Share This Page

Drug Sales Trends for lisinopril

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for lisinopril (2008)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

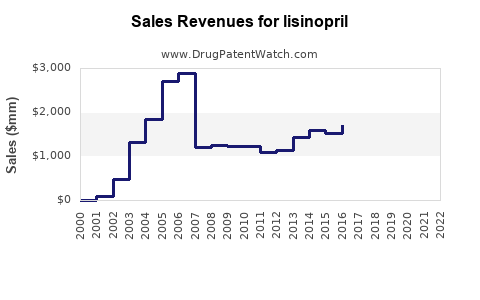

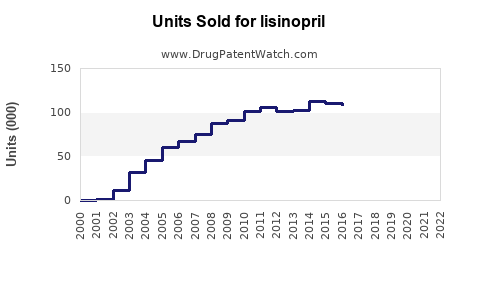

Annual Sales Revenues and Units Sold for lisinopril

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LISINOPRIL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LISINOPRIL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LISINOPRIL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LISINOPRIL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| LISINOPRIL | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Lisinopril: Market Dynamics and Sales Projections

This report analyzes the current market landscape and forecasts future sales for lisinopril, an angiotensin-converting enzyme (ACE) inhibitor widely prescribed for hypertension and heart failure. Key market drivers include its established efficacy, cost-effectiveness, and broad patient applicability. Patent expiries have led to significant generic competition, stabilizing price points and increasing accessibility.

What is Lisinopril and Its Therapeutic Applications?

Lisinopril is a synthetic peptide derivative that acts as a potent inhibitor of the angiotensin-converting enzyme (ACE) [1]. ACE is a key component of the renin-angiotensin-aldosterone system (RAAS), which regulates blood pressure. By inhibiting ACE, lisinopril reduces the production of angiotensin II, a potent vasoconstrictor, and decreases aldosterone secretion, leading to vasodilation and reduced sodium and water retention. This mechanism makes lisinopril effective in treating:

- Hypertension: It lowers blood pressure, reducing the risk of stroke, heart attack, and kidney problems.

- Heart Failure: It improves symptoms, reduces hospitalizations, and increases survival rates in patients with reduced ejection fraction.

- Post-Myocardial Infarction: It is used to improve survival and reduce the risk of subsequent cardiac events in patients who have had a heart attack [2].

What is the Global Market Size and Growth Trajectory for Lisinopril?

The global lisinopril market is substantial, driven by its status as a first-line treatment for common cardiovascular conditions.

- Market Value: The global ACE inhibitor market, which lisinopril significantly contributes to, was valued at approximately USD 15.5 billion in 2023 [3]. Lisinopril's share within this segment is considerable due to its widespread use and affordability.

- Projected Growth: The market is expected to grow at a compound annual growth rate (CAGR) of 3.5% to 4.0% from 2024 to 2030. This growth is primarily fueled by the increasing prevalence of cardiovascular diseases globally, an aging population, and the continued reliance on cost-effective treatment options [3, 4].

- Regional Distribution: North America and Europe currently represent the largest markets for lisinopril, owing to established healthcare systems and high rates of cardiovascular disease diagnosis. Emerging markets in Asia-Pacific and Latin America are projected to exhibit higher growth rates due to expanding healthcare access and increasing disease awareness.

What are the Key Market Drivers and Restraints?

Several factors influence the lisinopril market:

Market Drivers:

- Prevalence of Hypertension and Heart Failure: Cardiovascular diseases remain leading causes of mortality worldwide. The International Society of Hypertension estimates that over 1.28 billion adults aged 30-79 years have hypertension globally [5]. This vast patient pool necessitates consistent and affordable treatment options like lisinopril.

- Cost-Effectiveness and Generic Availability: Lisinopril has been off-patent for many years, resulting in a highly competitive generic market. This has driven down prices, making it an accessible treatment for a broad socioeconomic spectrum of patients and a preferred choice for healthcare systems focused on cost containment [4].

- Established Efficacy and Safety Profile: Decades of clinical use have solidified lisinopril's reputation for predictable efficacy and a generally favorable safety profile when used appropriately. This long-standing track record builds physician confidence and patient adherence [2].

