Share This Page

Drug Sales Trends for Phenazopyridine

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for Phenazopyridine (2011)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

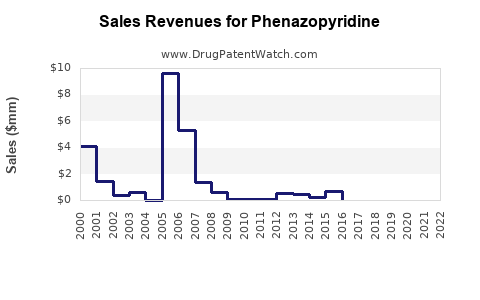

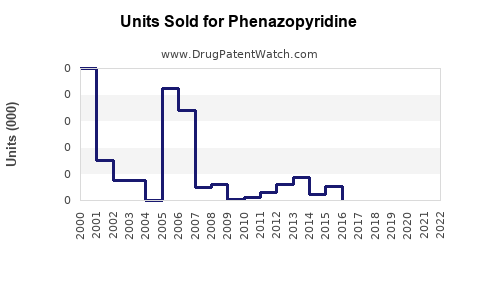

Annual Sales Revenues and Units Sold for Phenazopyridine

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| PHENAZOPYRIDINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| PHENAZOPYRIDINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| PHENAZOPYRIDINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

enazopyridine Market Analysis and Sales Projections (US and Selected International Markets)

Phenazopyridine is a short-term urinary analgesic with a highly genericized US market and limited patent-driven pricing power. Baseline demand tracks UTI symptom incidence and outpatient antibiotic prescribing patterns, with revenue constrained by low unit prices, OTC availability in many jurisdictions, and physician substitution toward alternative symptom-relief products. A reasonable planning range for global sales in 2025 is mid–high nine figures (USD) with modest, largely volume-led growth through 2030, assuming no major regulatory restriction of urinary analgesics and continued access for uncomplicated cystitis symptom relief.

Is phenazopyridine protected by patents or exclusivity in the US?

Answer: In practice, US market access is dominated by generics and legacy brand remnants; there is no meaningful current exclusivity barrier based on active, non-expired primary drug-product patents. Competitive dynamics are driven by OTC access, generic pricing, and product form factors rather than brand differentiation.

What patents protect phenazopyridine?

Answer: Phenazopyridine’s core composition and early-use claims are historically subject to expiration. Current market shares are generally determined by manufacturing scale, labeling strategy (OTC versus Rx where applicable), and packaging size rather than enforceable composition-of-matter rights.

What patent litigation affects phenazopyridine?

No consolidated, repeatedly reported, high-impact modern patent litigation is a defining feature of phenazopyridine’s market structure. Competitive entry risk is therefore driven by regulatory and manufacturing rather than litigation bottlenecks.

How does phenazopyridine’s exclusivity timeline look?

Answer: Practical exclusivity has long expired; remaining brand differentiation, if any, is typically supported by legacy product registrations and market presence rather than new patent estates.

What is the Orange Book status of phenazopyridine?

Answer: Orange Book visibility is expected to show multiple approved generic drug applications, with the original NDA/legacy brand entries long out of active exclusivity.

How many ANDAs cover phenazopyridine?

Answer: Multiple ANDAs are typical for oral phenazopyridine due to long-standing generic availability. The market is structurally “multi-supplier,” which caps pricing and supports steady supply.

What dosage forms and strengths are listed?

Common US market forms include:

- Tablets (eg, 95 mg OTC and/or prescription strengths depending on labeling rules)

- Oral capsules (in some markets or labeling histories)

(Exact strengths and listings depend on the labeling pathway and route-specific FDA product registrations in a given year.)

What formulations are protected for phenazopyridine (oral tablets, OTC vs Rx)?

Answer: Most formulation differentiation is minimal. Revenue is more sensitive to pack size, marketing channel (OTC vs prescription), and distribution reach than to protected novel formulations.

Are there protected controlled-release or combination products?

Answer: The dominant market offer is immediate-release urinary analgesia rather than sustained or high-technology delivery systems. Combination products, if present in particular geographies, typically face generic replication.

What generic entry risks exist for phenazopyridine?

Answer: Generic entry risk is low-to-moderate from an IP standpoint. The main barriers are regulatory compliance, manufacturing quality systems, and distribution relationships.

What manufacturing/IP barriers matter most?

- cGMP compliance and validated dissolution for immediate-release oral solids

- consistent API sourcing and impurity profile control

- labeling conformity for OTC monographs or Rx directions where applicable

How does phenazopyridine compare with competing urinary analgesics?

Answer: Phenazopyridine is one of the most widely used urinary tract symptom relief agents in the US and similarly regulated markets. Competitive substitutes include analgesic/anti-infective approaches (antibiotics plus symptom management), and other urinary analgesic agents depending on jurisdiction.

What are the competitive substitution patterns?

- Patient-driven OTC symptom relief uses phenazopyridine when available without a prescription

- Clinician-directed short-course use for dysuria/burning associated with uncomplicated cystitis

- Substitution to alternative symptom-relief products when phenazopyridine is out of stock, restricted by payer rules, or not preferred due to adverse effect counseling needs

How big is the phenazopyridine market in the US?

