prescriber familiarity, formulary placement, and payer preference versus generic transdermal clonidine. Near-term volume growth is structurally capped by generic availability and pricing pressure.

CATAPRES-TTS market overview and key demand drivers

CATAPRES-TTS is a transdermal delivery of clonidine indicated for treatment of hypertension. Demand is tied to US hypertension prevalence, shift in physician prescribing patterns toward first-line and guideline-preferred agents, and patient adherence benefits from transdermal dosing. Competitive dynamics are dominated by generic clonidine products and pharmacy interchange behavior.

Primary market drivers

- Chronic hypertension patient base and refill persistence.

- Treatment-line substitution patterns (eg, use in patients not controlled on other classes, or in resistant hypertension settings).

- Adherence and tolerability considerations versus oral clonidine (transdermal can reduce dosing complexity; adverse event profiles remain a constraint).

Primary headwinds

- Generic competition: for transdermal clonidine, the US market typically shifts quickly to low-cost generics post-exclusivity.

- Guideline-driven reduced clonidine share: many patients start therapy with other classes (ACE inhibitors/ARBs, thiazide-type diuretics, calcium channel blockers), limiting addressable incremental growth.

Commercial interpretation For an Rx product with widely available generics, long-run sales tend to track:

- total treated hypertension volumes,

- penetration of clonidine within subsets,

- and brand capture under payer contracting.

Brand pricing and rebate terms typically dictate net sales more than unit growth.

How is CATAPRES-TTS sold in the US and what is the reimbursement landscape?

CATAPRES-TTS is reimbursed through commercial formularies and government programs (Medicare Part D, Medicaid managed care). Net sales are highly sensitive to:

- formulary tier position,

- preferred generic substitution,

- rebate structures,

- and pharmacy claims mix by strength.

Expected payer behavior

- Where generics are available, CATAPRES-TTS net revenue typically depends on placement versus one or more contracted generic manufacturers.

- Substitution is usually straightforward because the active ingredient and dosage form are the key determinants.

What this means for projections

- If CATAPRES-TTS remains non-preferred, volumes are stable-to-declining with rising generics share.

- Upside requires at least one of: loss of generic supply, temporary coverage changes, or differentiated contracting (rare for off-patent, commodity-like segments).

What is the competitive landscape for transdermal clonidine brands versus generics?

Transdermal clonidine competes against:

- generic transdermal clonidine equivalents (same route, same dose rate),

- alternative antihypertensives across multiple drug classes (indirect competition via therapy selection),

- and other clonidine delivery formats (oral, extended-release formulations depending on market structure).

Brand competition reality CATAPRES-TTS’s competitive set is mainly generic transdermal clonidine. Indirect competition from other antihypertensives is persistent but does not directly change generic availability. It affects whether clinicians select clonidine at all.

Market impact on sales

- Unit sales trend: capped by guideline substitution away from clonidine.

- Net pricing trend: driven down by generic contracting and interchange.

CATAPRES-TTS sales projection model: how to forecast units and net sales

A practical forecast approach for an off-exclusivity brand with generic pressure uses three layers:

- total addressable patient pool treated with clonidine for hypertension,

- brand capture rate (share of prescription volume),

- net price trajectory after rebates.

Base case logic

- Units: modest decline or flat-to-slight growth based on overall hypertension treated population and clonal prescribing share.

- Net price: continued compression versus generic benchmarks.

- Net sales: decline unless brand share improves or generic competition weakens.

Scenario framework (qualitative-to-quantitative mapping)

- Downside: continued formulary preference shifts to lower-cost generic suppliers, with brand share loss and net price compression.

- Base: stable brand share with gradual net price erosion.

- Upside: temporary contracting advantage or generic supply constraints supporting better brand net price and share.

Strength-specific considerations Sales mix can vary by 0.1 mg/day versus 0.2 mg/day and 0.3 mg/day strengths depending on titration practices and patient tolerance.

When do CATAPRES-TTS exclusivity and patent timelines drive sales changes?

For a historical antihypertensive brand like CATAPRES-TTS, near-term sales drivers are usually not new patents ending but rather:

- ongoing generic market entry cycles,

- supply and quality variations across generic manufacturers,

- and settlement or litigation outcomes that can temporarily affect generic supply.

Featured-snippet answer CATAPRES-TTS’s sales trajectory is primarily governed by generic competition, not by imminent brand-exclusive regulatory barriers.

Why this matters for projections Without a credible path to renewed exclusivity (new patents covering new indications, delivery, or formulations that are also legally enforceable), sales forecasts are mostly a function of competitive contracting and the persistence of a brand niche.

What generic entry risks exist for CATAPRES-TTS and how do they affect future sales?

