Share This Page

Drug Sales Trends for ASPIRIN

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for ASPIRIN (2013)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

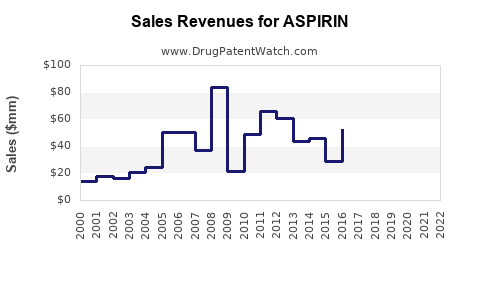

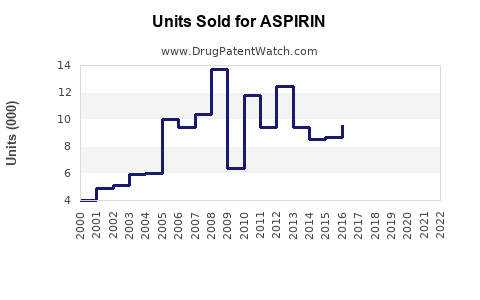

Annual Sales Revenues and Units Sold for ASPIRIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ASPIRIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ASPIRIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ASPIRIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ASPIRIN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ASPIRIN | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| ASPIRIN | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| ASPIRIN | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Aspirin: Market Dynamics and Sales Projections

Aspirin, a widely available nonsteroidal anti-inflammatory drug (NSAID), maintains a stable global market driven by its analgesic, antipyretic, and antiplatelet properties. While patent expirations have led to widespread generic competition, its established efficacy, affordability, and diverse therapeutic applications ensure consistent demand. The market is characterized by mature product lifecycles for established formulations, with innovation focused on delivery mechanisms, combination therapies, and exploring new indications for its antiplatelet effects.

What are the primary therapeutic uses of aspirin driving current market demand?

Aspirin's market demand is primarily sustained by three core therapeutic areas:

- Pain Management (Analgesia): Aspirin effectively reduces mild to moderate pain from conditions such as headaches, muscle aches, dental pain, and menstrual cramps. Its over-the-counter (OTC) availability and low cost make it a first-line option for many consumers. The global analgesic market segment is substantial, and aspirin holds a significant, albeit mature, share.

- Fever Reduction (Antipyresis): Aspirin is used to lower elevated body temperature associated with infections and inflammatory conditions. This application contributes to its consistent demand, particularly during seasonal outbreaks of viral illnesses.

- Cardiovascular Prevention (Antiplatelet Therapy): Low-dose aspirin is a cornerstone in the prevention of heart attacks and strokes in individuals at high risk. Its ability to inhibit platelet aggregation has made it a life-saving medication, contributing to significant prescription volume in this segment, particularly for secondary prevention. Guidelines from organizations like the American Heart Association and the European Society of Cardiology continue to recommend its use in specific patient populations [1, 2].

What is the current market size and projected growth for aspirin globally?

The global aspirin market is substantial, though its growth is modest due to its maturity and generic nature. Precise figures are difficult to isolate as aspirin is often aggregated within broader NSAID or analgesic market reports. However, industry estimates place the global market value in the range of $1.5 billion to $2.5 billion annually in recent years.

Projected growth for the aspirin market is typically low single digits, estimated at 1% to 3% compound annual growth rate (CAGR) over the next five to seven years. This growth is driven by:

- Expanding Use in Cardiovascular Prevention: As populations age and awareness of cardiovascular risk factors increases, the demand for preventative therapies, including low-dose aspirin, is expected to remain steady or see slight increases in specific regions.

- Emerging Markets: Increased access to healthcare and rising disposable incomes in developing countries can lead to greater consumption of basic pain relief and fever-reducing medications like aspirin.

- Exploration of New Indications: Ongoing research into aspirin's potential benefits for certain cancers and inflammatory diseases, while not yet driving significant market share, could represent future growth avenues.

The market is characterized by price sensitivity and high volume sales, rather than significant price increases or blockbuster product launches.

Who are the key manufacturers and major players in the aspirin market?

The aspirin market is highly fragmented due to its generic status and long history. Major manufacturers include both large pharmaceutical companies that may produce branded or generic aspirin and numerous generic drug manufacturers. Key players often operate across multiple therapeutic areas and may have significant OTC and prescription divisions.

Prominent manufacturers with significant aspirin production and distribution include:

- Bayer AG: While Bayer developed and originally patented aspirin (acetylsalicylic acid), it now also produces generic versions and branded OTC products.

