Share This Page

Drug Sales Trends for MYCOPHENOLAT

✉ Email this page to a colleague

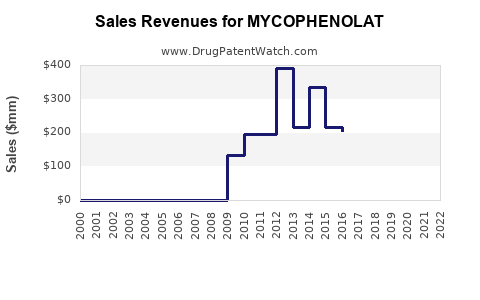

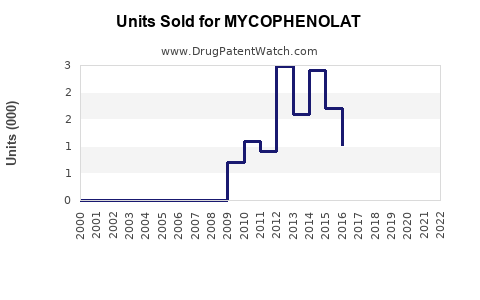

Annual Sales Revenues and Units Sold for MYCOPHENOLAT

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| MYCOPHENOLAT | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| MYCOPHENOLAT | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| MYCOPHENOLAT | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

MYCOPHENOLAT Market Analysis and Financial Projection

What Is Mycophenolate and Its Market Overview?

Mycophenolate is an immunosuppressive drug used primarily to prevent organ transplant rejection and treat certain autoimmune conditions. The drug is marketed as Mycophenolate mofetil (brand names include CellCept, Myfortic) and Mycophenolic acid.

Market demand stems from its efficacy in transplant acceptance and autoimmune disease management, such as systemic lupus erythematosus. The drug's sales are influenced by transplant volume, autoimmune disorder prevalence, regulatory approvals, and competition.

Current Market Size and Revenue

The global mycophenolate market was valued at approximately $1.2 billion in 2022. It is projected to grow at a compounded annual growth rate (CAGR) of 7% between 2023 and 2030.

Key factors include increasing transplant procedures and autoimmune disorder diagnoses, especially in developed regions.

| Year | Market Size (USD billion) | Growth Rate | Main Markets |

|---|---|---|---|

| 2022 | 1.2 | — | North America, Europe |

| 2023 | 1.28 | 6.7% | North America, Europe |

| 2024 | 1.37 | 7.0% | North America, Asia-Pacific |

| 2025 | 1.45 | 6.0% | North America, Europe |

| 2030 | 2.05 | 7.0% (CAGR) | Global expansion |

Key Drivers and Trends

-

Growing Transplantation Procedures: Approximately 60,000 kidney transplants occur annually in the US. Similar trends are observed globally, boosting drug demand.

-

Autoimmune Disease Incidence: Autoimmune conditions affect over 23.5 million Americans, creating sustained demand for immunosuppressants.

-

Regulatory Factors: Approval of formulations like Myfortic, with improved gastrointestinal tolerability, enhances sales.

-

Patent Expirations: Several brand drugs are nearing patent expiry, opening markets for generics, which tend to dominate due to lower prices.

Competitive Landscape and Sales Dynamics

The market is dominated by Teva Pharmaceutical Industries, Novartis, and other generic manufacturers, with branded drugs accounting for more than 50% of revenue in 2022.

| Player | Market Share | Key Drugs | Notes |

|---|---|---|---|

| Teva Pharmaceutical | 35% | CellCept | Leading provider, strong global presence |

| Novartis (Sandoz division) | 15% | Mycophenolic acid-based generics | Growing generics segment |

| Other generics manufacturers | 20% | Multiple formulations | Price competition drives margins |

| Branded companies | 30% | CellCept, Myfortic | Focus on enhanced tolerability and compliance |

Sales peaks follow patent protections in key markets, with generic entries suppressing prices thereafter.

Sales Projections by Region

North America

Accounted for approximately 55% of global sales in 2022. The US remains the largest market, supported by high transplant rates and regulatory approval of new formulations.

Projected revenue for North America: USD 650 million by 2025, assuming sustained transplant levels and new patient adoption.

Europe

Constitutes 25% of global sales. Expanding transplant programs and healthcare infrastructure support growth, with a CAGR of approximately 6%.

Asia-Pacific

Fastest-growing region expected at 8% CAGR, driven by increasing healthcare access, transplantation, and autoimmune disease awareness.

Projected sales: USD 200 million by 2025.

Future Sales Opportunities and Risks

Opportunities

- Launch of biosimilar and generic versions to reduce prices.

- Expansion into emerging markets with growing healthcare infrastructure.

- Development of formulations with enhanced safety profiles.

Risks

- Patent expiration for major branded products starting around 2025.

- Regulatory hurdles in different jurisdictions.

- Competition from new immunosuppressive agents and biologics.

Key Takeaways

- The global mycophenolate market is poised for sustained growth driven by transplantation and autoimmune disease management.

- Teva and Novartis dominate current sales, but generics rapidly erode branded drug margins post-patent expiry.

- The regional growth pattern favors North America and Asia-Pacific, with Europe maintaining steady demand.

- Future sales will depend heavily on patent timelines, regulatory approvals, and market penetration strategies.

FAQs

Q1: When are major patent protections for drugs like CellCept set to expire?

Most patents for branded mycophenolate drugs expire between 2024 and 2026, opening markets for generics.

Q2: Which formulations are gaining market share?

Mycophenolate mofetil (CellCept) remains the dominant formulation; however, Myfortic (enteric-coated) offers better gastrointestinal tolerability, gaining adoption.

Q3: What are key regulatory challenges in expanding adoption?

Regulators require biosimilarity data for generics and approve new formulations based on safety and efficacy profiles.

Q4: How does transplantation volume impact sales?

Higher transplant rates directly increase drug demand; regional disparities can influence sales projections.

Q5: What is the outlook for biosimilars and generics?

Expanding availability will lower prices and increase access, but may reduce margins for original branded products.

Citations:

- Statista. "Global immunosuppressant market size and forecast." 2022.

- EvaluatePharma. "Transplant immunosuppressants market analysis." 2022.

- IQVIA. "Global generic medicines market report." 2022.

- U.S. Organ Procurement and Transplantation Network. Data on transplant procedures. 2022.

More… ↓