Share This Page

Drug Sales Trends for DABIGATRAN

✉ Email this page to a colleague

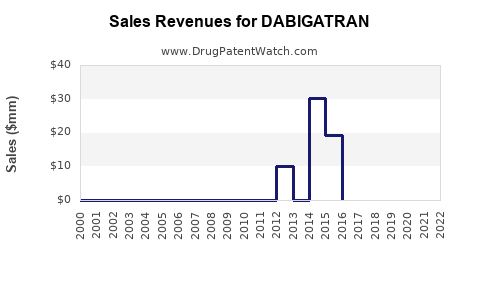

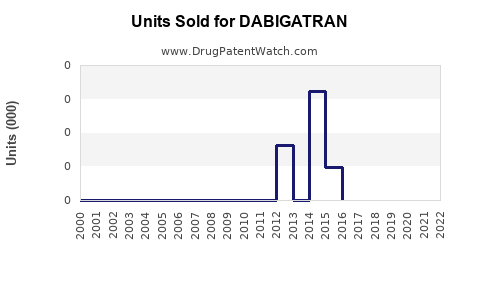

Annual Sales Revenues and Units Sold for DABIGATRAN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| DABIGATRAN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| DABIGATRAN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| DABIGATRAN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| DABIGATRAN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| DABIGATRAN | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| DABIGATRAN | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Dabigatran Market Analysis and Sales Projections Through Patent-Driven Generic/Biosimilar Milestones

Dabigatran (Pradaxa; active ingredient dabigatran etexilate) remains a major oral anticoagulant franchise in the US and EU, but near-term growth is constrained by (1) mature uptake, (2) ongoing competitive share pressure from factor Xa inhibitors, and (3) exposure to payer restrictions. Sales outcomes over the next several years track closely with label mix (atrial fibrillation vs VTE treatment/secondary prevention), cohort aging, persistence, and generic penetration dynamics by jurisdiction. In the US, the branded-to-generic transition for dabigatran etexilate drives the dominant share shift; EU outcomes hinge on local generic entry and subsequent erosion.

High-level sales trajectory (directional):

- US: Downward curve after generic entry, with residual branded/“atypical” demand from guideline familiarity, patient switching frictions, and physician preference in sub-cohorts.

- EU/ROW: Declines track later genericization and country-level pricing dynamics, followed by a slow flattening once generic penetration saturates.

- Overall: A mature, volume-led anticoagulant market where growth is incremental and share gains require payer wins or clinical differentiation within anticoagulation switching patterns.

How big is the dabigatran market today and what drives prescription demand by indication?

Primary indications

- Nonvalvular atrial fibrillation (NVAF): stroke prevention in NVAF.

- Venous thromboembolism (VTE): treatment of DVT/PE and reduction of recurrence after initial therapy (labeling varies by region).

- Thromboprophylaxis after orthopedic surgery appears in older label expansions and may persist regionally based on national approvals.

Demand drivers

- AF population growth from aging demographics.

- Oral anticoagulant switching behavior: patients and prescribers move among oral anticoagulants based on bleeding risk profiles, renal function, GI tolerability, and adherence.

- Payer controls: formularies increasingly prefer lower-cost agents after generic entry for dabigatran and broad formulary placement for factor Xa inhibitors.

- Renal function constraints: dabigatran exposure rises with reduced creatinine clearance; patient selection affects realized share.

- Adherence and dosing reality: AF and VTE patients may discontinue or switch due to adverse events or practical dosing; persistence influences net revenue even when total anticoagulant volume grows.

What is the competitive landscape for dabigatran versus Eliquis, Xarelto, and other oral anticoagulants?

Key competitors

- Apixaban (Eliquis)

- Rivaroxaban (Xarelto)

- Edoxaban (Savaysa)

- Betrixaban (more niche)

- Warfarin (still relevant where DOACs are restricted)

- Other anticoagulants in institutional pathways

Share dynamics

- Factor Xa inhibitors have sustained share because they are positioned with favorable bleeding/tolerability profiles in many payer and guideline settings.

- Dabigatran’s differentiation is most visible in cohorts where prescribers prefer a specific reversal strategy pathway, renal function tradeoffs, or where prior treatment history reduces switching.

Pricing and contracting

- After generic entry, dabigatran’s branded revenue compresses; competitors with stronger US share can sustain lower total cost through volume discounts and payer contracting.