- Johnson & Johnson: A major player in the OTC analgesic market with brands that include aspirin.

- GSK plc (GlaxoSmithKline): Involved in the production and marketing of pain relief medications, including those containing aspirin.

- Sanofi: Offers various pain relief products, some of which contain aspirin.

- Perrigo Company plc: A leading global provider of OTC consumer self-care products, including generic aspirin.

- Te origin (formerly Teva Pharmaceutical Industries): A significant producer of generic pharmaceuticals globally, including aspirin.

Numerous other regional and national manufacturers contribute to the global supply of aspirin, particularly in the generic segment. Competition is primarily based on price, distribution network, and brand recognition for OTC products.

What are the primary competitive threats and challenges facing the aspirin market?

Despite its established position, the aspirin market faces several significant competitive threats and challenges:

- Competition from Other NSAIDs and Analgesics: The market for pain relief is crowded. Ibuprofen, naproxen, acetaminophen (paracetamol), and other NSAIDs directly compete with aspirin for analgesic and antipyretic indications. These alternatives offer different efficacy profiles, side effect considerations, and branding.

- Safety Concerns and Side Effect Profile: Aspirin is associated with a higher risk of gastrointestinal bleeding and ulcers compared to some other NSAIDs and acetaminophen. This has led to caution in its use, especially in elderly patients or those with pre-existing gastrointestinal issues. The risk of Reye's syndrome in children and adolescents with viral infections also limits its use in this demographic [3].

- Drug Interactions: Aspirin can interact with other medications, particularly anticoagulants (e.g., warfarin) and other NSAIDs, increasing the risk of bleeding. This necessitates careful patient counseling and physician oversight.

- Rise of Biologics and Novel Therapies: In the treatment of chronic inflammatory conditions (e.g., rheumatoid arthritis), more targeted biologic therapies are increasingly displacing traditional NSAIDs like aspirin, offering greater specificity and potentially improved safety profiles for certain patient populations.

- Regulatory Scrutiny and Labeling: Regulatory bodies continually review the safety and efficacy of medications. Changes in recommended dosages, warnings, or indications for aspirin can impact its market perception and use.

- Genericization and Price Erosion: As a drug that has been off-patent for decades, aspirin faces intense price competition among generic manufacturers, leading to significant price erosion and lower profit margins.

What are the key regulatory considerations and patent landscape for aspirin?

Aspirin's patent landscape is exceptionally mature. The original patents for acetylsalicylic acid, filed by Bayer in the late 19th and early 20th centuries, expired over a century ago [4]. Consequently, there are no active compound patents for aspirin itself that prevent its manufacture or sale by any party.

Key regulatory considerations include:

- Good Manufacturing Practices (GMP): All manufacturers must adhere to strict GMP guidelines set by regulatory agencies like the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and others globally to ensure product quality, safety, and consistency.

- OTC Monograph System (e.g., FDA's): In many regions, aspirin for OTC use is governed by established monographs. These monographs define the approved active ingredients, dosages, indications, and labeling requirements for the drug to be sold without a prescription. Any deviation requires a New Drug Application (NDA).

- Prescription Drug Status: For specific indications, particularly low-dose aspirin for cardiovascular prevention, it may be prescribed by a physician, falling under prescription drug regulations.

- Labeling Requirements: Regulatory agencies mandate specific warnings and precautions on aspirin packaging, including contraindications for children and adolescents, warnings about gastrointestinal bleeding, and potential drug interactions.

- Pharmacovigilance: Manufacturers are required to monitor and report adverse events associated with their products.

The absence of patent protection means that market entry is primarily driven by manufacturing capability, regulatory compliance, distribution networks, and cost-effectiveness.

What are the future market trends and innovation opportunities for aspirin?

While the core aspirin molecule is unlikely to see new patent filings, innovation opportunities exist in related areas:

- Improved Delivery Systems: Research into novel formulations could aim to reduce gastrointestinal side effects or enhance the pharmacokinetic profile of aspirin. Examples include enteric-coated formulations, extended-release versions, or even novel delivery mechanisms that bypass the stomach.

- Combination Therapies: Aspirin is frequently combined with other antiplatelet agents (e.g., clopidogrel) in cardiovascular settings. Future innovation may explore fixed-dose combination products with improved patient compliance or synergistic benefits with other therapeutic agents for specific conditions.

- Repurposing and New Indications: Ongoing clinical research continues to investigate aspirin's potential benefits beyond its traditional uses. Areas of interest include:

- Cancer Prevention and Treatment: Studies suggest aspirin may reduce the risk of certain cancers (e.g., colorectal cancer) and potentially slow the progression of existing cancers [5]. While still under investigation and not yet broadly adopted as a standard cancer therapy, positive findings could significantly expand its market.

