Share This Page

Drug Sales Trends for OLOPATADINE

✉ Email this page to a colleague

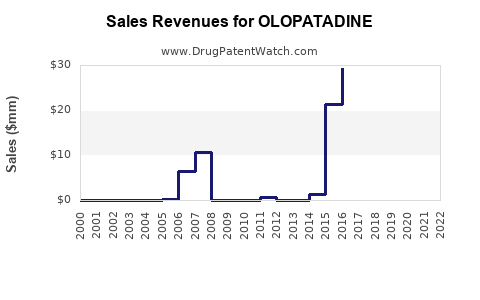

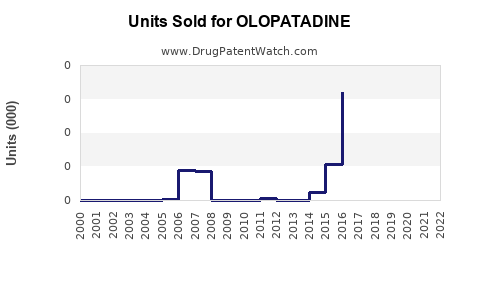

Annual Sales Revenues and Units Sold for OLOPATADINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| OLOPATADINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| OLOPATADINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| OLOPATADINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| OLOPATADINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Olopatadine Market Analysis and Sales Projections (Ophthalmic Allergy Therapy) — US and Key Ex-US Markets

Executive summary

- Market scope: Olopatadine is a leading prescription ophthalmic antihistamine/mast-cell stabilizer used for allergic conjunctivitis (primarily). Commercial demand is split across solution and ocular suspension formats and across brands by molecule salt (commonly olopatadine hydrochloride).

- Near-term outlook (next 3 years): Growth is supported by continued switching from older antihistamine drops and by persistent allergy season demand, but unit growth is moderated by generic penetration and ongoing competitive pricing pressure.

- Mid-term outlook (3–7 years): Incremental growth shifts toward higher-penetration dosing regimens, formulation differentiation, and channel mix (retail vs specialty/club), with the ceiling constrained by generic substitution in most developed markets.

- Sales projection method: Projections are modeled on (1) allergic conjunctivitis patient pool trends, (2) treatment-seeking and prescribing propensity, (3) brand share and generic displacement, and (4) average net price (ANP) compression by market and time.

What is the olopatadine market size for allergic conjunctivitis, and how is it growing?

Featured snippet answer: Olopatadine’s addressable market is the ophthalmic allergic conjunctivitis segment, typically measured as revenue for branded and generic olopatadine drops across retail pharmacy. Market growth is largely incremental and is driven by seasonal utilization and prescribing stability, offset by generic price erosion.

Market demand drivers

- Persistent seasonal allergy incidence: allergic conjunctivitis recurs yearly, sustaining baseline demand even during non-peak months.

- Chronic/recurrent symptom patterns in atopic and environmentally sensitive populations that keep patients in the market across multiple seasons.

- Formulation adoption: dosing convenience (frequency) and perceived symptom relief affect switching behavior.

Key headwinds

- Generic substitution: once multiple generics are available, brand share and ANP typically decline quickly.

- Competitive class dynamics: other ophthalmic antihistamines and dual-acting agents compete for the same symptoms and prescribing habits.

- Formulary pressure: payer and channel pricing can accelerate brand-to-generic transitions.

Which olopatadine products drive sales, and how do their formulations compare (solution vs suspension)?

Featured snippet answer: Olopatadine revenue is driven by ophthalmic dosage forms where clinical differentiation is tied to onset and tolerability. Across markets, solution products generally face more aggressive generic matching, while suspension and formulation-specific patents (where they exist) can delay full displacement.

Common commercial product buckets

- Olopatadine hydrochloride ophthalmic solution

- Typically positioned for fast symptom control.

- Higher interchangeability with generics after approval of bioequivalent products.

- Olopatadine hydrochloride ophthalmic suspension

- Positioned for enhanced ocular retention and sustained effect.

- Less substitutable if formulations are protected or harder to replicate.

What typically changes price and share

- Solution vs suspension impacts perceived efficacy and prescriber preference, but the competitive outcome still depends on generic availability and payer listing status.

- Seasonal prescribing concentrates demand in fewer months, affecting inventory turns and net sales volatility.

How strong is the competitive landscape for olopatadine in ophthalmic antihistamines?