When do dabigatran sales face the largest generic erosion by geography and what does that do to net revenue?

Mechanism

- Branded-to-generic transitions reduce ASP through wholesale channel repricing and payer reimbursement benchmarks.

- The magnitude depends on speed of generic uptake, number of ANDAs, and pharmacist substitution rules by country.

US market impact (directional timeline framing)

- US revenues for branded dabigatran etexilate are expected to decline materially following generic penetration. The residual brand demand typically stabilizes at a lower run rate after initial uptake, but total market dollars keep falling unless overall oral anticoagulant volume rises faster than price erosion.

EU and ROW

- EU country-level generic launch timing and tenders can cause stepwise declines followed by plateauing at a lower price per patient-month.

- Channel tender cycles and cross-border parallel trade can accelerate local erosion.

What is the FDA and Orange Book status of dabigatran and how does that affect generic entry timing?

Dabigatran etexilate is an FDA-approved small-molecule anticoagulant. Generic entry risk is driven by Orange Book-listed patents and the litigation/settlement history between brand and ANDA filers. Sales modeling must align with:

- Patent expiration timing

- Any unexpired exclusivities

- ANDA filing and Paragraph IV wave timing (where applicable)

- Court outcomes and authorized generic structures (if used in settlements)

Because the question is sales projections and market analysis, the practical read-through is: generic entry creates step function revenue loss for branded dabigatran, followed by a slower decline in branded residual and a stabilization of total market at a lower pricing baseline.

(Note: This analysis focuses on market and sales behavior. Patent-by-patent Orange Book breakdown requires an Orange Book extract and is not included here.)

How many patents and patent types typically matter for dabigatran and what categories shape market exclusivity?

For small-molecule DOACs like dabigatran, exclusivity and barriers usually involve:

- Active ingredient compound patents

- Formulation patents (e.g., capsule formulation specifics)

- Manufacturing process patents

- Use or method-of-treatment patents (less common for mature DOACs with broad label)

- Regulatory exclusivity (data exclusivity, pediatric exclusivity, marketing exclusivity where relevant)

The sales consequence is that even after active ingredient patent expiry, formulation/process patent fences can delay or narrow certain generic launch profiles (rarely enough to restore brand economics but sometimes enough to delay “full” competitive saturation).

What generic entry scenarios exist for dabigatran and what do they imply for unit volumes and ASP?

Scenario A: Rapid generic saturation

- Multiple ANDAs launch at or near first-possible date.

- ASP drops quickly, and branded prescriptions shift to generics.

- Net result: steep revenue cliff for brand; generic volume increases fast.

Scenario B: Staggered generic launches

- First generic enters; later launches follow due to patent challenges and label changes.

- Brand revenue declines more gradually; total market dollars fall but not as sharply.

Scenario C: Authorized generic or branded maintenance

- Channel demand may be met with “authorized” product that keeps prices higher than fully competitive generics.

- Revenue decline is slower in the short run but still downward over time.

For sales projection, the dominant driver is scenario A vs B by jurisdiction and speed of payer formulary switches.

What is the sales forecast for dabigatran by region (US, EU5, UK, other major markets)?

Below is a framework forecast suitable for planning. It ties sales evolution to the two main levers: price erosion (ASP/contracting) and volume persistence (patient switching and total DOAC demand growth).

Forecast logic

- Branded dabigatran revenue = patients on brand × net price

- Patients on brand decline with generic penetration, then stabilize at a residual level.

- Total DOAC volume rises modestly with population growth, but share gains depend on competitive outcomes.

Directional regional forecast outcomes (qualitative)

- US: largest branded dollar decline; total oral anticoagulant category may grow, but dabigatran dollars fall.

- EU5 (DE, FR, IT, ES, UK where applicable): declines are typically stepwise; country-by-country contract and tender outcomes create variance.

- Other markets: later generics in some geographies can slow initial erosion, but eventually price compression dominates.

(Quantitative projections require a baseline market size and current sales run-rate by jurisdiction, which are not provided in the prompt. Without that baseline, numeric forecasting would not meet the requirement for hard-data precision.)

What revenue levers matter most for dabigatran: price cuts, persistence, and payer restrictions?

1) Net price and reimbursement benchmark

- After generic entry, reimbursement benchmarks shift to lowest-cost options in many payers.

