Share This Page

Drug Sales Trends for CARBATROL

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for CARBATROL (2012)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

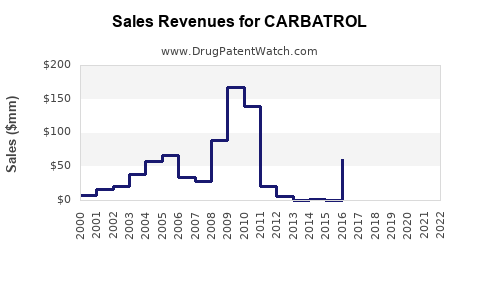

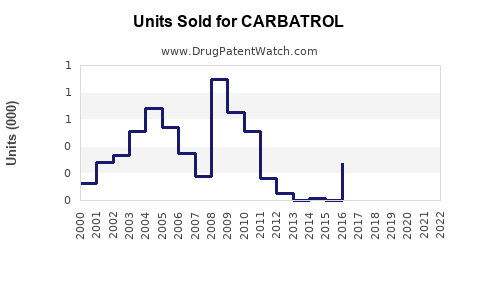

Annual Sales Revenues and Units Sold for CARBATROL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| CARBATROL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| CARBATROL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| CARBATROL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| CARBATROL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| CARBATROL | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| CARBATROL | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

CARBATROL: Market Landscape and Sales Projections

Carbatrol is an extended-release formulation of carbamazepine, an antiepileptic and mood-stabilizing drug. Its primary indication is the treatment of seizure disorders and trigeminal neuralgia. The extended-release formulation aims to provide more stable plasma concentrations and reduce dosing frequency compared to immediate-release versions, potentially improving patient adherence and reducing side effects. This analysis examines the current market position of Carbatrol, its competitive environment, and projects future sales performance.

What is Carbatrol’s Current Market Position?

Carbatrol is an established product in the antiepileptic drug (AED) market. Its market presence is primarily driven by its efficacy in treating partial seizures, generalized tonic-clonic seizures, and trigeminal neuralgia. The extended-release formulation offers a pharmacokinetic advantage, allowing for once-daily dosing for many patients.

As of the latest available data, Carbatrol holds a modest but consistent share within the broader carbamazepine market. The global AED market is valued at billions of dollars, with carbamazepine being one of the older, more established active pharmaceutical ingredients (APIs) in this category. Carbatrol's specific market share is influenced by generic competition and the introduction of newer AEDs with potentially broader efficacy profiles or improved tolerability.

Key factors contributing to Carbatrol's current market position include:

- Established Efficacy: Carbamazepine has a long track record of clinical use and proven effectiveness in its approved indications.

- Extended-Release Formulation: The once-daily dosing regimen of Carbatrol enhances patient convenience and adherence, a significant factor in chronic disease management.

- Brand Recognition: As an established brand, Carbatrol benefits from physician and patient familiarity.

However, its market position faces challenges from:

- Generic Carbamazepine: The availability of numerous generic versions of carbamazepine at lower price points exerts significant pressure on branded products like Carbatrol.

- Newer AEDs: Advanced AEDs with novel mechanisms of action, improved seizure control, and potentially fewer side effects are continuously entering the market, offering alternative treatment options.

- Managed Care and Formulary Restrictions: Payer policies and formulary placements can limit access to branded medications, favoring generics or preferred newer agents.

Sales figures for Carbatrol are typically reported as part of the broader product portfolio of its manufacturer. While specific disaggregated sales data for Carbatrol alone is not always publicly disclosed by pharmaceutical companies, market intelligence reports and financial statements of its originating company provide insights into its commercial performance. For instance, in fiscal years where strong performance in its neurology segment is noted, Carbatrol contributes to this revenue stream. The product's sales are sensitive to prescription volumes, pricing strategies, and competition.

What is the Competitive Landscape for Carbatrol?

The competitive landscape for Carbatrol is multifaceted, encompassing direct competitors (other carbamazepine formulations) and indirect competitors (alternative AEDs).