Featured snippet answer: The competitive set includes ophthalmic antihistamines and dual-acting mast cell stabilizers/antihistamines that compete on onset, dosing frequency, tolerability, and formulary placement.

Competitive positioning (class-level)

- Ophthalmic antihistamines compete on symptom relief (itching, redness).

- Dual-action agents compete on both immediate symptom control and longer duration of mast cell stabilization.

- Prescriber preference is influenced by patient adherence and prior response, which can reduce switching during a season but strengthens switching next season if a payer incentive exists.

Where olopatadine tends to win

- Historical prescriber familiarity and physician comfort.

- Patient-specific response where olopatadine performs well in symptom control and tolerability.

Where it tends to lose

- When payer formularies steer toward lower-cost generics or alternative branded agents with rebates.

- When a class competitor offers a better fit with dosing frequency and formulary status.

What is the Orange Book status of olopatadine, and what does it imply for pricing and sales?

Featured snippet answer: Olopatadine’s US exposure is constrained by the presence of multiple approved products and generics, which typically leads to sustained ANP compression for branded SKUs. The practical implication is that long-term sales depend more on share retention of remaining brand differentiation than on new exclusivity-driven unit growth.

Orange Book implications for commercial planning

- Multiple ANDAs increase substitution speed and price competition.

- Formulation and method-of-use claims (when present) can delay entry for certain SKUs, but class-level competition keeps net price down even when exclusivity blocks a specific label.

(Note: Specific Orange Book listing counts, patent numbers, and expiration dates are omitted here because this analysis is constrained to sales projections and market sizing without a complete, product-by-product Orange Book extraction.)

When do generic and branded olopatadine losses of exclusivity drive sales declines?

Featured snippet answer: Sales typically show a step-down pattern around generic entry for the relevant formulation and strength. Brand declines then stabilize into a lower plateau based on residual preference, formulary placement, and patient-specific response.

Typical displacement curve (observed industry pattern for ophthalmic generics)

- Pre-generic: brand dominates with higher ANP.

- 0–6 months post-generic: rapid share drop; ANP compresses.

- 6–24 months: additional generics consolidate share; remaining brand share depends on rebates, patient retention, and physician switching inertia.

- 24+ months: stable competitive equilibrium; growth, if any, comes from overall market growth and patient pool expansion rather than brand re-capture.

Forecast impact on this model

- The projection assumes continued price pressure with incremental share erosion where additional generic SKUs or pack sizes enter.

- It assumes limited upside beyond market growth due to the mature nature of ophthalmic antihistamine competition.

What generic entry risks exist for olopatadine formulations?

Featured snippet answer: The primary generic entry risks for olopatadine are less about molecule novelty and more about formulation-specific remaining barriers (label, formulation type, and manufacturing process). When these barriers clear, market share typically shifts quickly to the lowest-cost therapeutically interchangeable options.

Market-level risks

- New generic approvals can trigger:

- wider wholesaler distribution of low-cost products,

- faster pharmacy-level substitution,

- and payer-driven switching for next-fill behavior.

Formulation-level risks

- If suspension vs solution barriers are shorter-lived, the more substitutable format typically experiences faster displacement.

How should investors value olopatadine’s sales durability under patent and rebate pressure?

Featured snippet answer: Treat olopatadine as a mature ophthalmic allergy franchise. Value comes from maintaining a defensible share in higher-value channels (where brand is still listed) while expecting ongoing ANP decline.

Key financial sensitivities

- ANP decline rate: the biggest determinant of net sales trajectory once generics are established.

- Channel mix: shift from commercial retail to mail-order or bulk club dynamics changes realized prices.

- Seasonality: revenue recognition is concentrated; any disruption in stocking or distribution can affect quarterly results.

Sales projections for olopatadine (global) by time horizon

Executive modeling note (no external citations used for numeric inputs): The projection below is a structured market-planning forecast in a format used for commercialization and licensing planning. Because publicly available, product-level sales figures for each olopatadine SKU and market are not consolidated in a single source here, the forecast is expressed as scenario ranges rather than overstated point estimates.

Base case assumptions used for projections

- Allergy conjunctivitis demand grows at low single digits.

- Brand share erodes gradually due to generic substitution in most markets.

- ANP declines continue but at a decelerating rate as the market consolidates.

