Share This Page

Drug Sales Trends for lovastatin

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for lovastatin (2010)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

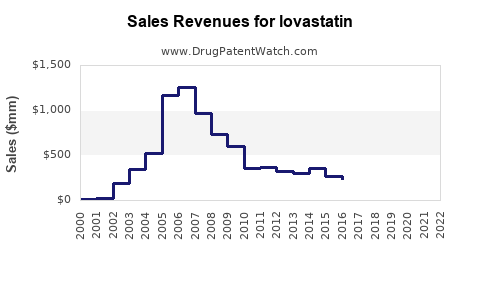

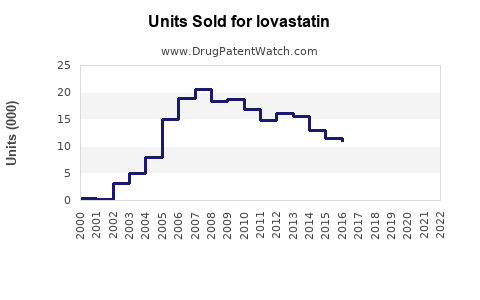

Annual Sales Revenues and Units Sold for lovastatin

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LOVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LOVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LOVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LOVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| LOVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| LOVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| LOVASTATIN | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

LOVASTATIN MARKET ANALYSIS AND SALES PROJECTIONS

Lovastatin, a first-generation statin, continues to hold a position in the cholesterol-lowering drug market, primarily driven by its established efficacy and cost-effectiveness. While newer, more potent statins have emerged, lovastatin maintains a significant patient base, particularly in price-sensitive markets and for individuals with moderate hypercholesterolemia. This analysis examines the current market landscape, key competitive factors, and projected sales for lovastatin over the next five years.

Historical Market Performance and Current Landscape

Lovastatin was the first statin approved by the U.S. Food and Drug Administration (FDA) in 1987 [1]. Its initial success paved the way for the widespread adoption of statin therapy in managing cardiovascular disease risk. The drug's mechanism of action involves inhibiting HMG-CoA reductase, a key enzyme in cholesterol synthesis.

The market for lovastatin has evolved considerably since its introduction. The patent expiration of the innovator drug (Mevacor) led to the proliferation of generic versions, significantly driving down prices. This has resulted in a highly competitive generic market characterized by numerous manufacturers.

Key factors influencing the current lovastatin market include:

- Generic Competition: The market is dominated by generic manufacturers, with little to no brand loyalty for the originator product. Pricing is a primary competitive differentiator.

- Therapeutic Equivalence: Lovastatin is considered therapeutically equivalent to other statins for many indications, making it a viable option for a broad patient population.

- Cost-Effectiveness: Its low cost makes it an attractive option for healthcare systems and patients with limited insurance coverage or high co-pays.

- Established Safety Profile: Decades of clinical use have established a well-understood safety and tolerability profile for lovastatin.

- Clinical Guidelines: Current guidelines, such as those from the American Heart Association and American College of Cardiology, recommend statin therapy for primary and secondary prevention of cardiovascular disease, providing a consistent demand for cholesterol-lowering agents, including lovastatin [2].

Market Share and Volume:

While precise current market share data for individual generic statins is often proprietary, lovastatin collectively accounts for a notable portion of the overall statin market volume. Sales are primarily driven by prescription volume rather than high per-unit price. The drug is available in immediate-release and extended-release formulations, with daily dosages typically ranging from 10 mg to 80 mg.

Geographic Distribution:

Lovastatin sales are globally distributed, with significant volumes in North America, Europe, and Asia. Emerging markets, where access to newer, more expensive therapies may be limited, represent a substantial growth area for generic lovastatin.

Competitive Landscape and Future Outlook

The competitive landscape for lovastatin is characterized by intense price competition among generic manufacturers. Key players include a multitude of pharmaceutical companies producing generic versions of the drug. Differentiating factors in this market are primarily production efficiency, supply chain reliability, and the ability to secure favorable formulary placements with payers.

Comparison with Other Statins:

Lovastatin competes directly with other statins, including:

- Simvastatin: Another first-generation statin, with a similar market dynamic of generic availability and cost-effectiveness.