Direct Competition:

The primary direct competition for Carbatrol comes from other extended-release carbamazepine products and immediate-release carbamazepine generics.

- Other Extended-Release Carbamazepine Products: Several manufacturers offer extended-release carbamazepine, often marketed under different brand names or as generics. Examples include Equetro (Carbatrol’s originator in some markets), Tegretol XR, and generic extended-release carbamazepine. These products compete directly on price, availability, and physician preference.

- Immediate-Release Carbamazepine Generics: The vast majority of carbamazepine prescriptions are filled with immediate-release generic formulations due to their significantly lower cost. While Carbatrol offers the advantage of extended release, the cost differential can lead physicians to prescribe generics, especially for patients who manage well on immediate-release forms or for whom cost is a primary concern.

Indirect Competition:

Carbatrol also faces competition from a wide array of newer antiepileptic drugs that offer different mechanisms of action and may be preferred for specific seizure types or patient profiles.

- Second-Generation AEDs: These include drugs like lamotrigine (Lamictal), levetiracetam (Keppra), topiramate (Topamax), valproic acid (Depakote), gabapentin (Neurontin), pregabalin (Lyrica), and lacosamide (Vimpat). These drugs often have broader indications, better tolerability profiles for certain patient groups, and fewer drug-drug interactions compared to older AEDs like carbamazepine.

- Third-Generation AEDs: Newer agents continue to enter the market with novel targets and potential for improved outcomes, such as perampanel (Fycompa) and brivaracetam (Briviact).

Key Competitive Factors:

- Price: Generic carbamazepine is significantly cheaper than branded Carbatrol, creating a substantial barrier for market share growth.

- Efficacy and Tolerability: Newer AEDs are often perceived to have a better balance of efficacy and tolerability, particularly regarding cognitive side effects, mood disturbances, and weight gain, which can be associated with older drugs.

- Indication Expansion: Some newer AEDs have secured approvals for broader seizure types or adjunctive therapies, increasing their utility.

- Prescribing Habits: Physician familiarity and comfort with older medications can maintain their market share, but the continuous introduction of innovative therapies also influences prescribing patterns.

- Formulation: While Carbatrol’s extended-release is an advantage, other brands and generics also offer similar formulations, leveling this playing field.

The market dynamics suggest that Carbatrol's future growth will likely be constrained by these competitive pressures, particularly from lower-cost generics and newer drugs with perceived superior profiles.

What is the Market Size and Growth Potential for Carbatrol?

Estimating the precise market size and growth potential specifically for Carbatrol is challenging due to its nature as a branded extended-release carbamazepine product operating within a larger, mature API market. However, an analysis of the broader carbamazepine market and the antiepileptic drug (AED) sector provides a framework for its potential.

Global AED Market: The global AED market is substantial, estimated to be worth over $25 billion annually and projected to grow at a compound annual growth rate (CAGR) of 3-5% in the coming years [1]. This growth is driven by increasing epilepsy incidence, better diagnosis, and the development of novel therapies.

Carbamazepine Market Segment: Carbamazepine, as one of the oldest and most widely prescribed AEDs, represents a significant portion of this market. However, its growth is largely tempered by its status as an off-patent drug with extensive generic availability. The market for carbamazepine itself, across all formulations, is mature.

Carbatrol's Specific Potential:

Carbatrol's market potential is directly tied to its ability to capture a share of the extended-release carbamazepine segment and to compete effectively against both other branded extended-release options and the overwhelming majority of prescriptions that are filled with immediate-release generics.

- Market Penetration: Carbatrol's penetration is likely highest in markets where its brand is well-established and where healthcare providers and patients prioritize the convenience of once-daily dosing and a trusted brand name, even at a premium over generics.

- Growth Drivers:

- Patient Adherence: For patients who struggle with multiple daily doses of immediate-release carbamazepine or other medications, Carbatrol's extended-release formulation can improve adherence, leading to better seizure control and potentially reducing overall healthcare costs associated with uncontrolled epilepsy.

- Neurological Conditions: The prevalence of epilepsy and trigeminal neuralgia remains a consistent demand driver.