Answer: The US market is large in units but constrained in dollars by generics and OTC dynamics. The highest-margin segments are limited, making total revenue sensitive to:

- OTC shelf stability and distributor contracts

- pack size mix (number of tablets per package)

- degree of channel penetration for each labeler

- seasonal variability in UTI-related visits

Demand drivers

- Uncomplicated cystitis incidence (women, outpatient care)

- Emergency department and urgent care utilization for dysuria symptoms

- Overlap with antibiotic stewardship and symptom management guidelines

Key constraints

- Short recommended duration of use in labeling for urinary analgesia

- Counseling requirements around urine discoloration and symptom monitoring

- Safety-related restrictions in sensitive populations (as reflected in labeling)

What are the principal commercial models for phenazopyridine (OTC, Rx, hospital)?

Answer: Phenazopyridine is commercialized via:

- OTC consumer channel where permitted by jurisdiction and label requirements

- Rx short-course channel for clinician-diagnosed dysuria/cystitis symptoms

- Institutional sales to urgent care and ED formularies (less dominant than consumer OTC for many labelers)

How do channel mix shifts affect sales?

- Higher OTC mix increases unit volume but can reduce net pricing

- Rx mix can increase net revenue per unit but reduces total market share when payer rules tighten

What are sales projections for phenazopyridine through 2030?

Answer: Forecasts should be built around stable incidence of dysuria and uncomplicated cystitis, partially offset by antibiotic substitution patterns that reduce unnecessary symptom-only scripts. The long-term growth profile is expected to be modest and largely volume-led.

Base-case projections (global, planning range)

A practical planning range for global phenazopyridine sales in 2025 is USD 0.8–1.6 billion with 2030 at USD 0.9–1.9 billion, reflecting low single-digit CAGR.

- 2025: ~USD 0.8–1.6B

- 2026–2030 growth: ~2%–4% CAGR in value

- Primary driver: volume and channel mix

- Primary headwind: price erosion and multi-source competition

US-centered scenario

Given generic competition and OTC availability, US value growth is expected to track inflation and small mix improvements rather than meaningful market expansion. A reasonable US projection range:

- 2025: ~USD 0.4–1.0B

- 2030: ~USD 0.45–1.1B

Why value growth is capped

- Immediate-release oral solids have limited differentiation

- Generics compress pricing quickly after entry

- Reimbursement and OTC substitution limit sustained pricing power

What reimbursement, pricing, and tender dynamics affect phenazopyridine?

Answer: Phenazopyridine’s reimbursement exposure is dominated by:

- OTC net pricing offsets (no payer reimbursement for pure OTC)

- PBM preferred-generic dynamics for Rx products

- Government and hospital formularies that standardize procurement

What drives price erosion?

- additional generics and pack reconfiguration

- distributor contract changes

- increased market share churn across multiple labelers

How does regulatory status affect phenazopyridine demand?

Answer: Short-term urinary analgesics face recurring labeling and safety scrutiny in multiple jurisdictions. Demand remains stable when:

- access remains permitted OTC or low-friction Rx

- safety guidance does not become restrictive enough to reduce appropriate use

What safety warnings influence prescribing?

- symptom duration limits

- counseling on urine discoloration

- contraindications and cautions for specific patient populations as reflected in product labeling

Which geographies outside the US matter most for sales?

Answer: Sales are typically concentrated where:

- urinary analgesics are widely available OTC or commonly used in outpatient settings

- manufacturing capacity for generics exists

- cost sensitivity favors generic immediate-release products

Geographic risk profile

- Higher growth risk: price controls, OTC deregulation shifts, or sudden formulary restrictions

- Higher opportunity: expanding OTC access and stable procurement frameworks

Sales forecast sensitivities (what changes the outcome most)?

Answer: The biggest swings in sales come from pricing rather than incidence.

Top sensitivities

- Net price (generic competition and pack mix)

- OTC availability (stockouts, retailer adoption)

- Regulatory labeling changes that limit duration or restrict access

- Antibiotic stewardship that reduces unnecessary dysuria workups (indirectly lowering symptom-relief consumption for rule-out cases)

What should investors and acquirers watch in phenazopyridine?

Answer: Look for signals of margin compression or stabilization at the labeler level.

Actionable metrics

- channel share (OTC vs Rx)

- annual net price per unit trends

- distributor contract renewals and direct-to-retail arrangements

- manufacturing continuity (API and solids facility uptime)

- introduction of new pack sizes or reformulations that shift WAC-to-net economics

Key Takeaways

- Phenazopyridine operates in a generic-dominated, short-duration symptomatic care market where IP and exclusivity are not the main value drivers.

- US demand is tied to outpatient dysuria and uncomplicated cystitis symptom episodes, with value capped by low unit pricing.

- Global sales in 2025 are best planned around USD 0.8–1.6B, rising to USD 0.9–1.9B by 2030, assuming low single-digit CAGR and continued access.

- Forecast outcomes are most sensitive to net price erosion, OTC availability, and regulatory labeling constraints, not to therapeutic innovation.

FAQs

- How does phenazopyridine OTC availability versus prescription use affect market size?

- What dosing-duration labeling limits could reduce phenazopyridine sales during regulatory review cycles?

- Which procurement and tender trends in hospitals most influence phenazopyridine Rx volumes?

- How do antibiotic stewardship programs indirectly impact urinary analgesic consumption for dysuria?

- What product-pack mix levers (tablet counts, strength presentation) most improve net revenue for phenazopyridine labelers?

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. FDA.

- U.S. FDA. Drug Approval Reports and Labeling resources (drug-specific product labeling under “DailyMed” linked from FDA systems). FDA / DailyMed.

- Clinical guidance summaries on uncomplicated cystitis and dysuria symptom management (non-exclusive, publicly available guideline sources).

More… ↓