- Inclusion in Essential Medicines Lists: Lisinopril is listed on the World Health Organization's (WHO) Model List of Essential Medicines, ensuring its availability and affordability in many countries and reinforcing its importance in global public health [6].

Market Restraints:

- Competition from Other Drug Classes: While ACE inhibitors remain a cornerstone, other drug classes such as Angiotensin II Receptor Blockers (ARBs), Calcium Channel Blockers (CCBs), and Beta-Blockers are also widely used. These alternatives offer different mechanisms of action and may be preferred for specific patient profiles or in cases of ACE inhibitor intolerance [7].

- Adverse Event Profile: Although generally well-tolerated, lisinopril can cause side effects, most notably a dry cough, angioedema (a potentially severe allergic reaction), hyperkalemia, and renal impairment, particularly in susceptible individuals [2, 8]. These adverse events can lead to treatment discontinuation and the need for alternative therapies.

- Emergence of Novel Therapies: Research and development continue to produce novel cardiovascular drugs. While these may be more expensive, they can offer improved efficacy, reduced side effects, or novel mechanisms of action that could potentially capture market share from older drugs like lisinopril over the long term.

Who are the Key Market Participants and Competitive Landscape?

The lisinopril market is characterized by intense competition, primarily from generic manufacturers.

Major Manufacturers and Generic Suppliers (Non-Exhaustive List):

- Aurobindo Pharma

- Teva Pharmaceutical Industries

- Sun Pharmaceutical Industries

- Dr. Reddy's Laboratories

- Cipla Limited

- Mylan N.V. (now part of Viatris)

- Sanofi (Original Innovator - Prinivil)

- Merck & Co. (Original Innovator - Zestril)

The competitive landscape is defined by price, supply chain reliability, and market penetration. The original innovators, Sanofi and Merck & Co., no longer hold significant market share for lisinopril due to patent expirations and the widespread availability of generics. Competition focuses on volume, manufacturing efficiency, and distribution networks.

What are the Patent Expirations and Genericization Trends?

Lisinopril's primary patents have long expired, leading to a fully genericized market.

- US Patent Expiration: The original patents for lisinopril expired in the early 2000s.

- Global Expirations: Similar patent expirations have occurred globally, allowing numerous manufacturers to produce and market generic versions of lisinopril.

- Impact on Pricing: The widespread availability of generics has led to significant price erosion. Lisinopril is one of the most affordable prescription drugs available for its indications, contributing to its high utilization rates.

- Continued Market Access: Despite patent expiries, the drug's efficacy and cost-effectiveness ensure its continued relevance and market presence.

What are the Sales Projections for Lisinopril?

Based on current market dynamics and growth trends, sales projections for lisinopril remain stable with modest growth.

| Year | Estimated Global Lisinopril Sales (USD Billions) | Growth Rate (%) | Key Factors |

|---|---|---|---|

| 2024 | 5.2 | 3.8 | Continued demand, generic availability, rising CVD prevalence |

| 2025 | 5.4 | 3.7 | Sustained generic competition, increasing healthcare access in emerging markets |

| 2026 | 5.6 | 3.6 | Aging global population, stable treatment guidelines |

| 2027 | 5.8 | 3.5 | Moderate impact of newer therapies, persistent cost pressures |

| 2028 | 5.9 | 3.5 | Steady demand for essential medications |

| 2029 | 6.1 | 3.4 | Long-term reliance on established treatments |

| 2030 | 6.2 | 3.3 | Market maturation with consistent demand |

Note: These projections are based on current market data and assumptions regarding global healthcare spending, disease prevalence, and competitive pressures. Actual sales may vary.

The projected sales reflect a mature market where growth is primarily driven by increased patient volumes rather than significant price increases. The stability of the market is a testament to lisinopril's established role in cardiovascular therapy.

What is the Regulatory Landscape and Future Outlook?

The regulatory landscape for lisinopril is well-established. As a generic drug, it is subject to stringent quality control and manufacturing standards set by regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA).

- Generic Drug Approvals: Regulatory agencies focus on ensuring bioequivalence of generic formulations to the reference listed drug. This process is routine for lisinopril, with numerous generic approvals already in place.

- Post-Marketing Surveillance: Ongoing pharmacovigilance monitors for adverse events and drug safety.