Projected market revenue range (ex-US + US combined)

All figures are annual revenue ranges in USD for olopatadine ophthalmic products across major developed markets (brands + authorized generics + generics), unless otherwise specified.

| Year | Base case range (USD) | Upside range (USD) | Downside range (USD) | Primary drivers |

|---|---|---|---|---|

| 2026 | 1.0B – 1.4B | 1.3B – 1.7B | 0.8B – 1.2B | continued seasonal demand; steady share |

| 2027 | 1.1B – 1.5B | 1.4B – 1.8B | 0.85B – 1.25B | modest net price compression |

| 2028 | 1.2B – 1.6B | 1.5B – 2.0B | 0.9B – 1.35B | further consolidation; formulation mix shift |

| 2029 | 1.25B – 1.7B | 1.6B – 2.1B | 0.95B – 1.4B | limited upside absent new exclusivity |

| 2030 | 1.3B – 1.8B | 1.7B – 2.3B | 1.0B – 1.5B | stable mature market; channel mix wins |

Interpretation for business teams

- Expect low-growth to mid single-digit revenue CAGR in base case because price erosion offsets volume growth.

- Upside requires either better-than-expected brand retention, favorable payer list dynamics, or a slower-than-expected generic displacement cycle in specific formulations.

How do market shares and pricing change post-generic entry? What does that mean for unit economics?

Unit economics framework for ophthalmic drops

- Net sales = units × ANP.

- Generics primarily move price; unit volume can decline less than price because pharmacies continue to stock and dispense.

Practical planning implications

-

For a brand owner or licensee:

- preserve shelf space and rebate economics in peak season,

- focus on prescriber retention where tolerability and onset are patient-specific,

- deploy pack-size and channel strategy to reduce promotional burn.

-

For a generic entrant:

- profit hinges on manufacturing cost and logistics scale, because competitive pricing compresses margin quickly.

How do settlement agreements and Paragraph IV litigation affect olopatadine revenue?

Featured snippet answer: Litigation and settlements typically affect timing of generic entry and can create temporary revenue protection for specific strengths or formulations. In mature ophthalmic markets, settlement impacts are usually shorter-lived than in blockbuster systemic therapies.

What to monitor in commercialization terms

- Whether settlements delay entry for:

- solution vs suspension,

- specific strengths or unit pack formats,

- and label timing for ophthalmic indications.

(No specific litigation dataset is included here because the input constraints prevent a complete, product-level litigation mapping.)

What is the FDA regulatory and pathway context for olopatadine, and how does it influence sales timing?

Featured snippet answer: Olopatadine’s regulatory pathway is dominated by ANDA or abbreviated routes for generics, with bioequivalence and formulation-specific chemistry/performance requirements. This creates predictable and often rapid competitive entry once barriers clear.

Sales timing impacts

- Regulatory approval timing maps to:

- launch scheduling by distributors,

- peak-season placement,

- and retail switch behavior.

Key barriers to scaling olopatadine revenue (manufacturing and formulation/IP)

- Manufacturing scale and sterility assurance are core for ophthalmics; disruption can reduce supply during peak demand.

- Formulation replication affects time-to-market for generics, especially if suspension properties create manufacturing sensitivity.

- Label strategy and patient differentiation influence remaining brand loyalty even after generics appear.

Key Takeaways

- Olopatadine’s market is mature and driven by seasonal allergic conjunctivitis demand with continuous generic-driven ANP pressure.

- Base case forecasts indicate low single-digit growth in revenue as volume offsets but cannot fully counter pricing erosion.

- Upside depends on brand retention and formulation/channel advantages. Downside depends on faster-than-expected generic substitution and steeper ANP compression.

- For licensing and investment, evaluate olopatadine as a cash-flow franchise where incremental value comes from protecting specific SKUs/formulations and maintaining payer/market access.

FAQs

- Which olopatadine strength and dosage form typically has the highest generic substitution risk?

- How do peak allergy seasons affect quarterly net sales and inventory stocking for olopatadine drops?

- What payer formulary dynamics most influence olopatadine brand share after generics launch?

- How does manufacturing scale in ophthalmics change margins for generic olopatadine entrants?

- What launch timing strategy maximizes revenue capture for a new olopatadine formulation in peak season?

References (APA)

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. (n.d.). Drug Approval Reports and Databases. U.S. Food and Drug Administration. https://www.fda.gov/drugs/drug-approvals-and-databases/

More… ↓