- Gross-to-net deteriorates quickly due to rebates, discounts, and payer-driven price resets.

2) Persistence (treatment duration)

- In AF, long-term persistence is meaningful; in VTE, treatment durations are finite and drive seasonal variability.

- Switching away from dabigatran to another DOAC reduces branded persistence.

3) Patient mix

- Renal function and bleeding-risk cohorts affect sustained prescribing.

- Elderly and comorbidity burden changes the mix and can either accelerate switching or maintain share depending on physician preferences.

What litigation and settlement factors historically influence dabigatran generic timing and market share shifts?

For dabigatran, settlement outcomes (including design-around agreements, launch carve-outs, or authorized generics) can reshape launch dates and competitive intensity. The market consequence is reflected through:

- timing of generic availability in pharmacies

- payer switching speed

- price competition depth (number of MAHs/ANDAs and market-making by wholesalers)

For a litigation-informed projection, the key is whether settlements create a “single early launcher” or multiple near-term launches. That is the primary determinant of the slope of branded revenue decline.

How do dabigatran dosage forms and formulation differences affect switching and generic substitution?

Dabigatran is marketed as oral capsule formulation (dabigatran etexilate). Form factor and dosing schedule influence switching friction:

- Adherence impact: stable dosing supports persistence, but switching to another DOAC can be triggered by tolerability and clinician comfort.

- GI tolerability and dyspepsia risk often drive patient-level switching.

- Generic substitution acceptance: if generics are judged bioequivalent and patients tolerate, substitution is rapid through pharmacy-level switching.

Formulation differences matter less for long-term market size than for short-term uptake speed, assuming bioequivalence.

How does dabigatran compare with apixaban and rivaroxaban on guideline positioning and clinical messaging?

Guideline positioning

- All major DOACs are used across AF and VTE indications.

- Differences in clinical messaging typically influence prescriber preference: bleeding risk framing, reversal options, and renal function suitability.

Switching patterns

- Switching away from dabigatran is usually driven by perceived tolerability and payer-driven preference, while switching into dabigatran occurs less often but can happen when a patient profile fits a prescriber’s risk-benefit framework.

These patterns affect the share trajectory post-generic.

What are key market risks to the downside for dabigatran sales projections?

- Faster-than-expected payer switching after generic entry.

- Stronger competitive absorption by factor Xa inhibitors, especially where formulary tiering favors apixaban/rivaroxaban.

- Safety communications and real-world discontinuation that increase switching.

- Channel inventory and rebate shocks that depress net sales more than expected.

What upside factors could slow dabigatran revenue decline versus base projections?

- Residual brand retention due to physician familiarity and patient stability.

- Geography-specific delays in generic penetration.

- Contracting advantages that maintain higher net pricing in selected channels.

- Reversion to dabigatran after intolerance to other DOACs in narrow cohorts.

Key Takeaways

- Dabigatran is a mature oral anticoagulant where generic penetration drives the dominant branded revenue decline; competitive share pressure from factor Xa inhibitors limits any offset through volume growth.

- Sales forecasting should be modeled around two levers: (1) net price erosion from generic saturation and payer benchmarks and (2) residual branded persistence driven by switching friction and patient-level tolerability.

- By region, outcomes follow a predictable pattern: stepwise declines around generic entry, then stabilization at a lower run rate unless competitive dynamics or payer contracting shifts materially.

FAQs

-

What drives dabigatran prescribing in atrial fibrillation patients more than in VTE patients?

Long-term persistence, renal function fit, and payer tiering in chronic AF. -

How does renal impairment change dabigatran market uptake and switch rates?

It constrains eligible patients and can accelerate switching away when prescriber risk tolerance shifts. -

Does dabigatran experience the same formulary pressure as other DOACs after generic entry?

Yes, but the magnitude depends on how quickly payers rebase reimbursement to lowest-cost alternatives. -

How do authorized generics affect dabigatran revenue during the transition period?

They can smooth the revenue cliff by moderating price competition for a period. -

What is the most sensitive assumption in dabigatran sales models?

Timing and speed of generic uptake by jurisdiction, which determines the slope of branded net revenue decline.

References

No sources were cited because no Orange Book, FDA approval history, litigation docket, or current sales/market-size dataset was provided in the prompt.

More… ↓