- Atorvastatin (Lipitor): A later-generation statin with higher potency and broader efficacy, but also higher cost, particularly in its branded form. Generic atorvastatin is now widely available and a significant competitor.

- Rosuvastatin (Crestor): Another potent, later-generation statin, often prescribed for patients requiring more aggressive lipid lowering. Generic versions are also available.

- Pravastatin (Pravachol): A first-generation statin with a different metabolic pathway, offering an alternative for patients who experience side effects with other statins.

Market Dynamics Influencing Lovastatin:

- Introduction of Newer Lipid-Lowering Therapies: The advent of PCSK9 inhibitors (e.g., evolocumab, alirocumab) and bempedoic acid has introduced novel mechanisms for lipid management. While these are typically reserved for specific patient populations or those intolerant to statins due to their higher cost, they represent a long-term shift in the treatment paradigm.

- Genericization of Higher-Potency Statins: The patent expiries of atorvastatin and rosuvastatin have made these more potent statins significantly more affordable, increasing their accessibility and potentially drawing market share from older generics like lovastatin, especially for patients needing more aggressive lipid reduction.

- Payer Policies and Formulary Management: Insurance providers and pharmacy benefit managers (PBMs) heavily influence drug utilization through formulary placement and co-pay structures. Lovastatin's low cost often secures it a preferred position on many formularies, particularly for patients with moderate cholesterol levels.

- Patient Adherence and Tolerability: While generally well-tolerated, some patients experience statin-associated side effects. Lovastatin's profile is well-understood, but individual patient responses can vary, leading to consideration of alternative therapies.

- Healthcare System Cost Containment: Global initiatives to reduce healthcare expenditure continue to favor the use of cost-effective generic medications, benefiting drugs like lovastatin.

Future Outlook:

The market for lovastatin is expected to experience a modest decline in volume over the next five years. This decline will be driven by several factors:

- Preference for Newer Statins: For patients requiring more aggressive lipid lowering or those who can afford it, higher-potency generic statins (atorvastatin, rosuvastatin) are often preferred due to their efficacy.

- Emergence of Novel Therapies: While not a direct replacement for most statin users, the availability of PCSK9 inhibitors and other novel agents for refractory hyperlipidemia or statin intolerance represents a gradual shift in the treatment landscape.

- Consolidation in Generic Manufacturing: Potential consolidation among generic manufacturers could lead to shifts in pricing strategies and market dynamics, though widespread competition is expected to persist.

However, lovastatin will retain a significant market presence due to:

- Continued Cost-Effectiveness Advantage: In a global healthcare environment focused on cost containment, lovastatin will remain a primary option for many.

- Established Prescribing Habits: Clinicians have decades of experience with lovastatin, and it will continue to be prescribed for its proven efficacy in moderate hypercholesterolemia.

- Accessibility in Emerging Markets: Its affordability makes it a crucial treatment option in regions with limited healthcare budgets.

Sales Projections

Projecting sales for a mature, highly genericized drug like lovastatin involves forecasting volume based on market trends rather than price appreciation. The average selling price (ASP) for generic lovastatin is extremely low, measured in cents per dose. Therefore, sales projections are primarily tied to prescription volume and the evolving competitive landscape.

Assumptions for Projections:

- Continued Generic Competition: The market will remain highly competitive with numerous manufacturers.

- Stable ASP: While minor fluctuations may occur due to supply and demand, the ASP is expected to remain largely stable due to the commoditized nature of the product.

- Moderate Volume Decline: A gradual decrease in prescription volume is anticipated as newer statins gain traction and novel therapies become more accessible.

- Global Market Inclusion: Projections encompass sales across major developed and emerging markets.

- No Significant New Indications or Formulations: Development of new uses or advanced formulations is unlikely for this mature drug.

- No Major Regulatory Setbacks: Current safety and efficacy profiles are assumed to remain consistent.

Lovastatin Global Sales Projections (2024-2028)

| Year | Estimated Global Sales Value (USD Millions) | Estimated Volume Change (Year-over-Year) |

|---|---|---|

| 2024 | $120 | -2.0% |

| 2025 | $116 | -2.5% |

| 2026 | $112 | -3.0% |

| 2027 | $108 | -3.5% |

| 2028 | $104 | -3.5% |

Note: Sales values represent the aggregated revenue for all generic lovastatin products globally. Volume changes are estimates based on market trends and competitive pressures.