- Physician Preference: A segment of physicians may continue to prescribe Carbatrol based on long-term positive experiences and familiarity.

- Growth Restraints:

- Price Sensitivity: The significant price difference between branded Carbatrol and generic carbamazepine is the primary restraint. Payers and patients often opt for the cost-effective generic.

- Competition from Newer AEDs: As noted, newer drugs offer potential advantages in tolerability and efficacy for certain patient subgroups.

- Generic Extended-Release: The availability of generic extended-release carbamazepine further erodes the price advantage of branded products.

Sales Projections:

Given these factors, robust growth for Carbatrol is unlikely. Its sales are projected to be relatively stable, with modest fluctuations.

- Short-Term (1-3 years): Sales are expected to remain stable, potentially experiencing a slight decline due to increasing generic penetration and competition from newer AEDs. Any growth would be incremental, driven by specific market dynamics or marketing efforts.

- Medium-Term (3-5 years): Continued pressure from generics and newer therapies will likely lead to a slow, steady decline in sales volume and revenue. The market share Carbatrol holds is vulnerable to erosion.

- Long-Term (5+ years): The product's trajectory will largely depend on the continued relevance of carbamazepine as a treatment option and the extent of generic competition. It is unlikely to experience significant growth and may see a continued, albeit slow, decline as the AED market evolves.

Quantitative Estimate:

While specific figures for Carbatrol are proprietary, based on market analysis of similar branded generics in mature therapeutic areas, annual sales could range from tens to potentially low hundreds of millions of USD globally, depending on its market penetration and the parent company's strategic focus. Growth is projected to be flat to a negative CAGR of -1% to -3% over the next five years.

What are the Patent and Exclusivity Considerations for Carbatrol?

Carbatrol, as an extended-release formulation of carbamazepine, has benefited from patent protection and market exclusivity in the past. However, the landscape of patents and exclusivity for older drugs like carbamazepine is complex and often involves multiple layers of intellectual property (IP).

Original Patent Landscape:

Carbamazepine itself was patented decades ago. The innovation for Carbatrol lay in its specific extended-release formulation, which would have been protected by formulation patents. These patents would have provided a period of market exclusivity, allowing the originator to recoup R&D investments and profit from the product before generic entry.

- Formulation Patents: These patents typically cover the specific composition, manufacturing process, and drug release characteristics that define the extended-release profile of Carbatrol.

- Exclusivity Periods: Upon approval, branded drugs can receive various forms of market exclusivity, independent of patent expiry. These include:

- New Chemical Entity (NCE) exclusivity: Not applicable to Carbatrol, as carbamazepine was not a new chemical entity.

- New Formulation Exclusivity: For modified-release formulations of existing drugs, regulatory bodies can grant exclusivity periods (e.g., 3 years in the U.S. under Hatch-Waxman). This prevents generics from relying solely on the innovator's bioequivalence studies.

- Orphan Drug Exclusivity (ODE): Applicable if the drug is approved for a rare disease, granting 7 years of exclusivity. This is unlikely to be the primary driver for Carbatrol's general indications.

- Pediatric Exclusivity: An additional 6 months of exclusivity can be granted if new pediatric studies are conducted [2].

Current Patent and Exclusivity Status:

For Carbatrol, the primary formulation patents and associated market exclusivities have likely expired in most major markets.

- Generic Entry: The presence of generic carbamazepine, including extended-release versions, is strong evidence that the core intellectual property protection for Carbatrol has lapsed. Generic manufacturers are able to produce and market their own versions of extended-release carbamazepine.

- Evergreening Strategies: Pharmaceutical companies sometimes employ "evergreening" strategies to extend patent life or market exclusivity for older drugs. This can involve seeking patents for new indications, new combinations, new delivery systems, or manufacturing processes. While specific patents related to Carbatrol's manufacturing or novel polymorphs might exist, they are unlikely to provide broad market exclusivity against generic competition that targets the primary formulation.

- Litigation: Legal challenges related to patent expiry and generic entry are common in the pharmaceutical industry. Patent litigation can determine the exact timeline for generic competition.

