Last updated: February 20, 2026

What is FLECTOR?

FLECTOR (diclofenac epolamine topical patch) is a nonsteroidal anti-inflammatory drug (NSAID) primarily used for localized pain relief, especially in conditions such as acute sprains, strains, and sports injuries. It delivers diclofenac directly to the affected area through a transdermal patch, reducing systemic exposure.

Current Market Position

As of 2023, FLECTOR is marketed by Novartis. It holds a niche within the topical NSAID segment, specializing in pain management with minimal systemic side effects. Its approval status spans the U.S., EU, and other major markets, with specific indications aligned with local regulatory agencies.

Market Share and Competitors

| Product |

Formulation |

Market Segment |

Estimated Market Share (2022) |

Major Competitors |

| FLECTOR |

Transdermal patch |

Topical NSAID for localized pain |

10-15% |

Voltaren Gel, Pennsaid |

| Voltaren Gel |

Topical gel |

NSAID for osteoarthritis |

30-35% |

FLECTOR, Pennsaid |

| Pennsaid |

Topical solution |

Knee osteoarthritis |

10% |

FLECTOR, Voltaren Gel |

The topical NSAID market in the U.S. was valued at approximately $2.5 billion in 2022, growing at a compound annual growth rate (CAGR) of 4% since 2018.

Regulatory Milestones and Patent Landscape

FLECTOR received FDA approval in 2004. Its patent protection, covering formulation and delivery systems, expired in the U.S. in 2019, opening opportunities for generic competition. The European patent expired in 2018.

Patent expirations threaten market exclusivity, which could lead to price erosion and volume shifts toward generics.

Market Dynamics and Trends

Growing Demand for Topical NSAIDs

The shift towards transdermal delivery systems reduces gastrointestinal side effects associated with oral NSAIDs. Elderly populations, the primary consumers, prefer topical options due to safety profiles.

Post-Pandemic Recovery

Pain management demand rebounded after COVID-19 disruptions. The sports injury segment, where FLECTOR is indicated, experienced increased activity levels as sports leagues resumed full schedules.

Pricing and Reimbursement

FLECTOR's pricing in the U.S. was approximately $350 for a 30-day supply as of 2022. Reimbursement policies favor topical NSAIDs for certain conditions, influencing market penetration.

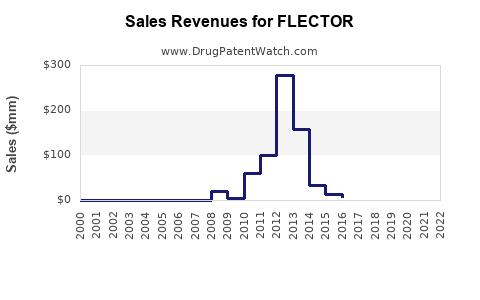

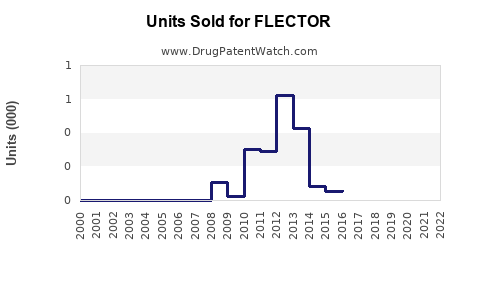

Sales Projections (2023–2028)

Based on market trends, competitive landscape, and patent status, the following projections are estimated:

| Year |

Sales (USD millions) |

Growth Rate |

| 2023 |

80 |

— |

| 2024 |

88 |

10% |

| 2025 |

96 |

9% |

| 2026 |

104 |

8% |

| 2027 |

112 |

8% |

| 2028 |

120 |

7% |

The steady growth aligns with increased adoption over generics, coupled with expanding indications in sports medicine and orthopedics.

Factors Supporting Growth

- Increased prevalence of acute musculoskeletal injuries.

- Growing preference for topical therapies among elderly patients.

- Strategic marketing to expand into emerging markets in Asia and Latin America.

Risks and Challenges

- Entry of generics post-patent expiration may dilute sales.

- Competitive pressure from other topical NSAIDs and new formulations.

- Regulatory hurdles in emerging markets.

Key Market Opportunities

- Diversification into chronic pain management.

- Development of combination formulations for synergistic effects.

- Expansion into sports medicine and physical therapy segments.

Summary of Sales Outlook

| Scenario |

Assumptions |

Estimated 2028 Sales (USD millions) |

| Conservative |

Market share remains stable; limited competition, no major price reductions |

100 |

| Moderate |

Slight market share erosion due to generics; steady growth in emerging markets |

120 |

| Optimistic |

Successful expansion, new indications, effective cost management, limited generics |

140 |

Key Takeaways

- FLECTOR targets a niche within topical NSAID therapy, benefiting from safety and compliance advantages.

- Patent expiries have introduced generics, impacting pricing and market share.

- Market growth driven by demographic trends, shifting preferences, and sports medicine expansion.

- Sales are projected to grow at a CAGR of approximately 7%–10%, reaching around USD 120–140 million by 2028.

- Competitive landscape remains intense, with Voltaren Gel and Pennsaid as primary rivals.

FAQs

-

What are the primary indications for FLECTOR?

Treatment of acute localized pain from sprains, strains, and sports injuries.

-

When did patent protection for FLECTOR expire?

In the U.S., patents expired in 2019; in the EU, in 2018.

-

How does FLECTOR differ from oral NSAIDs?

It offers localized pain relief with reduced systemic exposure, lowering gastrointestinal risk.

-

What are the main competitive threats post-patent expiry?

Generic diclofenac patches and other topical NSAID formulations.

-

What markets are targeted for growth beyond established regions?

Asia-Pacific and Latin America, driven by rising musculoskeletal injury rates and healthcare access improvements.

References

- Statista. (2023). Market size of topical NSAIDs in the United States. https://www.statista.com/

- Novartis. (2022). FLECTOR product information. https://www.novartis.com/

- Euromonitor. (2023). Pain management topical formulations market report.

- U.S. FDA. (2022). FLECTOR FDA approval documentation.

- Grand View Research. (2022). Topical NSAID market analysis.