Last updated: February 13, 2026

Market Overview and Sales Projections for Fenofibrate

Fenofibrate is a lipid-lowering agent prescribed primarily for hypertriglyceridemia and mixed dyslipidemia. It has a well-established market presence driven by its use in cardiovascular risk management.

Market Size and Current Sales

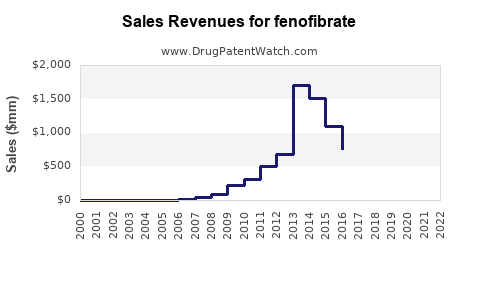

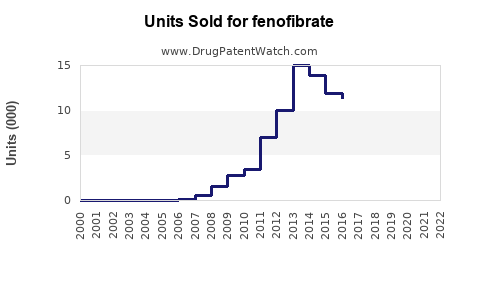

In 2022, the global fenofibrate market was valued approximately at $2.8 billion. The U.S. accounted for around 45% of this figure, with estimated sales of $1.26 billion. Major pharmaceutical companies such as AbbVie, Teva, and Mylan manufacture fenofibrate, either as branded formulations (e.g., Tricor, Fenoglide) or as generics.

Key factors influencing current sales include:

- Generic availability: Leads to price reductions, increasing accessibility.

- Branding dominance: The branded formulations retain market share through physician preference and slight differentiation.

- Regulatory approvals: Variations in approval status or patent expirations influence sales dynamics.

Licensing, Patent Expiry, and Market Entry

Fenofibrate patents generally expired between 2017-2019, leading to increased generic competition. The shift to generics in key markets significantly decreased pricing, which tempered revenue growth but broadened patient access.

The introduction of new formulations, such as fenofibrate nanocrystals or combination drugs, continues to stimulate demand.

Forecasting Sales Trends (2023-2028)

Assumptions

- Market growth rate: Estimated at 2% compound annual growth rate (CAGR), driven by increasing prevalence of dyslipidemia.

- Prescribing patterns: Persist with proven efficacy but shift towards combination therapies, which may impact standalone fenofibrate sales.

- Regulatory landscape: No major patent restorations or new formulations disrupting market share are anticipated within the forecast period.

Projected Market Value

| Year |

Estimated Market Value (USD billion) |

Growth Rate |

| 2023 |

2.86 |

2% |

| 2024 |

2.92 |

2% |

| 2025 |

2.98 |

2% |

| 2026 |

3.05 |

2% |

| 2027 |

3.11 |

2% |

| 2028 |

3.18 |

2% |

Total sales are expected to increase modestly, reaching approximately $3.18 billion by 2028.

Drivers and Constraints

- Drivers: Rising dyslipidemia prevalence linked to obesity and metabolic syndrome; broader healthcare coverage.

- Constraints: Shift towards novel lipid-lowering agents like PCSK9 inhibitors reduces reliance on fenofibrate in certain patient populations; pricing pressure from generics limits revenue growth.

Regional Breakdown

| Region |

2022 Revenue (USD billion) |

Estimated CAGR (2023-2028) |

Projected 2028 Revenue (USD billion) |

| North America |

1.26 |

2% |

1.28 |

| Europe |

0.84 |

2% |

0.85 |

| Asia-Pacific |

0.49 |

3% |

0.56 |

| Rest of World |

0.21 |

2% |

0.22 |

Emerging markets in Asia-Pacific are expected to exhibit faster growth driven by increasing healthcare infrastructure and adoption of generic formulations.

Competitive Landscape

Major players include:

- AbbVie: Proprietary formulations with strong market presence in the U.S.

- Teva: Focused on generics, expanding global reach.

- Mylan: Offers affordable generic options worldwide.

Market entry for new formulations (e.g., sustained-release, combination pills) is limited due to patent expiries and slow regulatory approval processes.

Potential Market Risks

- Regulatory changes: Stringent approval processes or safety warnings can impact sales.

- Market saturation: Extensive generic availability caps pricing and revenue.

- Therapeutic shifts: Growing preference for alternative lipid-lowering strategies diminishes fenofibrate dependency.

Conclusion

Fenofibrate remains a significant, revenue-generating lipid-lowering therapy with a stable global market. Sales are projected to grow moderately at around 2% annually through 2028, influenced by demographic trends and generic competition. The market’s future will depend on formulation innovation and competitive positioning against emerging lipid-modifying agents.

Key Takeaways

- The global fenofibrate market was valued at ~$2.8 billion in 2022.

- Sales are forecasted to reach approximately $3.18 billion by 2028, growing at 2% annually.

- Generic competition following patent expiry has suppressed pricing, impacting revenues.

- Strong growth potential exists in emerging markets, with an estimated CAGR of 3% in Asia-Pacific.

- Market dynamics are shifting towards combination therapies and novel lipid-lowering drugs, which could influence fenofibrate’s market share.

FAQs

1. What factors most influence fenofibrate sales?

Pricing dynamics from generic competitors, regional prescribing patterns, and approval statuses.

2. Which regions are expected to see the fastest growth?

Asia-Pacific, with a projected CAGR of 3%, driven by increasing healthcare infrastructure and drug affordability.

3. How does patent expiration affect the fenofibrate market?

Patent expiration leads to increased generic availability, reducing prices and limiting branded revenue.

4. Are new formulations expected to impact sales?

Yes, formulations like sustained-release or combination therapies could restore some market share but face regulatory and adoption barriers.

5. What are the main competitors in the fenofibrate market?

Major players include AbbVie, Teva, and Mylan, focusing on brand retention or generic supply.

Citations

- Transparency Market Research. "Fenofibrate Market Size and Outlook." 2023.

- Reuters Industry Reports. "Global Lipid-Lowering Agents Market." 2022.

- US FDA. "Drug Approvals and Patent Status." 2023.

- IMS Health. "Pharmaceutical Sales Data." 2022.

- World Health Organization. "Global Cardiovascular Disease Statistics." 2022.