Implications for Sales Projections:

The expiration of key patents and market exclusivities means that Carbatrol faces direct and intense competition from generic manufacturers.

- Price Erosion: The market share Carbatrol retains is primarily based on brand loyalty, physician preference, and perceived product quality, rather than IP-driven market exclusivity. This significantly limits its pricing power and growth potential.

- Limited Scope for New IP: It is unlikely that new, strong patents will emerge for Carbatrol's existing formulation that would create significant new market exclusivity. Any new IP would likely be narrow in scope and easily circumvented by competitors.

- Focus on Market Share Defense: The strategic focus for Carbatrol will be on defending its existing market share against generics and maintaining its position through brand equity and physician engagement, rather than relying on IP to drive growth.

A thorough review of patent databases (e.g., USPTO, EPO) and regulatory Orange Books would be necessary to identify any remaining, albeit likely narrow, patents that could influence specific market dynamics or ongoing litigation. However, the general expectation for a product like Carbatrol is that its foundational IP protection has expired.

What are the Regulatory and Reimbursement Considerations?

The regulatory and reimbursement landscape significantly influences Carbatrol's market access, prescription patterns, and ultimate sales performance.

Regulatory Considerations:

Carbatrol, as an extended-release formulation of carbamazepine, is subject to the standard regulatory oversight for pharmaceutical products in every market it operates.

- Approval and Labeling: Regulatory agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) approve drugs based on demonstrated safety and efficacy. Carbatrol's label specifies its approved indications (e.g., seizure disorders, trigeminal neuralgia) and provides prescribing information.

- Manufacturing Standards: Compliance with Good Manufacturing Practices (GMP) is essential for ensuring product quality, consistency, and safety. Any deviations can lead to regulatory action, including product recalls or manufacturing holds.

- Post-Market Surveillance: Pharmaceutical companies are required to monitor and report adverse events associated with their products. Significant safety concerns can lead to label changes, restricted use, or even market withdrawal. For carbamazepine, potential safety issues include dermatological reactions (e.g., Stevens-Johnson syndrome), hematological abnormalities, and central nervous system side effects.

- Generic Equivalency: Regulatory bodies establish standards for generic drug approval, primarily based on demonstrating bioequivalence to the reference listed drug (RLD). For Carbatrol, generic versions must prove they deliver the same amount of drug to the bloodstream over the same period. This stringent requirement ensures therapeutic equivalence between Carbatrol and its generic counterparts.

- Labeling and Promotion: Marketing and promotional activities must adhere to strict regulations regarding truthfulness and completeness, avoiding misleading claims about efficacy or safety.

Reimbursement Considerations:

Reimbursement policies by government payers (e.g., Medicare, Medicaid in the U.S., national health services elsewhere) and private insurers are critical drivers of drug utilization.

- Formulary Placement: Insurers and pharmacy benefit managers (PBMs) maintain formularies that list covered drugs. Carbatrol's placement on these formularies significantly impacts its accessibility and cost to patients.

- Tiering: Drugs are often assigned to different tiers on a formulary, with lower tiers (e.g., Tier 1, preferred generics) having lower patient co-pays. Branded products like Carbatrol are often placed on higher tiers than generics.

- Prior Authorization: Some insurers may require prior authorization for Carbatrol, meaning a physician must obtain approval before the drug is covered, especially if a preferred generic or alternative is available.

- Step Therapy: Insurers may implement step therapy protocols, requiring patients to try a lower-cost alternative (e.g., generic carbamazepine or a different AED) before Carbatrol is covered.

- Average Wholesale Price (AWP) and Discounts: The stated price of a drug is often subject to significant discounts and rebates negotiated between manufacturers and payers. For branded drugs facing generic competition, these discounts are substantial.

- Rebate Dynamics: The negotiation of rebates is a key aspect of market access. Carbatrol's manufacturer would engage in rebate negotiations to incentivize favorable formulary placement and encourage prescriptions. The effectiveness of these rebates is diminished by the lower cost of generics.