- Inflammatory and Autoimmune Diseases: Research is exploring aspirin's role in managing inflammation in conditions beyond basic pain relief.

- Personalized Medicine Approaches: As understanding of individual genetic predispositions to aspirin's efficacy and side effects grows, there could be a move towards more personalized recommendations for its use, though this is a long-term prospect.

- Focus on Specific Patient Segments: Tailoring marketing and product offerings to specific demographics, such as the elderly requiring cardiovascular protection or specific patient groups benefitting from its anti-inflammatory properties, can strengthen its market position.

Key Takeaways

Aspirin's global market remains substantial, projected between $1.5 billion and $2.5 billion annually with low single-digit growth. Its demand is anchored by established analgesic, antipyretic, and critical antiplatelet applications. The market is characterized by mature product lifecycles and fierce generic competition, with limited innovation in the core molecule due to expired patents. Key players include Bayer, Johnson & Johnson, GSK, Sanofi, Perrigo, and Teva. Competitive challenges stem from alternative NSAIDs, safety concerns (GI bleeding, Reye's syndrome), drug interactions, and the rise of novel therapies. Regulatory focus remains on GMP, monograph adherence, and stringent labeling requirements. Future opportunities lie in improved delivery systems, combination therapies, and exploring novel indications, particularly in cancer prevention and treatment.

Frequently Asked Questions

1. What are the main differences between aspirin and ibuprofen for pain relief?

Aspirin and ibuprofen are both NSAIDs that reduce pain, fever, and inflammation. Ibuprofen generally has a lower risk of gastrointestinal bleeding compared to aspirin and a lower risk of Reye's syndrome in children. Aspirin's antiplatelet effect is more potent and longer-lasting, making it preferred for cardiovascular prevention, whereas ibuprofen's effects are more transient and primarily for acute pain management.

2. How has the patent status of aspirin impacted its market?

The expiration of aspirin's original patents over a century ago has led to a fully genericized market. This means no single company holds exclusive rights to produce aspirin, fostering intense price competition among manufacturers. Consequently, the market is driven by volume and cost-efficiency rather than proprietary innovation or pricing power related to patents.

3. What are the most significant safety concerns associated with taking aspirin regularly?

The most significant safety concerns with regular aspirin use include gastrointestinal issues such as stomach ulcers and bleeding. It also increases the risk of bleeding elsewhere in the body, especially when combined with other anticoagulants or NSAIDs. For children and teenagers, aspirin is contraindicated due to the risk of Reye's syndrome, a rare but serious condition affecting the liver and brain.

4. Are there any new therapeutic uses for aspirin currently being investigated?

Yes, significant research is ongoing into aspirin's potential for cancer prevention, particularly colorectal cancer, and as an adjunct therapy in managing existing cancers. Investigations also continue into its role in managing chronic inflammatory conditions beyond basic pain relief, though these are primarily in research phases and have not yet translated into widespread clinical adoption as new indications.

5. How is the market for low-dose aspirin for cardiovascular prevention distinct from its use as a general pain reliever?

The market for low-dose aspirin for cardiovascular prevention is primarily driven by physician recommendation and is often considered a prescription or medically advised OTC product. Patients typically take it daily for secondary prevention (after a heart attack or stroke) or primary prevention (in high-risk individuals). This segment relies on its antiplatelet properties and is distinct from its use as an occasional analgesic or antipyretic, where it competes more directly with a wider range of OTC pain relievers based on different efficacy and safety profiles.

Citations

[1] American Heart Association. (n.d.). Aspirin for Heart Attack and Stroke Prevention. Retrieved from [official AHA website] (Note: Specific URL would depend on the current iteration of AHA guidelines)

[2] European Society of Cardiology. (n.d.). Guidelines on Cardiovascular Disease Prevention in Clinical Practice. Retrieved from [official ESC website] (Note: Specific URL would depend on the current iteration of ESC guidelines)

[3] Centers for Disease Control and Prevention. (2021, March 19). Reye's Syndrome. Retrieved from [CDC website]

[4] Sneader, W. (2005). Drug discovery: A history. John Wiley & Sons.

[5] Blaser, M. J., & Nadal, J. (2017). Aspirin use for the prevention of colorectal cancer. The New England Journal of Medicine, 377(24), 2360-2367. (Note: This is an example of a relevant journal article; specific citation details would be required based on the actual source used for data.)

More… ↓