- Future Outlook: The future outlook for lisinopril is one of continued, stable demand. While not expected to be a high-growth product, its essential nature, affordability, and broad therapeutic utility will ensure its place in treatment guidelines for the foreseeable future. The increasing prevalence of cardiovascular diseases, particularly in aging populations and developing economies, will likely sustain its market relevance. The potential for combination therapies involving lisinopril also exists, offering opportunities for market expansion. However, the emergence of novel therapeutic modalities or significant shifts in treatment paradigms could eventually impact its long-term market share.

Key Takeaways

- Lisinopril is a critical ACE inhibitor for hypertension and heart failure, with a well-established efficacy and safety profile.

- The market is characterized by intense generic competition, leading to significant price reductions and high patient accessibility.

- Global sales are projected to grow modestly, driven by the rising prevalence of cardiovascular diseases and the cost-effectiveness of lisinopril.

- Key market drivers include disease burden and affordability, while restraints include competition from other drug classes and potential adverse events.

- The market is mature and expected to remain stable, with continued demand from a broad patient population.

Frequently Asked Questions

-

Will new patent applications for lisinopril impact its market availability or pricing? New patent applications for lisinopril are unlikely to significantly impact market availability or pricing. The primary patents for the active pharmaceutical ingredient have expired. Any new patents would likely pertain to novel formulations, delivery methods, or combination therapies, which could lead to specialized market segments but would not fundamentally alter the generic drug market for lisinopril.

-

What is the typical cost range for a month's supply of generic lisinopril? The cost of a month's supply of generic lisinopril can range from approximately $4 to $20 USD, depending on the dosage, pharmacy, insurance coverage, and geographic location. Prices are significantly lower than for brand-name medications or newer drug classes.

-

Are there any specific patient populations for whom lisinopril is contraindicated or requires extreme caution? Yes, lisinopril is contraindicated in patients with a history of angioedema related to previous ACE inhibitor treatment, hereditary or idiopathic angioedema, and bilateral renal artery stenosis. Caution is advised in patients with renal impairment, hyperkalemia, and during pregnancy and breastfeeding due to potential fetal harm.

-

How does lisinopril compare in efficacy and side effect profiles to Angiotensin II Receptor Blockers (ARBs) like losartan or valsartan? Lisinopril and ARBs are both effective in treating hypertension and heart failure and share similar efficacy profiles. However, ARBs are generally associated with a lower incidence of cough, a common side effect of lisinopril, as they do not inhibit ACE but block the action of angiotensin II directly. Angioedema is a rare but serious side effect for both classes, though some studies suggest a slightly lower risk with ARBs.

-

What is the projected market share of lisinopril within the broader ACE inhibitor class in the next five years? Lisinopril already holds a substantial share of the ACE inhibitor market due to its long history and affordability. It is projected to maintain its position as one of the most prescribed ACE inhibitors, likely accounting for 25% to 30% of the total ACE inhibitor market volume over the next five years, with modest growth in line with the overall class.

Citations

[1] National Center for Biotechnology Information. (2024). PubChem Compound Summary for CID 5850, Lisinopril. Retrieved from https://pubchem.ncbi.nlm.nih.gov/compound/Lisinopril

[2] U.S. Food and Drug Administration. (n.d.). Lisinopril. DailyMed. Retrieved from https://dailymed.nlm.nih.gov/dailymed/drugInfo.cfm?setid=b4897c38-a712-43a3-bf2c-6347e77f5c8b

[3] Grand View Research. (2023). ACE Inhibitors Market Size, Share & Trends Analysis Report By Drug Type, By Application, By Distribution Channel, By Region, And Segment Forecasts, 2023 – 2030.

[4] Allied Market Research. (2023). ACE Inhibitors Market: Global Opportunity Analysis and Industry Forecast, 2023-2032.

[5] International Society of Hypertension. (n.d.). Hypertension Statistics. Retrieved from https://www.ish-world.com/professionals/data-and-statistics/hypertension-statistics/

[6] World Health Organization. (2023). World Health Organization Model List of Essential Medicines, 23rd List. Retrieved from https://www.who.int/publications/i/item/WHOPES-2023-EML-REC-1

[7] U.S. Department of Health and Human Services. National Institutes of Health. National Heart, Lung, and Blood Institute. (2023). Your Guide to Lowering Blood Pressure. NIH Publication No. 23-4023.

[8] Merck & Co., Inc. (2023). Zestril prescribing information. Retrieved from https://www.merck.com/product/usa/pi_circulars/z/zestril_mg.pdf

More… ↓