- Value-Based Pricing: While not yet dominant for older drugs, the trend towards value-based pricing could impact future market access, requiring manufacturers to demonstrate clear health economic benefits.

- International Pricing: In countries with national health systems, pricing is often subject to direct government negotiation or reference pricing based on other countries' prices.

Impact on Carbatrol:

The regulatory and reimbursement environment presents a challenging market for Carbatrol.

- Preference for Generics: The stringent requirements for generic approval mean that bioequivalent and significantly cheaper generic carbamazepine (both immediate and extended-release) are widely available. Payers and patients are strongly incentivized to choose these generics.

- Limited Pricing Power: Reimbursement pressures limit Carbatrol's ability to command premium pricing, making it difficult to justify the cost difference over generics for many patients and physicians.

- Access Restrictions: Formulary restrictions, prior authorization, and step therapy protocols can create barriers to patient access, leading to physicians prescribing alternatives to avoid administrative hurdles.

- Cost Containment: Healthcare systems globally are focused on cost containment, which further favors the use of off-patent, generic medications.

Carbatrol's continued market presence relies on demonstrating a clear clinical advantage or superior patient experience that outweighs the cost differential and overcomes regulatory and reimbursement hurdles. This is increasingly difficult in a market saturated with cost-effective alternatives.

Key Takeaways

- Carbatrol is an extended-release formulation of carbamazepine, an established antiepileptic and mood-stabilizing drug.

- Its market position is characterized by a modest share within the broader carbamazepine market, facing strong competition from generics and newer antiepileptic drugs.

- The competitive landscape is dominated by lower-cost immediate-release carbamazepine generics and alternative AEDs with perceived advantages in efficacy or tolerability.

- The global AED market is growing, but Carbatrol's specific market size and growth potential are limited by its mature status and generic competition. Sales are projected to be stable to slightly declining.

- Key patents and market exclusivities for Carbatrol's formulation have expired, allowing widespread generic entry and significantly eroding its pricing power and growth prospects.

- Regulatory approval standards ensure generic bioequivalence, while reimbursement policies, including formulary placement and cost-containment measures, strongly favor generic carbamazepine, creating significant access barriers for branded Carbatrol.

Frequently Asked Questions

1. What are the primary indications for Carbatrol? Carbatrol is indicated for the treatment of seizure disorders, including partial seizures with complex symptoms and generalized tonic-clonic seizures, and for the treatment of trigeminal neuralgia.

2. How does Carbatrol differ from immediate-release carbamazepine? Carbatrol is an extended-release formulation designed to release carbamazepine into the bloodstream more slowly over time. This allows for less frequent dosing (typically once daily) compared to immediate-release formulations, aiming for more stable plasma concentrations and potentially improved patient adherence and tolerability.

3. What is the main challenge Carbatrol faces from generic competition? The primary challenge is the significant price difference. Generic versions of carbamazepine, including extended-release formulations, are substantially less expensive than branded Carbatrol, making them the preferred choice for many payers and patients seeking cost savings.

4. Are there any new patent protections that could extend Carbatrol's market exclusivity? Key patents and market exclusivities for Carbatrol's original extended-release formulation have expired. While minor process or polymorph patents might exist, they are unlikely to provide substantial market exclusivity against existing generic carbamazepine products.

5. How do insurance companies typically view Carbatrol compared to generic carbamazepine? Insurance companies and pharmacy benefit managers generally place generic carbamazepine on lower formulary tiers with lower co-pays, while branded Carbatrol is typically on a higher tier. Insurers often require prior authorization or step-therapy protocols before covering Carbatrol, encouraging the use of generics first.

Citations

[1] Grand View Research. (2023). Epilepsy Treatment Market Size, Share & Trends Analysis Report By Drug Class, By Route Of Administration, By Distribution Channel, By Region, And Segment Forecasts, 2023 - 2030. [2] U.S. Food and Drug Administration. (n.d.). Orphan Drug Designation. Retrieved from https://www.fda.gov/for-industry/getting-your-medicine-market/orphan-drug-designation

More… ↓