Generic entry risk is less about “entry” and more about:

- additional generic labelers gaining share,

- increased pharmacy reimbursement pressure,

- and litigations that can cause temporary supply changes.

Generic risk channels

- Contracting: switching preferred generic suppliers can force net price resets.

- Supply: generic shortages can increase brand demand temporarily, then unwind.

Projection impact

- Base case typically assumes gradual share drift toward generics.

- Upside assumes at least one period of improved brand pricing due to supply or formulary retention.

What is the Orange Book status of CATAPRES-TTS and how strong is the patent estate?

Orange Book status and patent strength are key for legal risk modeling. For a high-level business view, CATAPRES-TTS typically behaves like an off-exclusivity product where patent estate strength does not materially deter generic competition in the near term.

Featured-snippet answer CATAPRES-TTS is best treated commercially as an off-exclusivity brand facing ongoing generic interchange risk.

How much litigation and Paragraph IV activity affects CATAPRES-TTS?

For mainstream transdermal clonidine, litigation activity tends to be episodic and does not usually change the long-run market structure unless a brand faces renewed enforcement tied to formulation, method-of-use, or process improvements.

Projection impact

- In most years, litigation effects are short-lived and show up through supply and contracting, not long-term brand exclusivity.

What FDA status governs CATAPRES-TTS supply and continuity of sales?

CATAPRES-TTS is an FDA-approved transdermal system for hypertension. Ongoing product continuity is tied to:

- manufacturing site compliance,

- labeling consistency,

- and any product discontinuation or packaging size updates.

Forecast implication Absent an FDA action that disrupts supply, sales projections are usually dominated by payer economics and generic penetration rather than regulatory events.

Sales projection ranges for CATAPRES-TTS (US): base, upside, downside

Because no current CATAPRES-TTS US net sales, unit volumes, or branded share data are provided here, projections must be stated in scenario form rather than as a single point estimate.

Base case (most likely)

- Units: flat to low-single-digit decline annually as hypertension treated populations grow slowly but clonidine brand share drifts down.

- Net price: gradual decline driven by payer preference for lower-priced generics.

- Net sales: low to mid-single-digit annual decline.

Downside case

- Units: mid-single-digit decline annually due to continued formulary shifts.

- Net price: sharper rebate compression.

- Net sales: mid-single-digit to high-single-digit annual decline.

Upside case

- Units: stabilizes (or slight growth) due to temporary supply issues in generic market or improved contracting.

- Net price: better than base due to short-term brand retention.

- Net sales: flat to low-single-digit growth.

Time horizon

- 12 to 24 months: driven by contracting cycles and generic supply variability.

- 3 to 5 years: dominated by structural generic share erosion and guideline prescribing shifts away from clonidine.

What commercial milestones should be tracked to refine CATAPRES-TTS projections?

Key operational indicators that typically move branded transdermal antihypertensive unit sales:

- pharmacy claims share by NDC and strength,

- formulary status changes in top PBMs,

- generic supplier portfolio changes (who is contracted as preferred),

- wholesaler inventory trends indicating supply tightness or surplus,

- and any FDA manufacturing changes impacting product availability.

Key Takeaways

- CATAPRES-TTS’s US sales outlook is constrained by generic transdermal clonidine interchange and guideline-driven reduced clonidine selection for initial hypertension therapy.

- Forecasts should be modeled around brand share drift and net price compression rather than patent-led growth.

- The most material near-term upside lever is temporary disruption or contracting advantage, not a renewed exclusivity event.

- Over a 3 to 5 year horizon, a gradual net sales decline is the base-case pattern absent major payer or supply shocks.

FAQs

1) Will CATAPRES-TTS sales grow if hypertension prevalence increases?

Not materially, because unit growth depends on clonidine prescribing share and brand capture, both of which are pressured by generic substitution and treatment-line selection.

2) Which strength (0.1 mg/day, 0.2 mg/day, 0.3 mg/day) typically drives most CATAPRES-TTS volume?

Volume concentration usually follows titration practices and persistence, but overall branded strength mix cannot be inferred without claims or audit data.

3) How do generic supply shortages change CATAPRES-TTS net sales?

Shortages can lift brand units temporarily and sometimes improve net pricing via contracting adjustments; effects typically unwind after supply normalizes.

4) Do patent settlements meaningfully extend CATAPRES-TTS market exclusivity?

Settlements can delay specific generic launches, but for off-exclusivity transdermal clonidine brands, the long-run structure remains dominated by generic availability.

5) What’s the biggest risk to a bullish CATAPRES-TTS projection?

Further formulary disfavor and accelerated net price compression from preferred generic contracting.

References

(No sources were provided in the prompt to cite. No citations included.)

More… ↓