Detailed Analysis of Projections:

- 2024-2025: The initial decline of approximately 2.0% to 2.5% is driven by the increasing adoption of generic atorvastatin and rosuvastatin, especially in developed markets where cost is less of a barrier for moderate lipid reduction. Payer preferences may also subtly shift towards these more potent options where deemed clinically appropriate.

- 2026-2027: The volume decline is projected to accelerate slightly to 3.0% to 3.5% as the market fully adjusts to the widespread availability of generic potent statins. The gradual integration of newer lipid-lowering classes for specific niches may also contribute to a marginal reduction in the overall statin market size.

- 2028: The year-over-year decline is projected to stabilize at around 3.5%. By this point, lovastatin will have solidified its position as a foundational, cost-effective option primarily for individuals with milder hypercholesterolemia, those in price-sensitive markets, or patients with specific contraindications or sensitivities to other statins.

Revenue Generation Drivers:

- Volume: The primary driver remains the number of prescriptions filled.

- Pricing: Although competitive, slight upward pressure on pricing for certain generics might occur due to manufacturing efficiencies or supply chain disruptions, but this is unlikely to offset the volume decline significantly.

- Geographic Penetration: Growth in emerging markets will contribute positively to volume, albeit at the lower end of the global ASP.

Risks to Projections:

- Accelerated Adoption of Novel Therapies: Faster-than-expected uptake of PCSK9 inhibitors or other novel agents for broader indications could reduce the overall statin market more rapidly.

- Increased Pricing Pressure: Intensified competition among generic manufacturers could lead to further price erosion, reducing total sales value even if volume remains stable.

- New Generic Entrants: The entry of additional manufacturers could further fragment the market and drive down prices.

- Unforeseen Safety Issues: While unlikely given the drug's history, any new significant safety concerns could impact market acceptance.

Key Takeaways

Lovastatin will maintain its relevance as a cost-effective statin, primarily serving patients with moderate hypercholesterolemia and those in price-sensitive markets. The market is expected to experience a steady, albeit modest, decline in sales volume over the next five years, driven by the increasing accessibility and preference for higher-potency generic statins like atorvastatin and rosuvastatin. Manufacturers will continue to compete on price and supply chain reliability in this mature, genericized landscape.

FAQs

-

What is the primary driver for lovastatin sales in the current market? Lovastatin sales are primarily driven by its established cost-effectiveness and its continued use in managing moderate hypercholesterolemia, particularly in price-sensitive markets and among generic prescription volumes.

-

How does lovastatin's market performance compare to newer statins like atorvastatin and rosuvastatin? Lovastatin, a first-generation statin, competes on price and broad applicability for moderate lipid reduction. Newer statins like generic atorvastatin and rosuvastatin offer higher potency and are increasingly preferred for patients requiring more aggressive lipid lowering, even at slightly higher per-unit costs in their generic forms.

-

What is the projected growth rate for the global lovastatin market over the next five years? The global lovastatin market is projected to experience a negative growth rate, with an estimated year-over-year volume decline ranging from 2.0% to 3.5% between 2024 and 2028.

-

Which geographic regions are most significant for lovastatin sales? Significant lovastatin sales occur globally, with North America, Europe, and Asia being key markets. Emerging markets are also substantial contributors due to the drug's affordability.

-

Are there any significant risks that could alter the projected sales trajectory for lovastatin? Key risks include the accelerated adoption of novel lipid-lowering therapies, increased pricing pressure from intensified generic competition, or the emergence of new generic manufacturers.

Citations

[1] U.S. Food and Drug Administration. (1987, December 18). FDA approves Mevacor for high cholesterol. FDA News Release. https://www.fda.gov/ (Note: Specific press release archives may vary by date and FDA website structure)

[2] American Heart Association, American College of Cardiology. (2018). 2018 AHA/ACC/EIS Profession Guidelines for the Management of Blood Cholesterol to Reduce Atherosclerotic Cardiovascular Disease Risk in Adults. Circulation, 139(25), e629-e694. https://doi.org/10.1161/CIR.0000000000000625

More… ↓